Sell in May but don’t stay away!

True to the old financial-world adage “Sell in May and Go Away”, last month marked the start of a difficult period for global equity markets. Almost no sooner had the month began than there was activity on the most famous Twitter account in the world, causing a headache. Contrary to the general expectation that the trade conflict between the US and China would soon be resolved, President Trump announced his intention to hike tariffs on certain Chinese imports. The Chinese government promptly responded with its own increases in tariffs on US exports to China. As a result, the S&P 500 index slipped 4.5% and Chinese equities fell by more than 7% at the beginning of the month. In that respect, the old saying proved true.

However, not only the US and its high-profile Twitter user but also the Chinese, too, have no interest in much lower share prices. Hence the overtures – at least from the Americans – to a meeting of Presidents Trump and Xi at the G20 summit at the end of June, which could pave the way for an agreement. A Chinese delegation even went as far as Washington to negotiate the terms of a deal. On the other hand, the Chinese telecommunications giant Huawei has got caught up in the dispute. US suppliers now have to apply for exemptions to enable them to continue supplying to Huawei. This is strikingly similar to the situation with Iranian oil exports. In this instance, too, consumer nations (China, India, Korea and others) had to obtain waivers to continue to import Iranian oil, or else incur US sanctions. These waivers expired at the beginning of May and have not been extended.

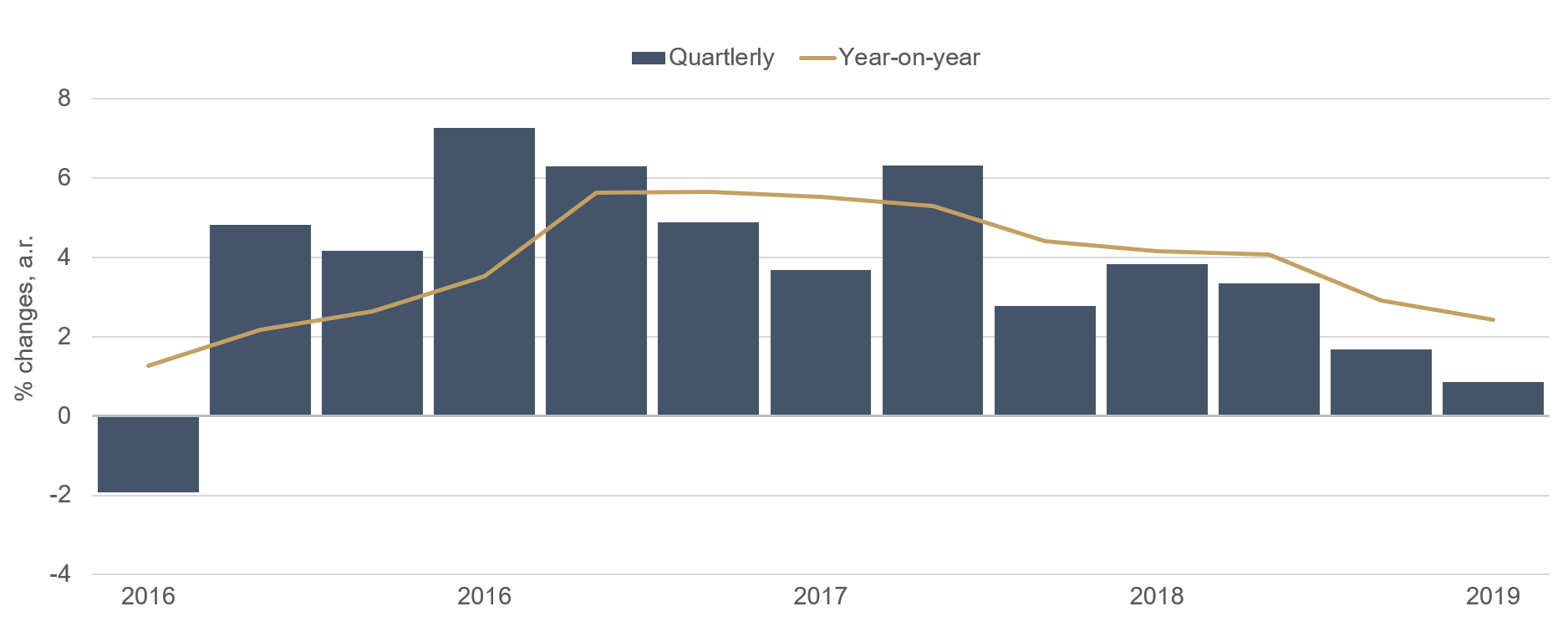

However, there is also positive news about global trade. The US has again cut import tariffs on Turkish, Mexican and Canadian steel. And the decision on higher US tariffs on car imports from Europe and Japan has been shelved for the time being. This is likely to be met with temporary relief but we are certainly not totally in the clear yet. Given such uncertainty and how little planning security there is, it’s no surprise that global trade growth is just hovering above zero in the first quarter of 2019 by the OECD’s reckoning.

