Stress in the interbank market – Lehman Brothers reloaded?

Between the ECB meeting on the 12th September and the Fed meeting on the 18th September, the situation in the interbank market suddenly and unexpectedly came to a head. What happened? At its meeting, the ECB decided to make a further rate cut and ease refinancing operations for banks. In the run-up to its meeting, expectations were also that the Fed would make a further rate cut of 25 basis points. Let’s look into the details.

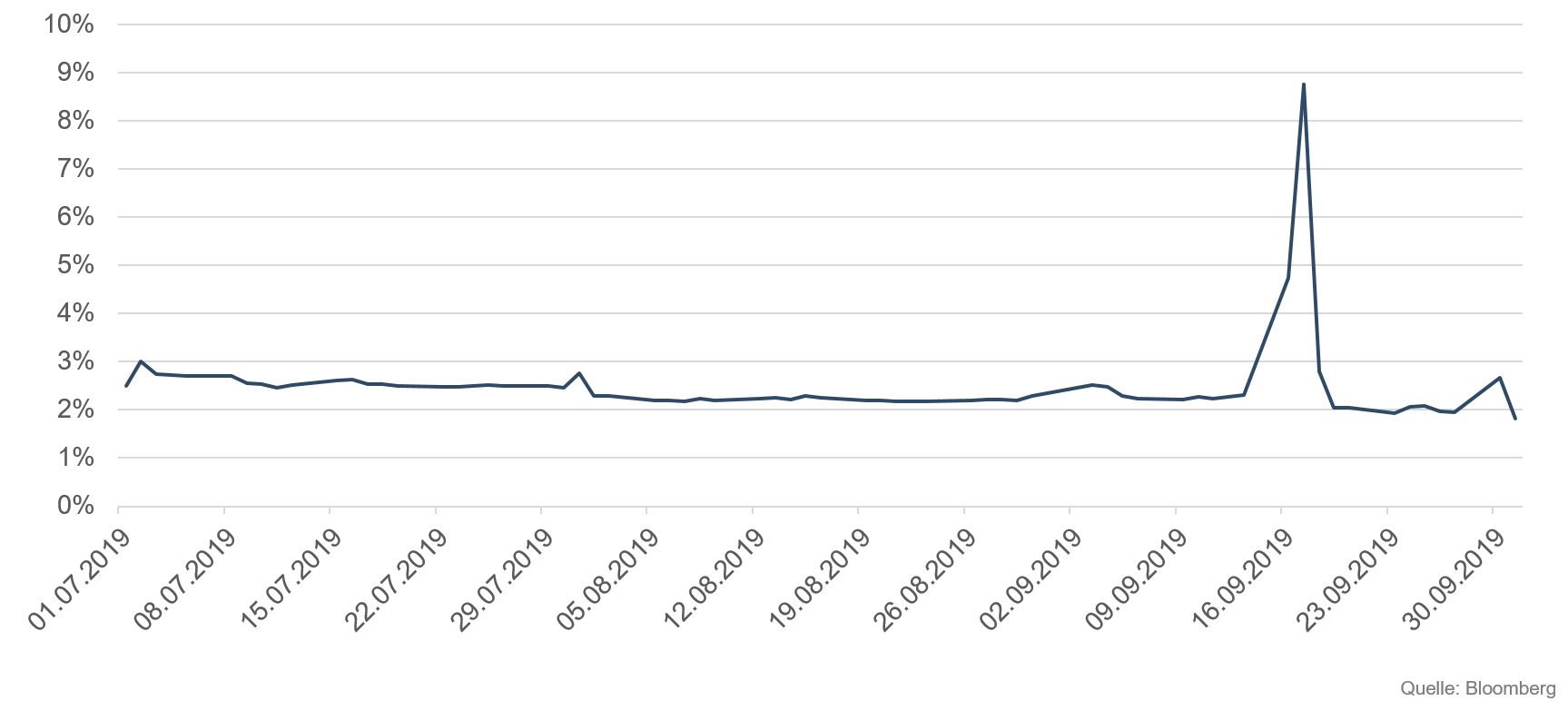

Money is cheap and getting cheaper. Before the US central bank meeting, the effective rates at which US banks borrow money overnight to meet the minimum reserve requirement had risen to slightly above the Fed Funds rate. But it wasn’t until Thursday, 17 September 2019, that this developed into a precarious situation for the US banking system.

With large corporate customers in the US due to pay their taxes in September, banks had to cover significant cash outflows. In addition, significant volumes of US Treasury Bills were issued and bought up by banks and primary dealers, resulting in a greater need for short-term liquidity in the whole banking system. Once the exact inflows and outflows have been ascertained and the bank’s financing requirements are known, then the required funds must be borrowed in the interbank market. Normally this would be business as usual. Since the US central bank’s bond purchase programmes, US commercial banks have been (technically) swimming in money. But things are different these days: while the effective Fed Funds rate for unsecured loans in the interbank market was up slightly at 2.25% on Monday evening, 16 September 2019, on Tuesday no money could be raised at these rates. The large institutions – which had excess liquidity – were not prepared to provide it at the usual interest rates. However, commercial banks had to meet their requirements. Over the course of the day, the cost of liquidity peaked at over 8% and was additionally covered with first-class collateral.

Figure 1: US overnight rate

In other words, the interest rate for overnight repurchase agreements rose to levels we haven’t seen since the collapse of Lehman Brothers investment bank. The situation threatened to escalate. If the costs of overnight refinancing exploded and exceeded the already marginal interest income, this would put banks in jeopardy. The Federal Reserve Bank of New York, which is responsible for providing emergency liquidity, was initially slow to react and on Tuesday, 17 September, it temporarily lost control of short-term interest rates.

The bank eventually did react, and provided the market with USD 75 billion in overnight repurchase agreements in an emergency intervention on Tuesday. But the tension did not let up, prompting the New York Fed to announce that it, as the lender of last resort, would not stop at offering overnight repurchase agreements. It would also provide 14-day maturities up to the end of the month. Together, these would equip the market with a peak amount of liquidity of USD 100 billion per day.

Thus disaster was once again averted for US banks. But is this how it’s going to be in the future?

Liquidity requirements in the banking market remain high

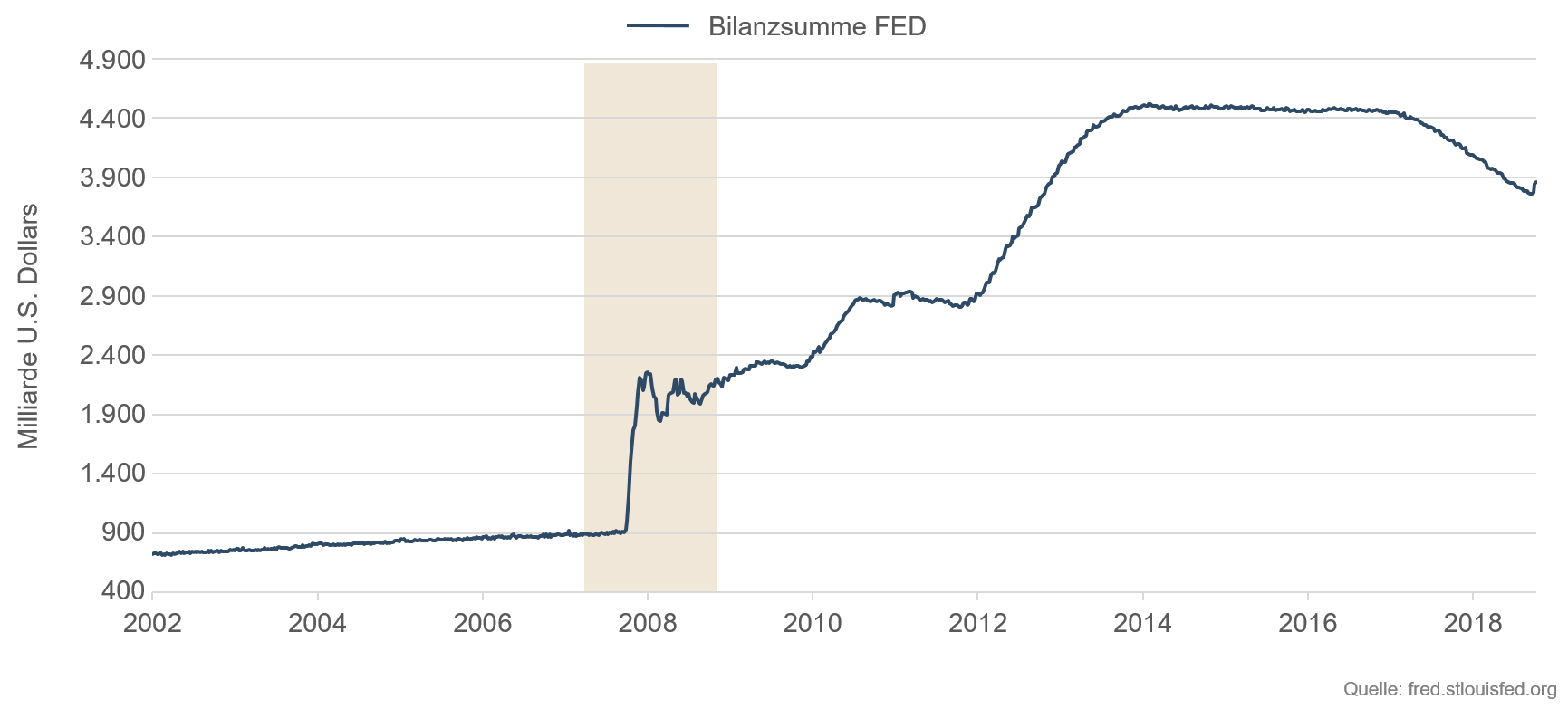

Since the global financial crisis in 2008, central banks in the US, the eurozone, the UK and Switzerland have followed Japan’s lead in providing banks with liquidity by making large-scale securities purchases. At the height of the financial crisis around the time of the collapse of Lehman Brothers investment bank on 15 September 2008, banks were no longer willing to lend money to each other overnight. Liquidity became so expensive, and the lack of confidence in the ability of the borrower to repay became so extreme, that the interbank market was completely paralysed.The purchase of sovereign bonds and other accepted securities held by the banks created central bank money that was made available to the financial institutions. This revived the interbank market and money began to circulate again. Unlike the ECB, the Fed ended its purchase programme back in October 2014, but initially reinvested monies due, and the balance sheet thus remained stable.

But what about this September, 11 years later? Are we seeing another flare-up of systemic risks in the banking sector? Have all the endeavours to recapitalise the banks and make them more secure by imposing higher capital requirements been in vain?

It wasn’t until 2018 that the Fed, under Janet Yellen, deemed the banking market and the US economy strong enough to begin unwinding the asset purchase programme and to reduce its balance sheet, which had grown to USD 4.5 trillion. At the end of August 2019, there was a total of approximately USD 3.8 trillion on the balance sheets of all the US federal reserve banks. In only 20 months, USD 700 billion had been withdrawn from the market. Alongside an increase in the Fed Funds rate from 0% to 2.25% between December 2015 and December 2018, the US central bank had effectively pursued a contractionary monetary policy, which came to an end in 2019 due to the increase in economic uncertainty despite record-low unemployment.

Figure 2: Total Fed assets

Signs point to a liquidity squeeze

The interest rate a borrower pays is made up of various components that together determine the price of the loan: not only is the counterparty default risk a factor but, of course, the lender’s liquidity preference is too. Ultimately, the price also reflects the relative scarcity. Modern financial instruments enable interest rate components to be broken down. The average credit default swap spread for US financial service providers (America Fin Sr IG 5Y CDX), which can be used to estimate the price of default risks in the sector, has only risen by a few basis points. Nor was there the same upheaval in the euro-dollar market – the most important international market for short-term provision of liquidity in USD – as in the US market for overnight repos.

We therefore see no sign of a repeat of the global financial and credit crisis of 2008 in this latest spike in the interest rate for overnight repurchase agreements. In and of itself, bank creditworthiness is not poor. Nevertheless, we see this as a confirmation of our assessment that interest rates will remain low for a prolonged period yet. The Fed’s two key rate cuts by 50 basis points in total since July, alongside the latest upheavals in the US interbank market, are a clear sign of how fragile the banks’ situation, and thus the US economy, is, and especially how unequal the distribution of excess liquidity in the US banking market is.

There is already some debate about whether the Fed will soon commence a fourth round of its purchase programme or activate a “standing overnight repo facility” in order to meet the banking sector’s liquidity requirements. September’s stress in the US overnight interbank market is probably not a signal of a repeat of the banking crisis on 2008’s scale. This was an unfortunate coincidence of regulatory requirements on banks to tidy up their balance sheets periodically at the end of the quarter and the year, an unfavourable tax day combined with US Treasury issuance, as well as a slow-to-react central bank. Having said that, the fact remains that the US and the eurozone will continue to depend on the provision of liquidity by central banks.

Unicorns – the natural enemy of value equities?

Do unicorns exist? ”Yes, they most certainly do!” asserts our Senior Portfolio Manager Christian Schmitt. With their deep pockets and aggressive expansion strategies, they are posing an ever-greater threat to the business models of long-established companies. This causes structural distortion in markets. Find out in our latest video what criteria can steel the Ethna-DYNAMISCH against these distortions.If you are having video playback issues, please click HERE.

Positioning of the Ethna Funds

Ethna-DEFENSIV

In September, investors’ focus was on the ECB and Fed central bank meetings. The ECB and outgoing President Mario Draghi met the expectations of many people and lowered the deposit interest rate from -0.4% to -0.5%. In addition, the ECB announced the re-launch of its asset purchase programme in November at a pace of EUR 20 billion a month. One week later, its US counterpart – the Federal Reserve Bank – reduced the target level for its key refinancing rate to between 1.75% and 2%. This, too, was not unexpected. Nevertheless, long-term interest rates increased surprisingly sharply in the days before and after the decisions. Yields on 10-year Bunds rose from -0.7% to -0.45% and those on 10-year Treasuries climbed from below 1.50% to 1.9%, in less than two weeks. This rise is also the main factor in the Ethna-DEFENSIV’s negative performance for the month in September. Things settled down slightly towards the end of the month, and yields ended September at -0.6% and 1.7%, respectively.

In a world of low interest rates, the interest rate on daily liquidity suddenly exploded in the US. The interest rate for short-term liquidity with a US Treasury as collateral peaked at almost 10% – just two days before the US central bank’s decision on interest rates. This anomaly reflects the lower level of excess reserves in the US banking system, for reasons including the unwinding of the central bank’s balance sheet. Since then, the US central bank has been pumping liquidity into the market on a daily basis in order to tackle the distortion. Other reasons cited for the insufficient liquidity on 16 September were quarterly tax payments by US companies as well as the issuance of Treasuries. Both are certainly events that came as no surprise. On the other hand, the stricter rules for US banks as a consequence of the financial crisis are, in some cases, preventing any existing reserves from getting passed on quickly and efficiently.

It is unclear whether this distortion in the US money market is a factor in the US dollar’s continued stability. However, investors will have given serious thought to when they should stock up on their USD for quarter-end. This will certainly have stimulated demand. The value of the CHF has risen in step with the USD even though there is no liquidity squeeze in Switzerland. The first steps towards the impeachment of President Trump have been taken, and this has doubtless spread general uncertainty. Even though these recent developments have to date only marginally shored up the strength of our preferred currencies CHF and USD, we are even more confident at the moment that these currencies have further potential to gain against the EUR.

Based on this conviction, we have allocated a higher weighting to the existing USD and CHF positions. We have reduced the risk allocation elsewhere. Given that long-term yields have been steadily falling for almost 12 months now, in the short term we rather expect yields to consolidate at a low level. For that reason, we have completely reversed our position in Treasury futures and thus reduced portfolio duration further. Apart from these changes, we are continuing to systematically rotate out of European corporate bonds yielding close to zero and into bonds denominated in USD. In our opinion, the yields on these are still attractive.

Ethna-AKTIV

Central banks, including the ECB and the Fed, met again in September, and their statements were followed by many investors. As expected, the European Central Bank under outgoing President Mario Draghi lowered the deposit interest rate by 10 basis points to -0.5% and announced the launch of a new asset purchase programme amounting to EUR 20 billion a month starting in November. Fed Chair Jerome Powell, too, coming under pressure from President Trump, announced a rate cut, which, at 25 basis points, was as expected. While the outcomes of the meetings in and of themselves held no surprises, interest rate movements before and after the meetings were surprisingly strong. Both the yield on the 10-year German Bund and that of its US counterpart hit record lows for the year to date at the beginning of the month, before rising sharply over a two-week period. Investors who had been running a long portfolio duration had benefited from the steady decline in interest rates this whole year so far, and this now came to an abrupt end, including for us. The same occurred as a result of a sudden rotation for this year’s stand-out factor and sector strategies within equities. While the broad indices revealed almost nothing, momentum equities, for instance, and the spread between cyclical and defensive securities, sustained heavy losses in some cases due to rotation into other sectors or factors. Our portfolio escaped this, since at the moment we are only invested at the index level.