Figure 1: Global trade growth¹

There’s no sign of any progress in the UK either. Up until very recently, Theresa May was still desperately trying to get some version of her Brexit deal with the EU through parliament. Now she’s announced that she will step down at the beginning of June. In the wake of her Tory party’s disastrous European election results, the search for a successor has begun. Whoever it is will find it just as difficult as their predecessor because Brexit and what form it will take is splitting party and country alike. The winners in the European elections were Nigel Farage’s new Brexit Party, which is in favour of a hard Brexit, as well as the Liberal Democrats and the Greens, both of which oppose Brexit. It will be hard to find a solution. Nor is the mood going to improve with Jamie Oliver’s restaurant chains going into administration and the collapse of British Steel. The nonetheless solid growth of the UK economy at the beginning of this year was probably more to do with the stockpiling to cover all possible variants of Brexit than anything else. This is not what healthy economic development looks like. Only when it comes to football has the UK maintained its dominance and this is perhaps clouding many people’s vision of current problems.

Only Klopp – the Normal One – seems able to stop the UK’s exit from Europe. Who wants to see it come to a point where the Liverpool manager – who is so popular both in Germany and in the UK – has no work permit? Not me, for one. But it is becoming increasingly likely that Jürgen Klopp will eventually follow in the footsteps of Mourinho – the Special One – and seek his fortune outside of the UK, as Farage and his Brexit hardliners ultimately steer the UK to a hard Brexit. At any rate, Remainers were unable to agree on a joint candidate for a by-election in Peterborough. This does not exactly show solidarity, which is so desperately needed.

Despite these frustrating circumstances, global equity and bond markets have only reacted to a slight extent. This is due to the fact that services markets continue to grow strongly in the major economies around the world as well as the steady rise in wages and the expectation that the Federal Reserve and ECB central banks will remain supportive. “Sell in May” has, in fact, come true and the broad S&P 500 index lost around 4.5% at the beginning of the month. However, one should be careful about “going away/staying away” because the S&P 500 has regained 2% in the meantime, in the knowledge that the company earnings situation and the financing conditions remain good. The first quarter reporting season showed that companies both in the US and in Europe continue to report solid earnings, which if anything are slightly higher year-on-year. In any case there is no need to stick one’s head in the sand and stay away from equity markets for the next few months. Interesting situations will arise from time to time that require a new way of thinking. Who would have thought that Renault and Fiat would contemplate a merger and both stock exchanges and politicians would be enthusiastic?

Bond markets in the US have repeatedly signalled recession. The 10-year US Treasury yield has again fallen below the three-month government debt yield. However, this anomaly in the yield curve can certainly be attributed to supply to a great extent. In the first four months of the year, the Treasury Department issued more than USD 4 trillion in bonds. Of that, however, only USD 177 billion were long-dated 10- to 30-year bonds; that is, only 4.4% of total issuance. Therefore, the US Treasury’s pattern of issuance is likely to have been conducive to the yield curve inversion. Since there are no plans to change that, this continues to justify low long-term interest rates.

In the end, a few tariffs more or less will not have a lasting impact on global trade. However, companies need planning security. As long as they don’t have that, companies will refrain from making large investments. Therefore, many of them are currently working on optimising their internal operations. However, one can hardly expect any costly bad investments to be made here. May has once again turned out to be a difficult month for stock markets but there is no call for a long abstinence, as there is much too much support from central banks for that and one can well imagine the US Federal Reserve ending its balance sheet run-off early. And perhaps our VIP Twitter user will even soon use conciliatory language on his favourite channel. Of course, there’s also the possibility of de-escalating the trade dispute in a traditional face-to-face meeting between Presidents Trump and Xi during the G20 summit at the end of June.

The comeback of the trade war

The trade war between the US and China again escalated in May, not without consequences for global capital markets. Frank Borchers, Senior Portfolio Manager at ETHENEA, explains in our latest video what effects the dispute is having on corporate bonds, in which the Ethna-AKTIV predominantly invests.If you are having video playback issues, please click HERE.