September was eventful on the geopolitical front, too. The attack on two Saudi Arabian refineries not only put the sensitivity of the price of oil to the test, but also clearly demonstrated that there are forces in Iran that are willing to escalate the current situation. On the supply side of the oil market, there is capacity to make up for these production losses relatively quickly; what is more unsettling for us, however, is the new sort of escalation in the Middle East. What the parties involved do next will have to be observed closely. Meanwhile, the Brexit drama also entered the next stage. The Supreme Court’s ruling that the prorogation of Parliament was unlawful dealt Prime Minister Boris Johnson another setback, and the roadmap for an orderly exit of the UK from the EU remains unclear. Fresh talks in the trade conflict between the US and China, which has been ongoing now for more than a year and a half, are scheduled for mid-October. At the moment, the market seems to regard even a mini-deal – leaving out key elements, such as how to deal with intellectual property – as a success. Should the tariffs imposed during the conflict be suspended, we would join this state of euphoria for a time and take any opportunities that arise. However, we still strongly doubt that there will be a comprehensive solution covering all points of contention.

These developments have prompted us to balance out the portfolio a bit more. We have successively increased the equity allocation, as we assume that much of the aforementioned bad news has already been priced in and there is potential for upside surprises rather than downside. On the other hand, we are reducing our duration in favour of assigning a higher weighting to the existing USD and Swiss franc positions. While interest rates have already fallen markedly in the past 12 months and we expect the current consolidation to continue, both invested currencies have a tendency to remain strong. Apart from these changes, we continue to systematically rotate out of European corporate papers yielding close to zero and into US bonds, whose yields we still find attractive.

Ethna-DYNAMISCH

If both players in a game of chess see no way of winning, they agree to a draw. But such a stalemate will never arise in the stock market, as prices either rise or fall. There are plenty of arguments at the moment for optimists and pessimists to justify their positioning. Valuations are, in some cases, ambitious but, on the other hand, interest rates are very low. The economy continues to weaken but, on the other hand, central banks are supportive. This is a classic draw situation. In August, we wrote, “The foundation for bottoming out and an end to the lack of trend has been laid.” Indeed, prices rose sharply at the end of August and the beginning of September, in some cases so sharply that we found ourselves, at least temporarily, in slightly overbought territory. The impetus for this rise came from the central banks in Europe and the US, which consistently implemented the announced monetary easing. The economic situation remains moderate. Europe’s most important economy – Germany – is facing a few challenges. Manufacturing is again weak and the profit warnings for small and mid-sized companies go on and on. Calls for government economic stimulus packages are getting louder and are certainly being heard by politicians. Here, too, Germany is a role model within Europe, as a budget surplus means available reserves. The US generally has fewer reservations about government economic stimulus packages. President Trump cannot afford to have a sustained flagging economy, with next year being a presidential election year. For that reason, we expect him to do everything in his power to support the US economy by suitable means. The monetary easing that has already been implemented together with any upcoming fiscal measures could prevent a deep recession. Investors don’t like talk of recession, but at least some parts of the world will not be able to completely avoid it.

On the equities side, we are currently positioned in the middle; that is, we have purchased mainly equities whose business models are not linked to the economy and which are fairly valued. We are cautious about highly cyclical exposures on account of the fragile economy. In some cases the prices of growth segment equities are overdone, so for the time being we plan to make no major investments here. In September, we closed the position in the Japanese engineering company SMC Corp. The stock made strong gains in recent weeks and the chart shows a flagpole formation. The increase was not associated with fundamental increases in profits, which makes the share too expensive. Many SMC customers are in the semi-conductor sector, which is highly cyclical and would be directly affected by the coming downturn. We made no additional purchases in September.

Following the strong price rise in equity markets at the beginning of the month, we expanded the futures hedging and, at the same time, reduced the options. The net equity allocation is thus slightly lower, and at the end of September was just over 50%.

After abstaining for a number of months, we built up our bond portfolio once again with a single position. We purchased a BASF convertible bond in USD with a 2023 maturity and a yield slightly above 2%. The appeal of the bond is the convertible component, which is currently priced at zero by the market, i.e. the bond is trading at the same yield level as other BASF bonds without the conversion option.

Even though we have slightly reduced the equity allocation in the short term, we see good opportunities for share prices to rise further in the medium term and we are optimistic about the fourth and final quarter of the year.