Positioning of the Ethna Funds

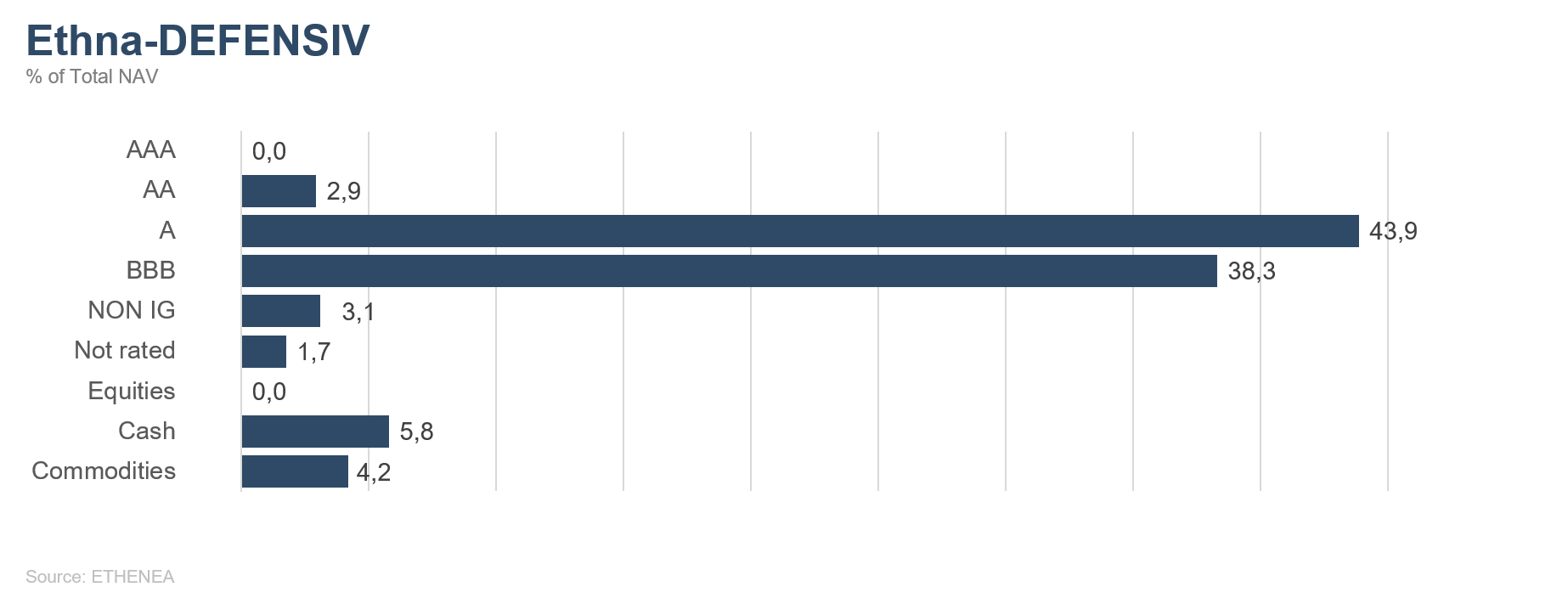

Ethna-DEFENSIV

No sooner had the month of May begun than the trade dispute between China and the US re-escalated, resulting in higher tariffs, initially on the US side and then on the Chinese side. Furthermore, a 5% tariff will shortly be levied on Mexican exports to the US, which is set to increase to 25% by October if the Mexican government does not do more to stop the inflow of immigrants into the US. All this has again stoked fears of an impending global recession. Equities therefore fell sharply in May and the price of oil dropped back considerably from its highs due to the concerns about growth. The 10-year US Treasury yield has again fallen below the three-month government debt yield. Yields on 10-year German sovereign bonds are also down sharply.

The Ethna-DEFENSIV’s bond portfolio benefited considerably from falling interest rates on account of the high duration of 6.3. Duration was further increased, to 8.3, using US Treasury futures and this was a significant contributor to the fund’s overall positive performance in May (+0.10%). The widening of corporate bond spreads only had a marginal effect on fund performance. We are primarily invested in high-quality corporate bonds where spread widening is well in check. In addition, USD-denominated bonds now account for one quarter of the bond portfolio. While spread widening and the interest-rate movement balanced out in the case of EUR-denominated bonds, the balance was tipped in favour of interest-rate movement in the case of USD. Through consistent risk management, we reduced the equity allocation to 4% in the downturn and thus limited the losses. We sold off all our oil certificates. The unchanged gold position of 4% was a positive contributor to performance for the month.

We are confident that the better growth in the US will strengthen the US dollar in the foreseeable future, so we increased our US dollar position slightly during the month to 25% (primarily via bonds). The results of the European elections are another reason for us to do so, even though the overall value of the USD versus the EUR hardly changed at all in May.

If trade relations between China and the US ease or growth prospects stabilise in the long term, the time would be right for the Ethna-DEFENSIV to take on more risk again; e.g. via a higher equity allocation. For the moment, however, and for as long as the outlook for global trade remains dim due to constant hikes in tariffs and attacks on individual companies, we are sticking with our focus on US Treasury futures and high-quality corporate bonds. The addition of gold to the mix should also continue to contribute to fund performance.