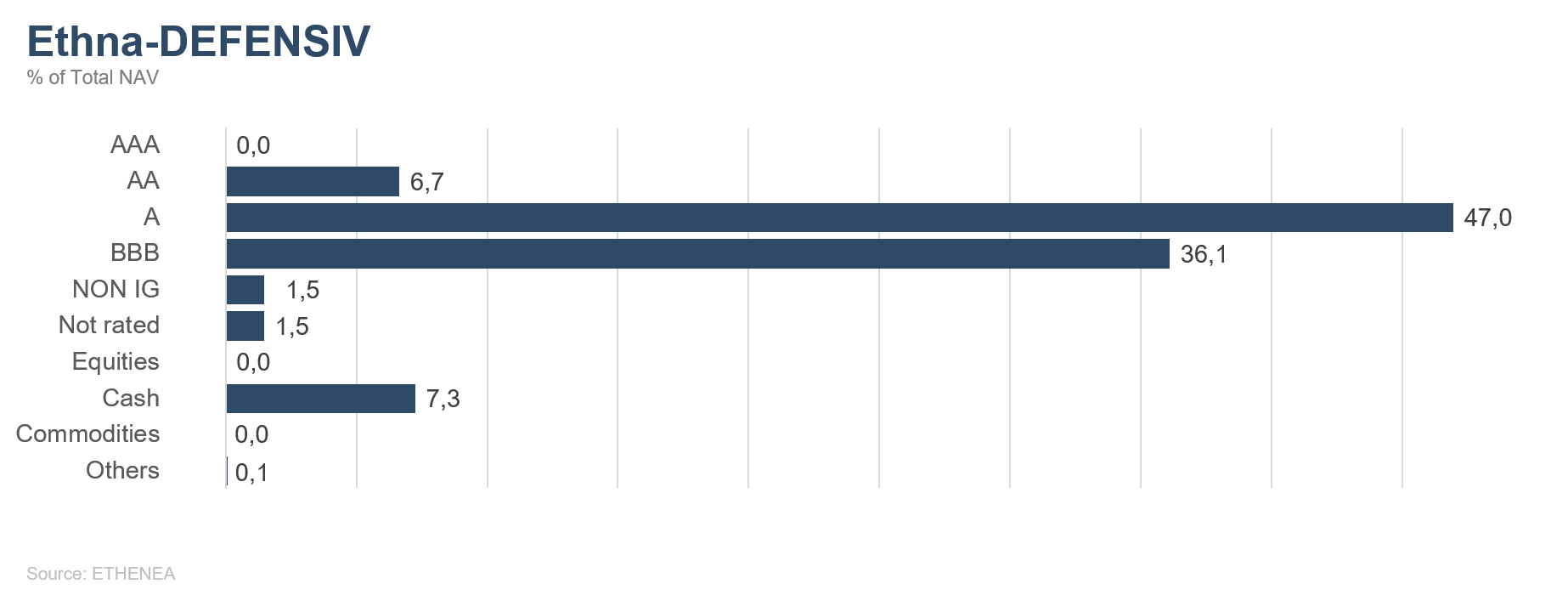

Figure 3: Portfolio structure* of the Ethna-DEFENSIV

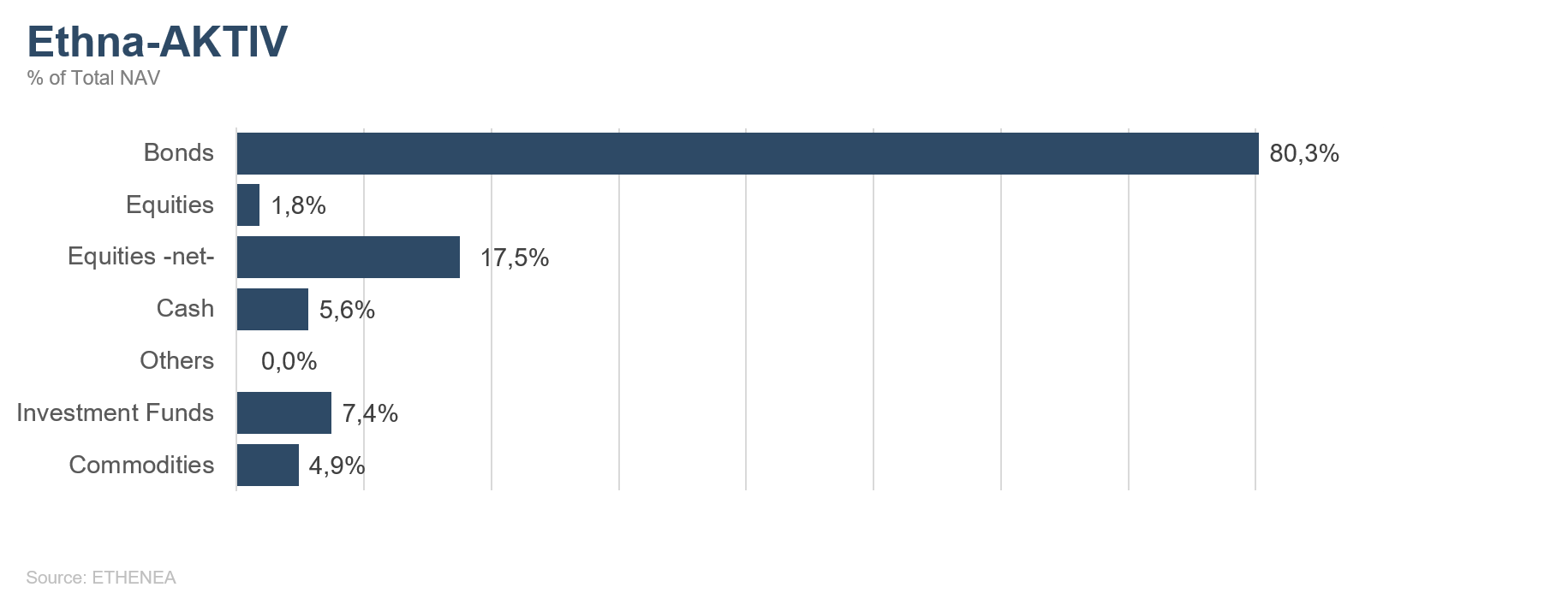

Figure 4: Portfolio structure* of the Ethna-AKTIV

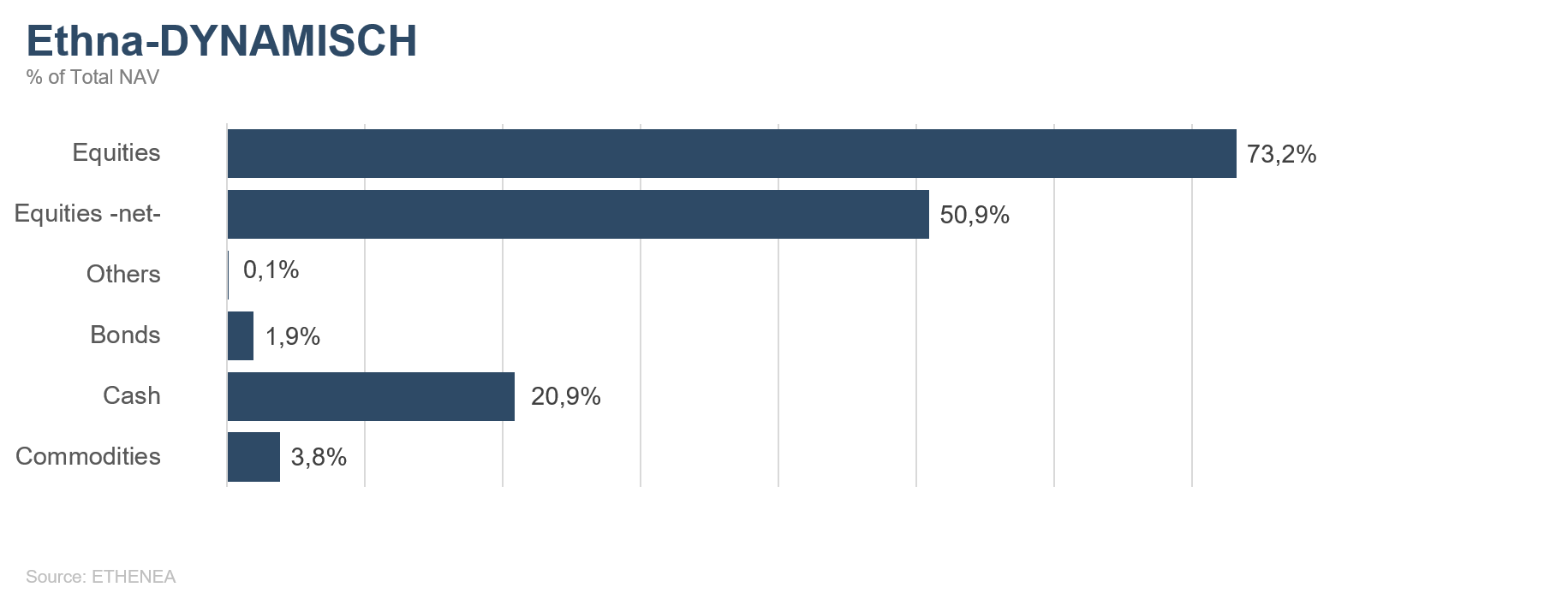

Figure 5: Portfolio structure* of the Ethna-DYNAMISCH

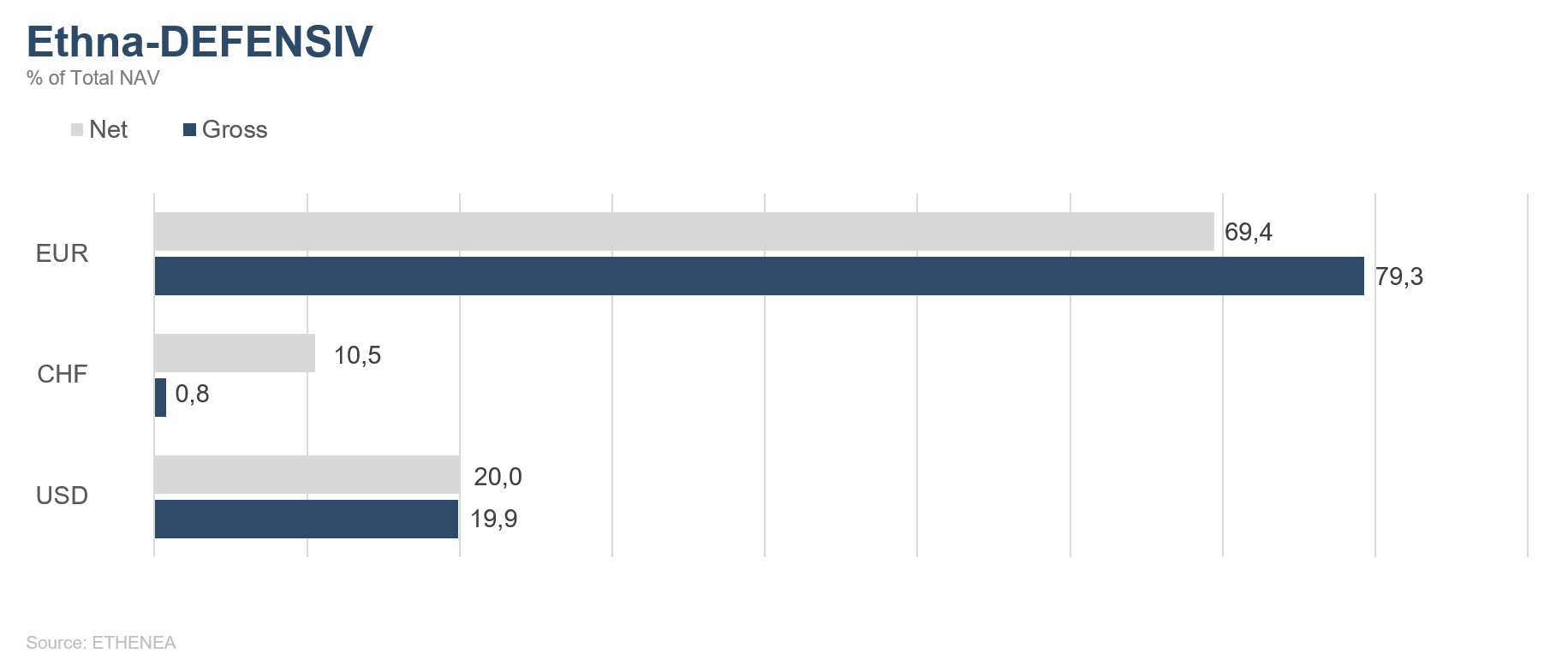

Figure 6: Portfolio composition of the Ethna-DEFENSIV by currency

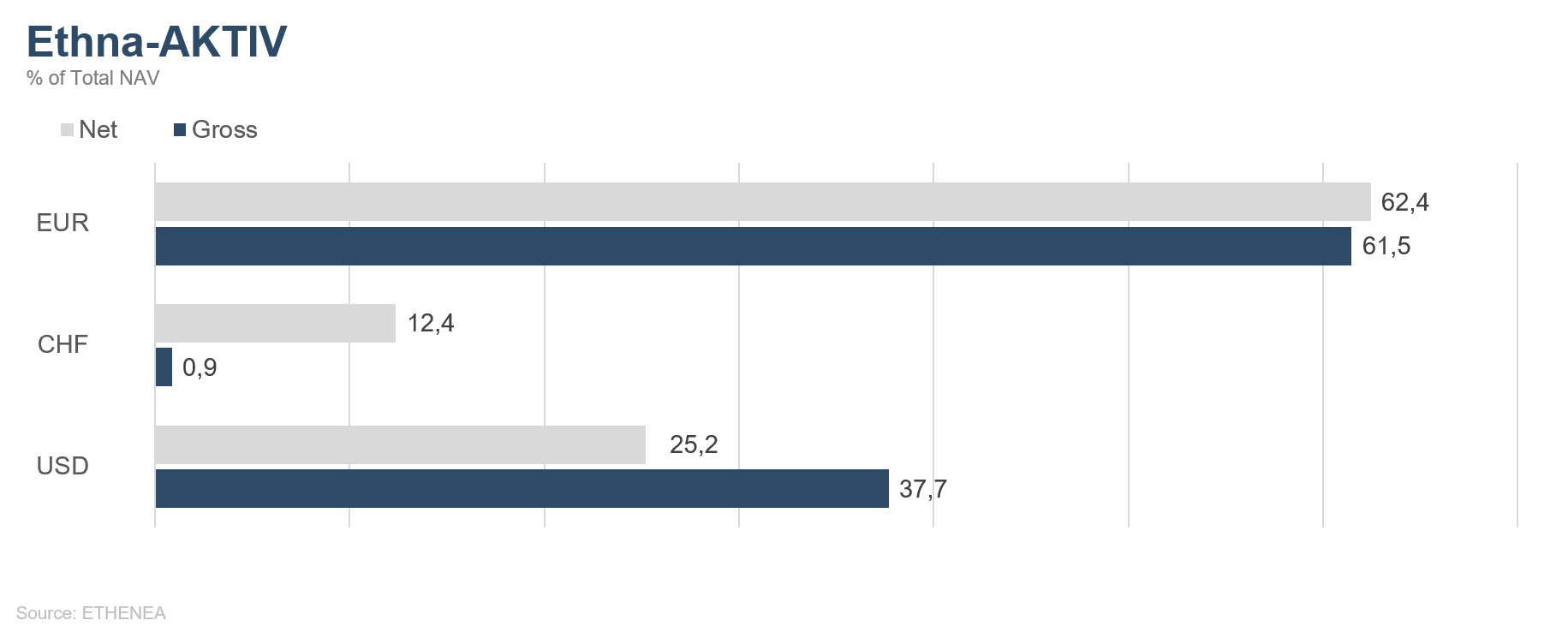

Figure 7: Portfolio composition of the Ethna-AKTIV by currency

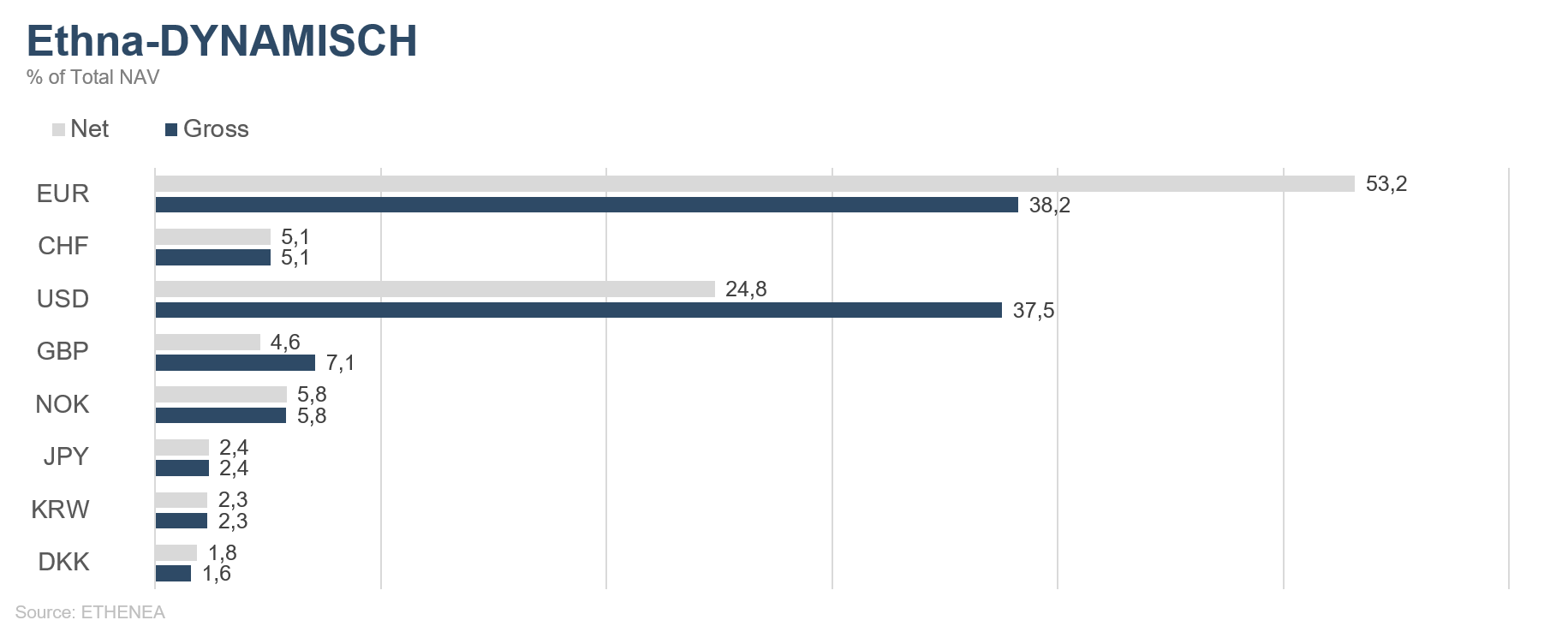

Figure 8: Portfolio composition of the Ethna-DYNAMISCH by currency

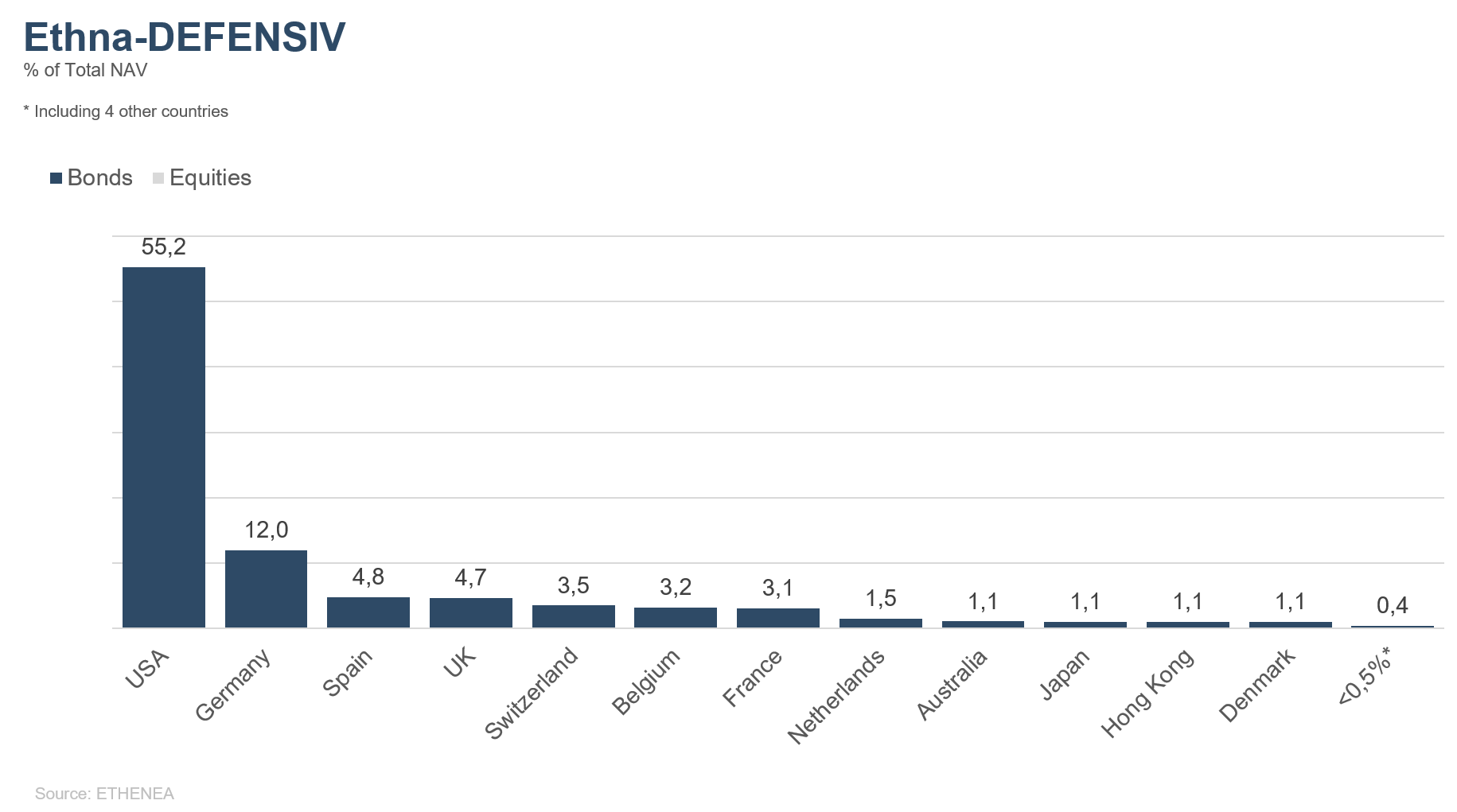

Figure 9: Portfolio composition of the Ethna-DEFENSIV by country

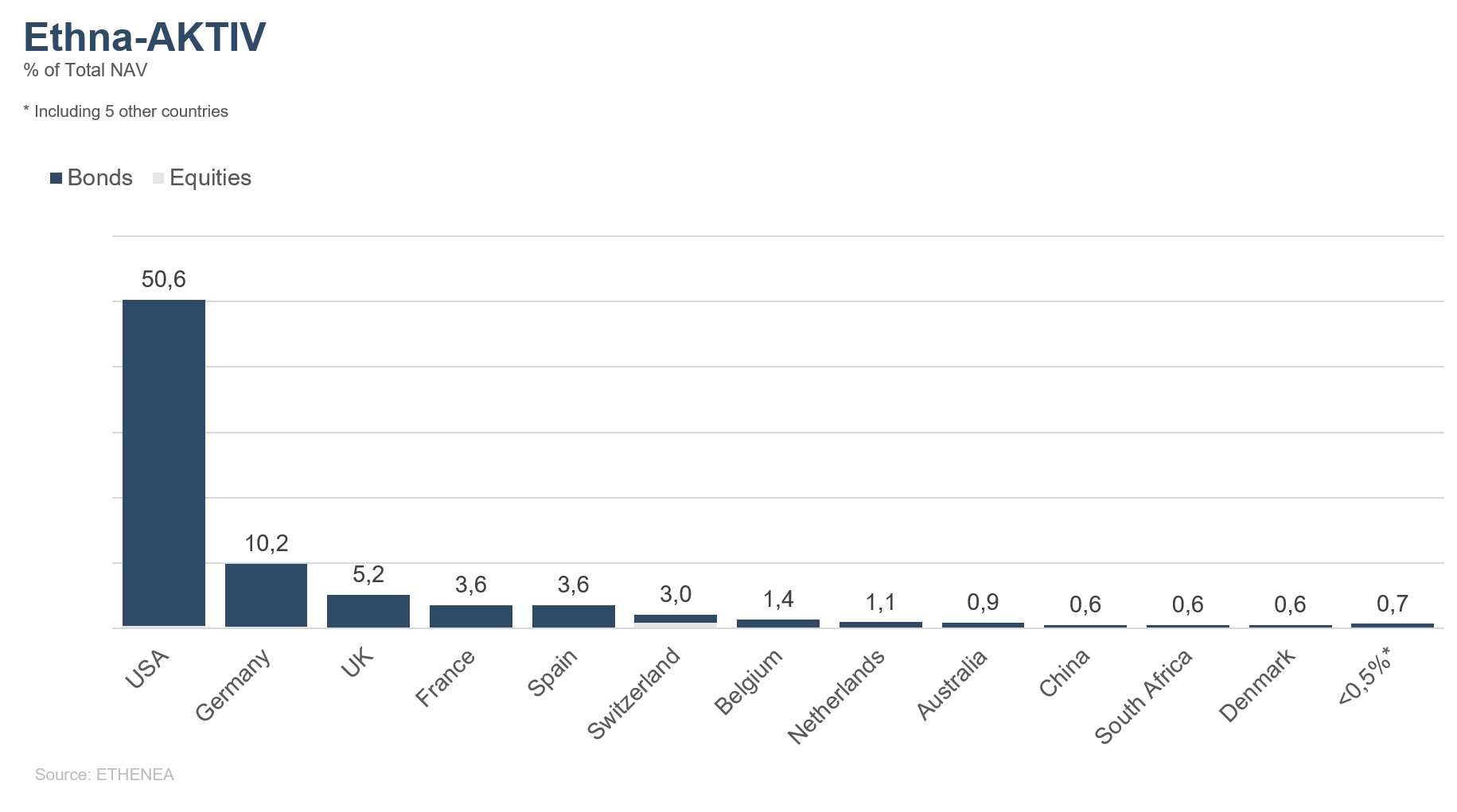

Figure 10: Portfolio composition of the Ethna-AKTIV by country

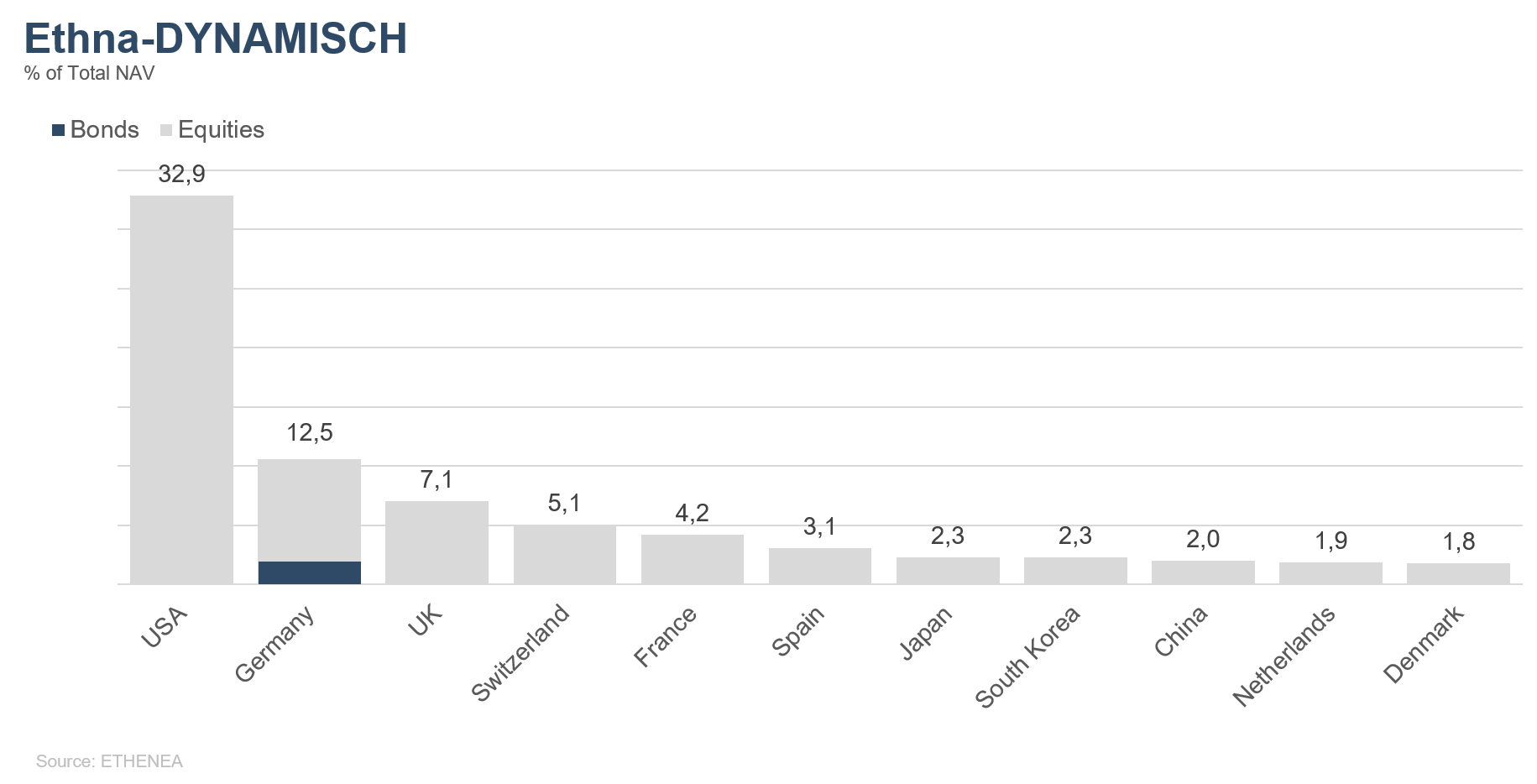

Figure 11: Portfolio composition of the Ethna-DYNAMISCH by country

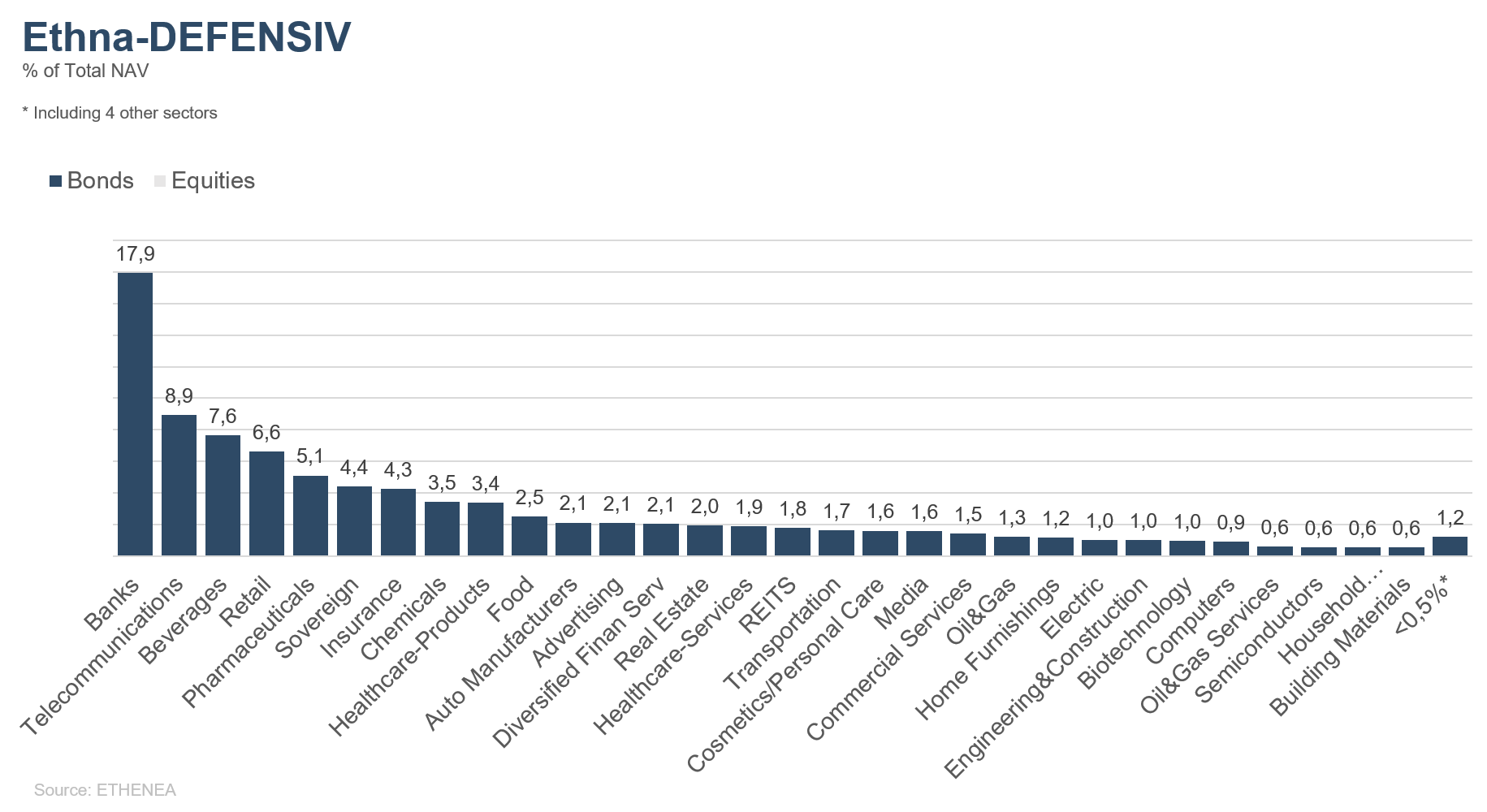

Figure 12: Portfolio composition of the Ethna-DEFENSIV by issuer sector

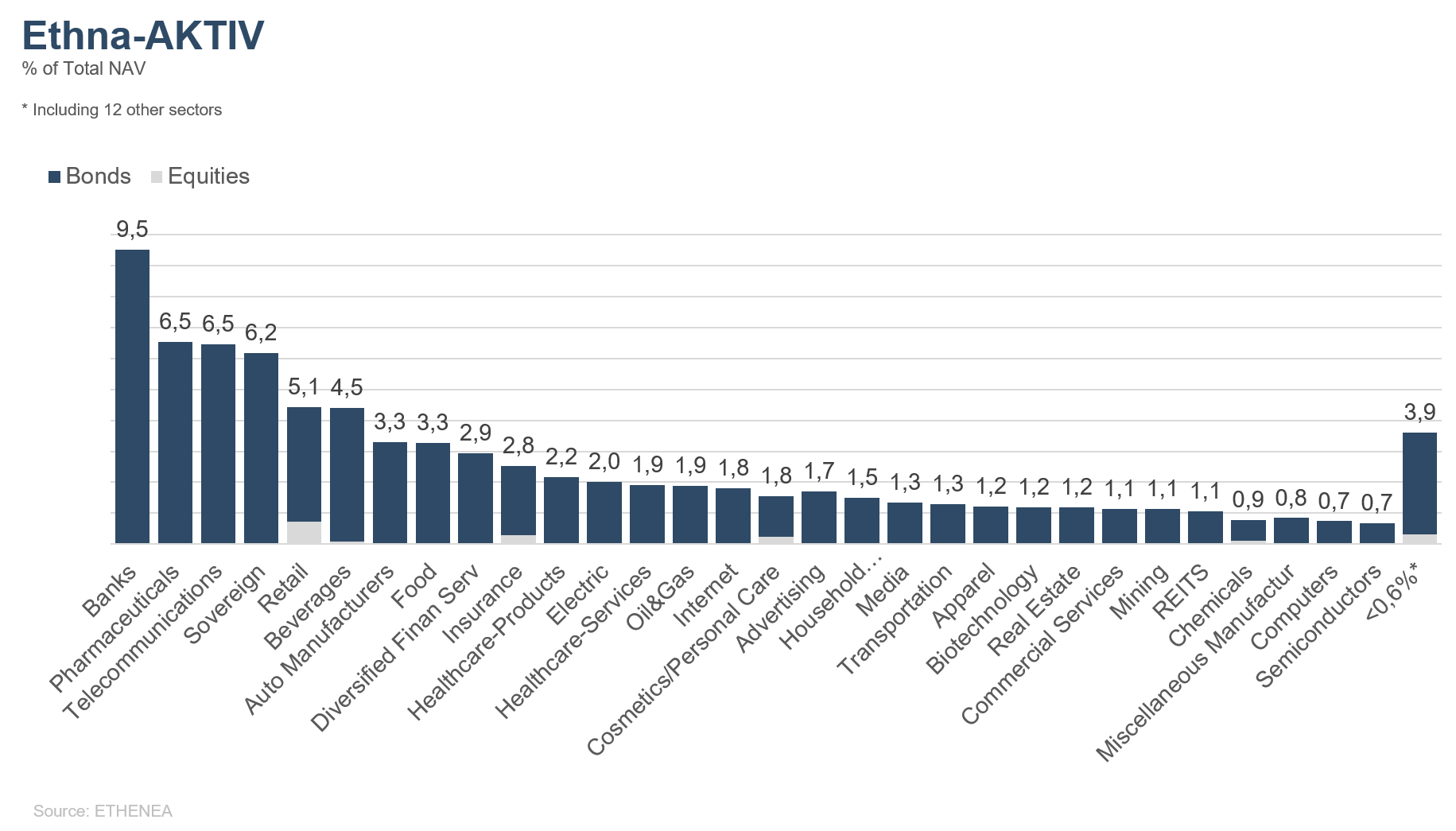

Figure 13: Portfolio composition of the Ethna-AKTIV by issuer sector

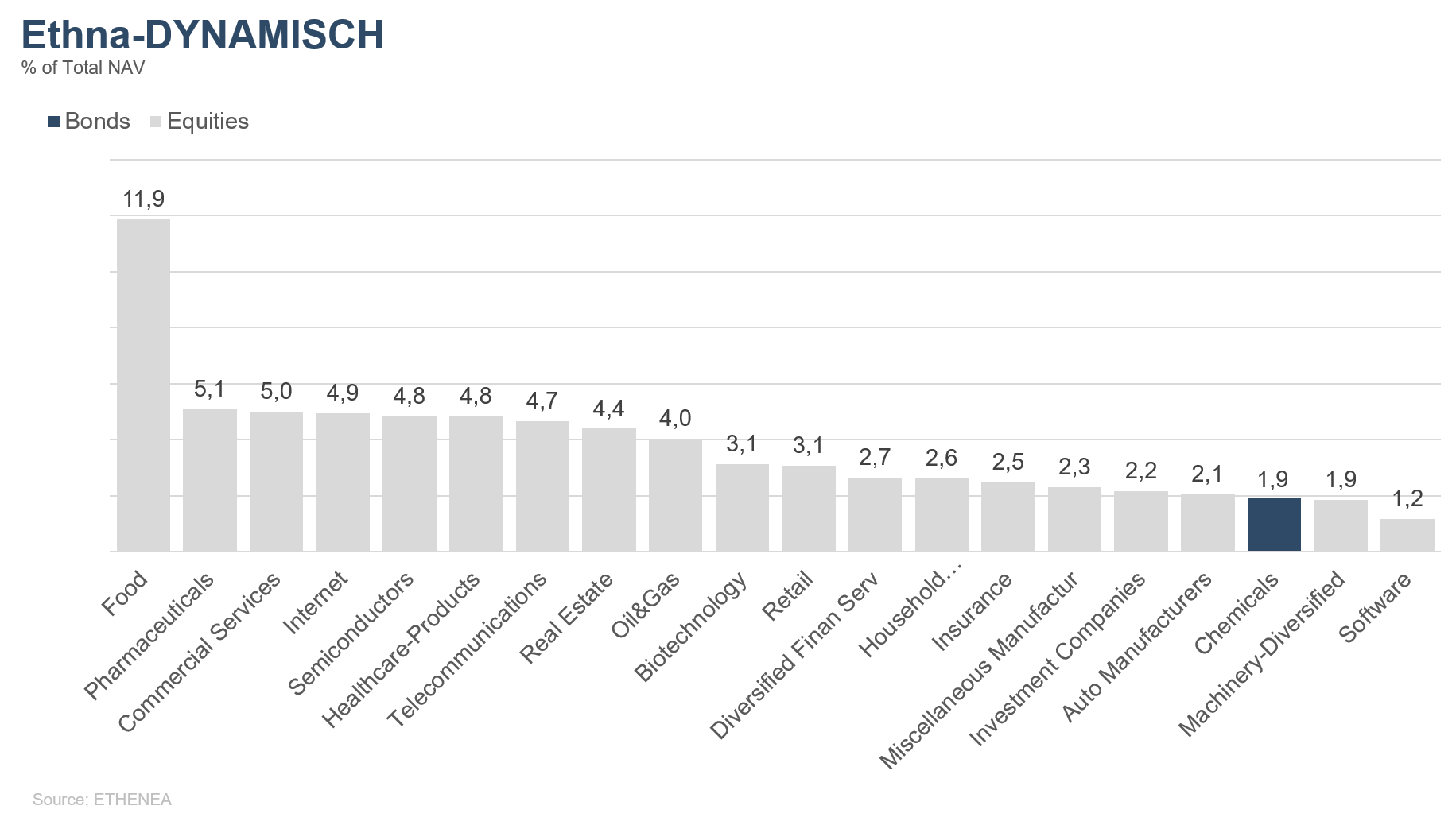

Figure 14: Portfolio composition of the Ethna-DYNAMISCH by issuer sector

* “Cash” comprises term deposits, call money and current accounts/other accounts. “Equities net” comprises direct investments and exposure resulting from equity derivatives.

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

This marketing communication is for information purposes only. It may not be passed on to persons in countries where the fund is not authorized for distribution, in particular in the USA or to US persons. The information does not constitute an offer or solicitation to buy or sell securities or financial instruments and does not replace investor- and product-related advice. It does not take into account the individual investment objectives, financial situation, or particular needs of the recipient. Before making an investment decision, the valid sales documents (prospectus, key information documents/PRIIPs-KIDs, semi-annual and