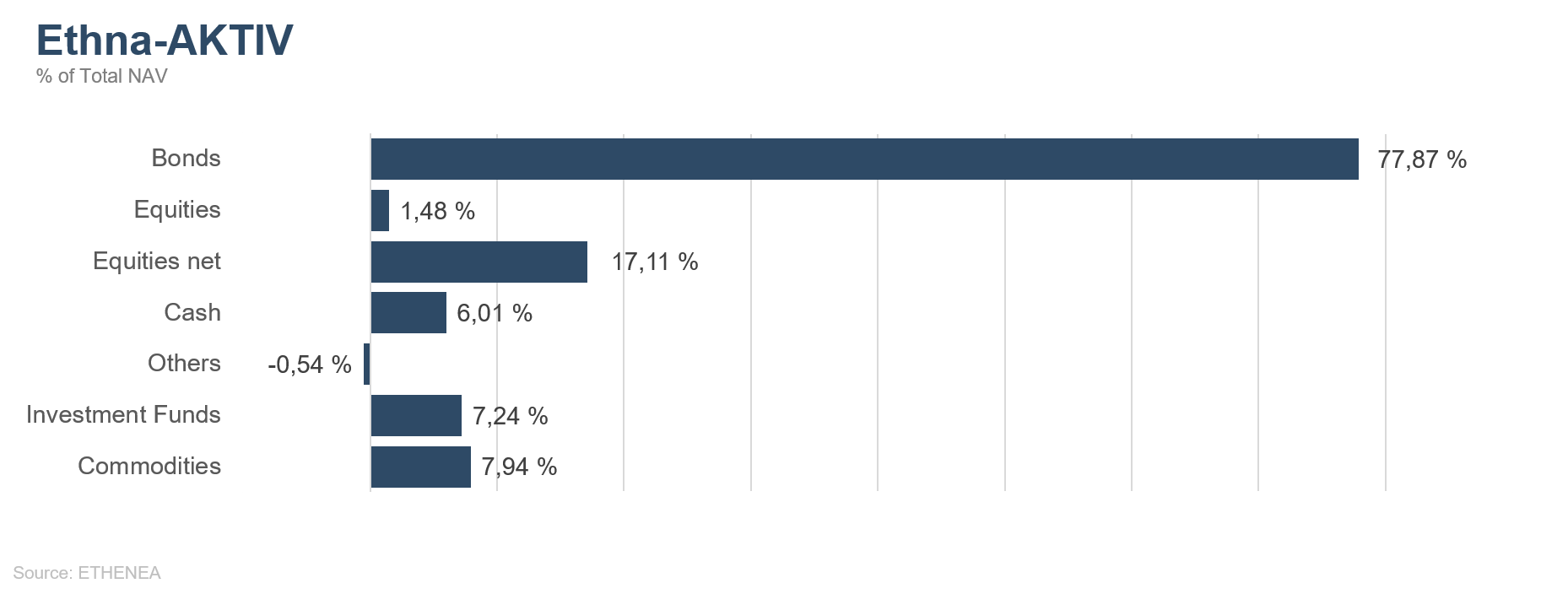

Ethna-AKTIV

Market sentiment – which we felt was overly positive last month – was put to a direct test over the course of the month. The abrupt escalation of the trade dispute between the US and the People’s Republic of China led very quickly to a risk-off phase, in which both equities fell and bond spreads rose, especially those of riskier bonds in the high-yield segment. By contrast, secure sovereign bonds benefited. 10-year US Treasury yields fell from 2.50% to 2.13%. Yields on comparable German sovereign bonds fell from 0.00% to -0.20%. A drop in yields of this magnitude can’t really be regarded as positive in light of the growth outlook. This is reinforced by leading indicators, such as the Purchasing Manager Index in the US and the Ifo Business Climate Index in Germany, which were worse than expected. We assume that both the US central bank’s actions and the progression of trade hostilities will play a key role in the future direction of growth. At the moment, the Fed is adopting a wait-and-see attitude and the trade dispute is not expected to be resolved soon.

Due to the high duration of 6.3 within the Ethna-AKTIV’s bond portfolio, we were able to benefit from falling interest rates. A further increase in the duration to 8.6 using interest-rate futures was a positive contributor to performance. High-quality corporate bonds had a stabilising effect on the portfolio: these now make up ¾ of the overall portfolio. Through consistent risk management, we reduced the equity allocation to 17% in the downturn and thus limited the losses. We reduced the oil exposure to 2.5%. We still hold a US dollar position of 30% (primarily via bonds) and this is an indicator of our firm conviction that better growth in the US will strengthen the dollar in the foreseeable future. The results of the European elections unsurprisingly showed that anti-European parties have gained ground, and this only serves to confirm our opinion. Overall, the portfolio lost 1.11%, with the contribution from the bond portion going some way to make up for the losses on equities and oil. Our gold position is now back at 5% but it made no contribution to performance in the month of May.

As soon as signs re-emerge of an easing of tensions on the trade front or the prospects of a more stable growth environment increase, we will once again be prepared to take on more risk in the portfolio, especially by expanding the equity exposure.