annual reports) must be read carefully. These documents are available in German and as non-official translations from ETHENEA Independent Investors S.A., the custodian, the national paying or information agents, and at www.ethenea.com. The most important technical terms can be found in the glossary at www.ethenea.com/glossary/. Detailed information on opportunities and risks relating to our products can be found in the currently valid prospectus. Past performance is not a reliable indicator of future performance. Prices, values, and returns may rise or fall and can lead to a total loss of the capital invested. Investments in foreign currencies are subject to additional currency risks. No binding commitments or guarantees for future results can be derived from the information provided. Assumptions and content may change without prior notice. The composition of the portfolio may change at any time. This document does not constitute a complete risk disclosure. The distribution of the product may result in remuneration to the management company, affiliated companies, or distribution partners. The information on remuneration and costs in the current prospectus is decisive. A list of national paying and information agents, a summary of investor rights, and information on the risks of incorrect net asset value calculation can be found at www.ethenea.com/legal-notices/. In the event of an incorrect NAV calculation, compensation will be provided in accordance with CSSF Circular 24/856; for shares subscribed through financial intermediaries, compensation may be limited. Information for investors in Switzerland: The home country of the collective investment scheme is Luxembourg. The representative in Switzerland is IPConcept (Suisse) AG, Bellerivestrasse 36, CH-8008 Zurich. The paying agent in Switzerland is DZ PRIVATBANK (Suisse) AG, Bellerivestrasse 36, CH-8008 Zurich. Prospectus, key information documents (PRIIPs-KIDs), articles of association, and the annual and semi-annual reports can be obtained free of charge from the representative. Information for investors in Belgium: The prospectus, key information documents (PRIIPs-KIDs), annual reports, and semi-annual reports of the sub-fund are available free of charge in German upon request from ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxembourg, and from the representative: DZ PRIVATBANK AG, Niederlassung Luxemburg, 4, rue Thomas Edison, L-1445 Strassen, Luxembourg. Despite the greatest care, no guarantee is given for the accuracy, completeness, or timeliness of the information. Only the original German documents are legally binding; translations are for information purposes only. The use of digital advertising formats is at your own risk; the management company assumes no liability for technical malfunctions or data protection breaches by external information providers. The use is only permitted in countries where this is legally allowed. All content is protected by copyright. Any reproduction, distribution, or publication, in whole or in part, is only permitted with the prior written consent of the management company. Copyright © ETHENEA Independent Investors S.A. (2025). All rights reserved. 02/10/2019