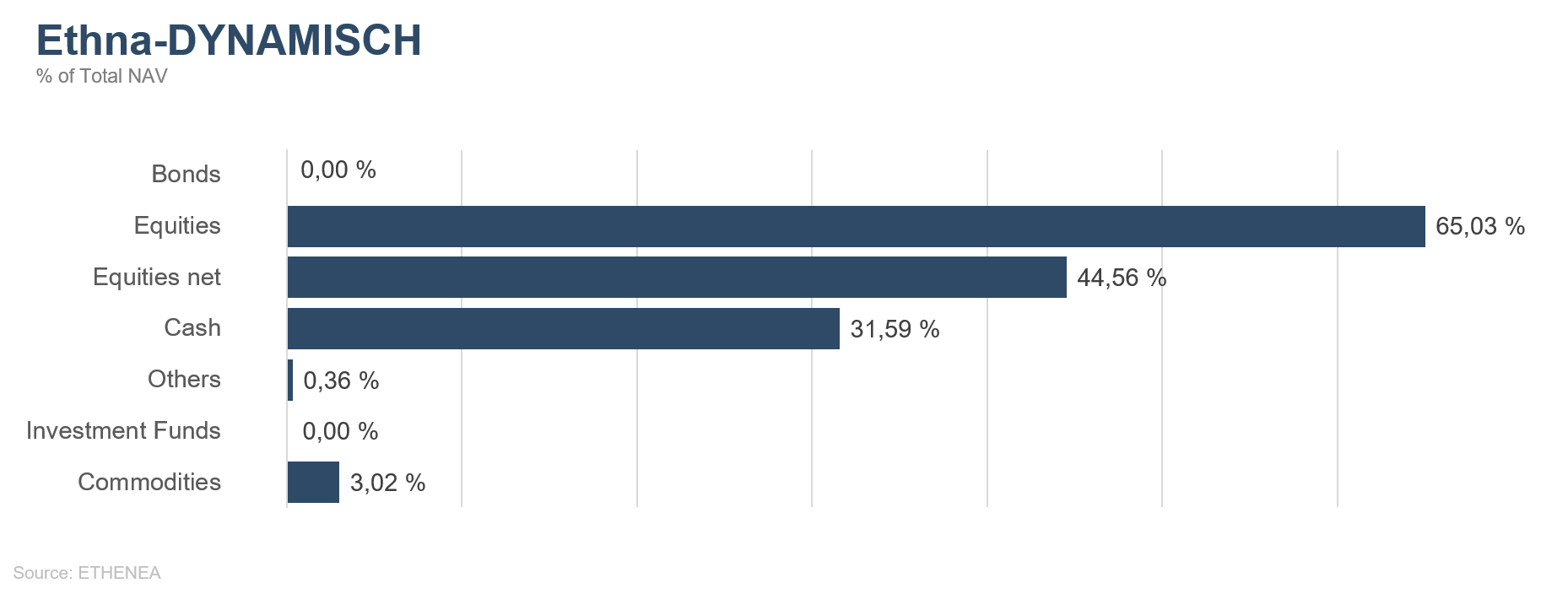

Ethna-DYNAMISCH

May was a damp squib and not just in terms of the weather. Conditions got much harsher in global equity markets last month as well. There was a sudden change in the weather, much like one sees in the mountains. What changed over the course of the month was not so much the news itself but more so the manner in which news was interpreted by market participants and translated into action. While in the first four months the emphasis was constantly on the positive factors, in recent weeks there has been a tendency to focus on the fly in the ointment. First and foremost, markets were preoccupied by the ongoing trade war between the US and China. The attitude that “it will all be alright in the end” gave way to a new baseline scenario where the outcome of the confrontation has become much more uncertain.

In this environment of heightened uncertainty, two aspects remain essential for us: firstly, quite apart from the daily distraction of individual Tweets, we must keep our eye on the fundamental developments. Secondly, the analysis of sentiment ‒ that is, of investor mood and positioning – is a valuable source of advice at present. Combining both can allow us to draw helpful conclusions as to potential opportunities and risks.

Based on the fundamental developments, we believe opportunities still outweigh the risks, especially in the case of high-quality single stocks. While growth expectations for the global economy still have to be successively revised downwards we do not yet see any signs of a self-perpetuating downward spiral. On the contrary, there are plenty of signs that fuel hopes of a foreseeable end to the dip in growth. The heavy going we encountered in the earlier stages of the current economic cycle is likely to return with a vengeance in the future. Experience shows that this is by no means a bad environment for equities, especially if central banks and governments are already standing by with fresh support measures. Set against this backdrop, we are keeping investment in single stocks high and are taking advantage of any setback to make selected additional purchases. No new names were added to the portfolio in May, but existing positions were adjusted.

At the same time, we have a clear goal to keep fluctuations and losses of value within acceptable limits. Given the growing number of warning signs emitted by sentiment indicators at the beginning of the month, we accordingly adjusted the hedging components within the Ethna-DYNAMISCH at an early stage. Just recently, therefore, the net equity allocation (including derivatives) was well below the gross equity allocation (which reflects pure investments in single stocks).

The real extremes in May were to be found less on the equities side and more on the fixed-income side. After the Ethna-DYNAMISCH completely withdrew from this asset class in the spring, yields on secure sovereign bonds have fallen significantly further. The yield on 10-year German sovereign bonds has again fallen to the historically low levels it reached after the Brexit referendum in summer 2016 of around -0.2%. In our opinion, this still doesn’t offer even a half-way attractive risk/return ratio, so we believe that the combination of attractively-valued, quality equities and cash remains the optimum overall package for the Ethna-DYNAMISCH.

Figure 2: Portfolio ratings for Ethna-DEFENSIV

Figure 3: Portfolio structure* of Ethna-AKTIV

Figure 4: Portfolio structure* of Ethna-DYNAMISCH

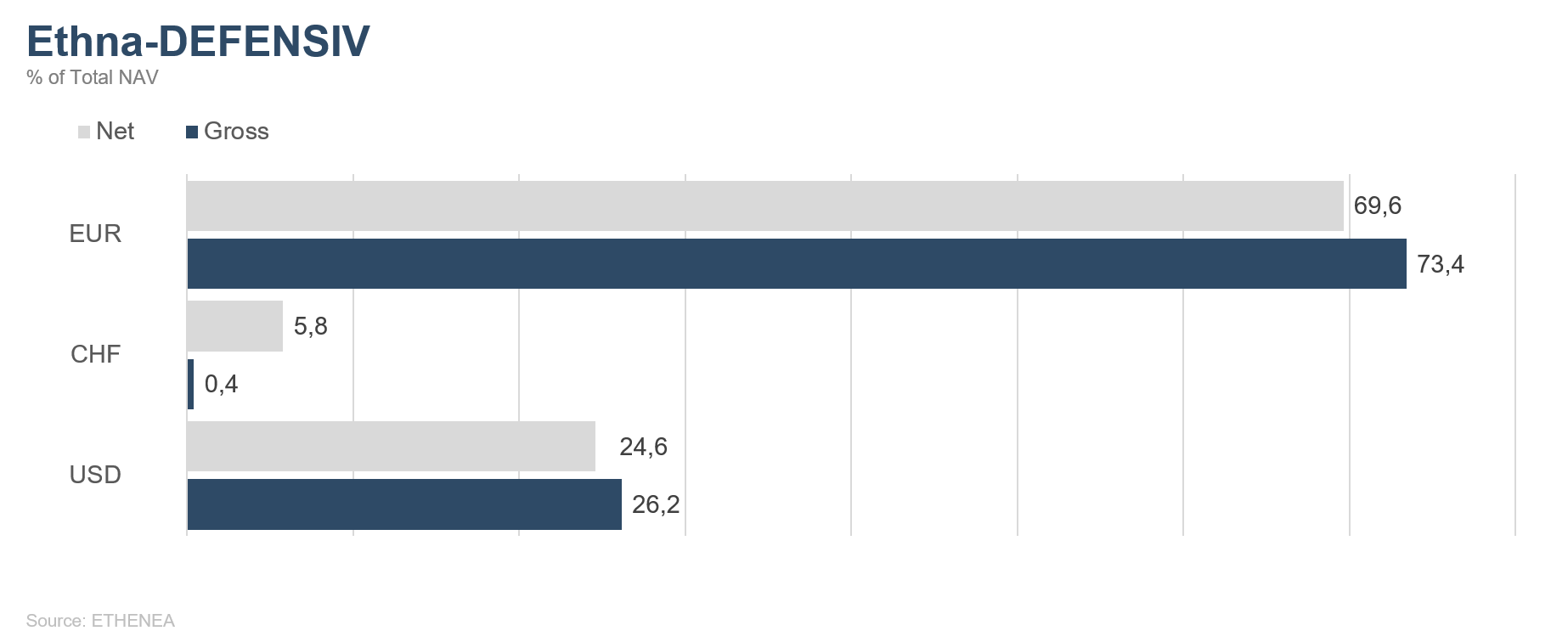

Figure 5: Portfolio composition of Ethna-DEFENSIV by currency

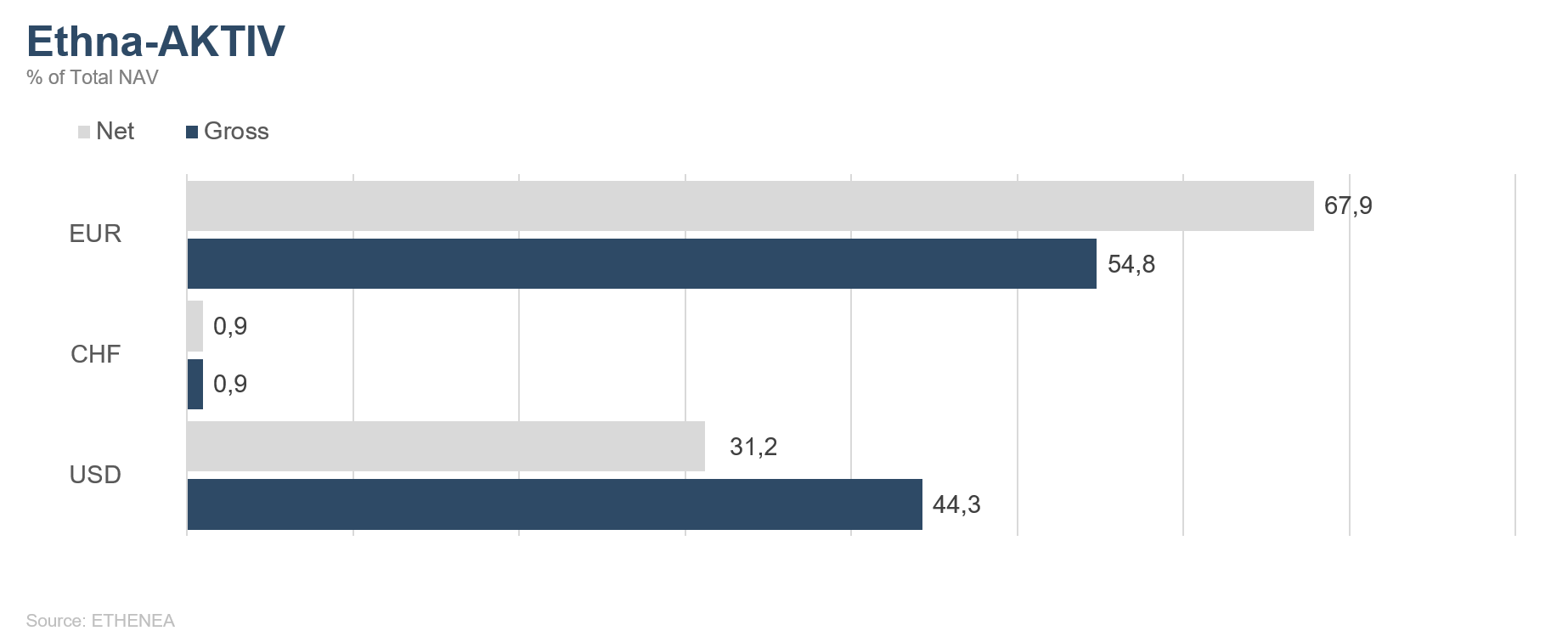

Figure 6: Portfolio composition of Ethna-AKTIV by currency

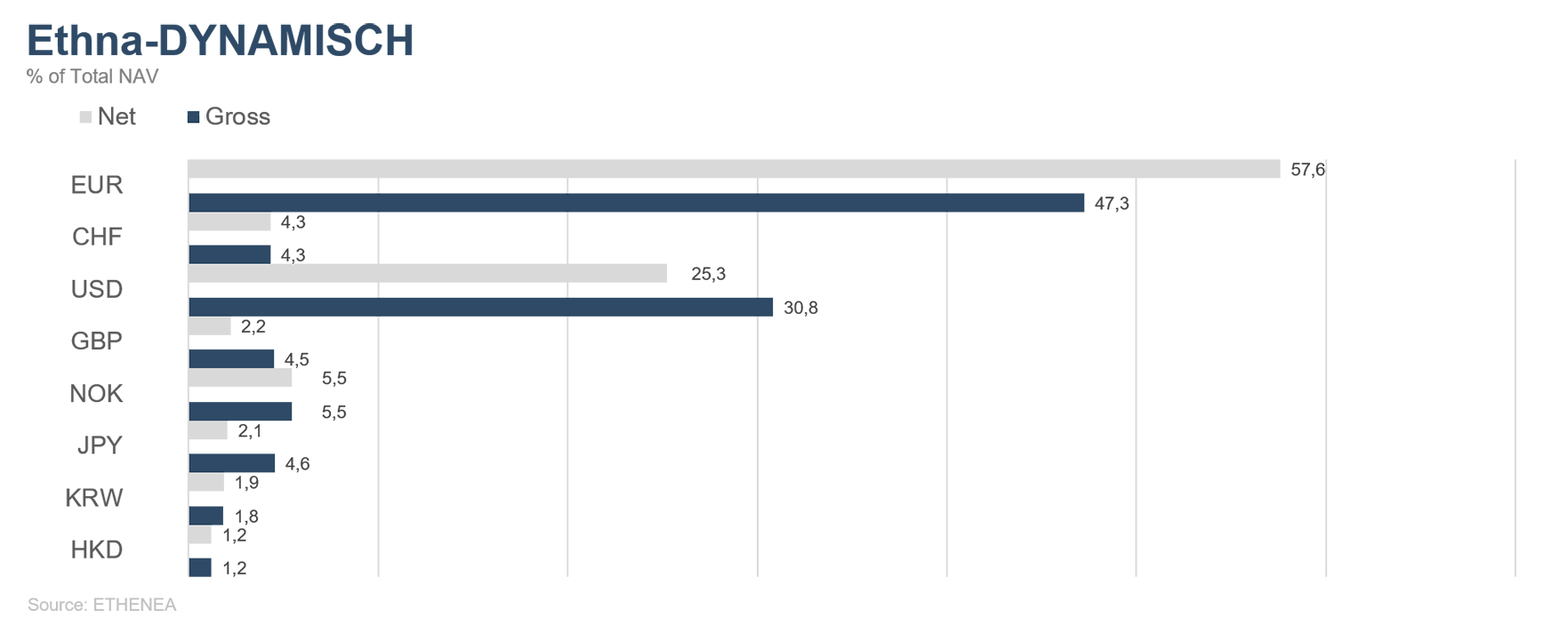

Figure 7: Portfolio composition of Ethna-DYNAMISCH by currency

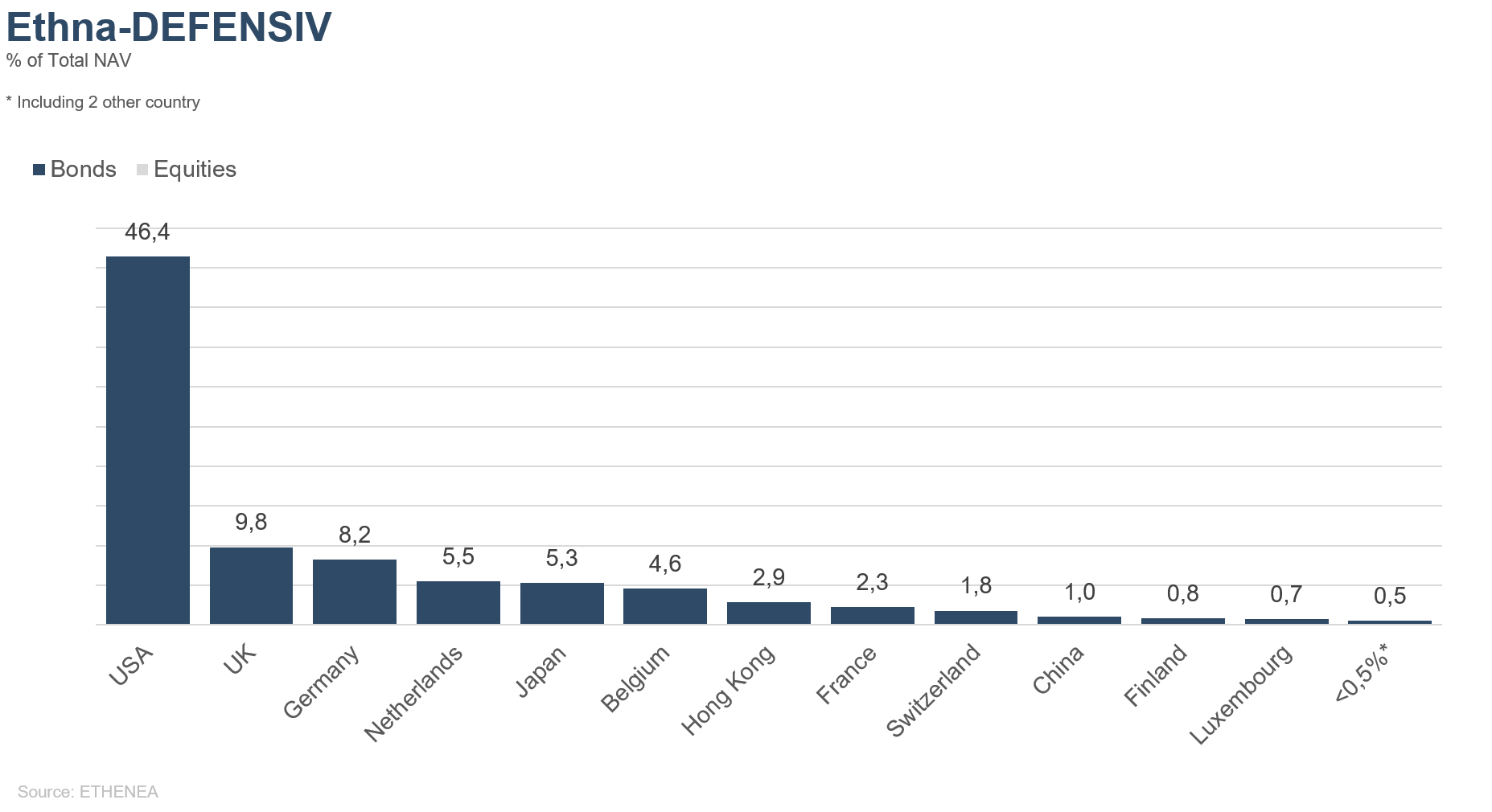

Figure 8: Portfolio composition of Ethna-DEFENSIV by country

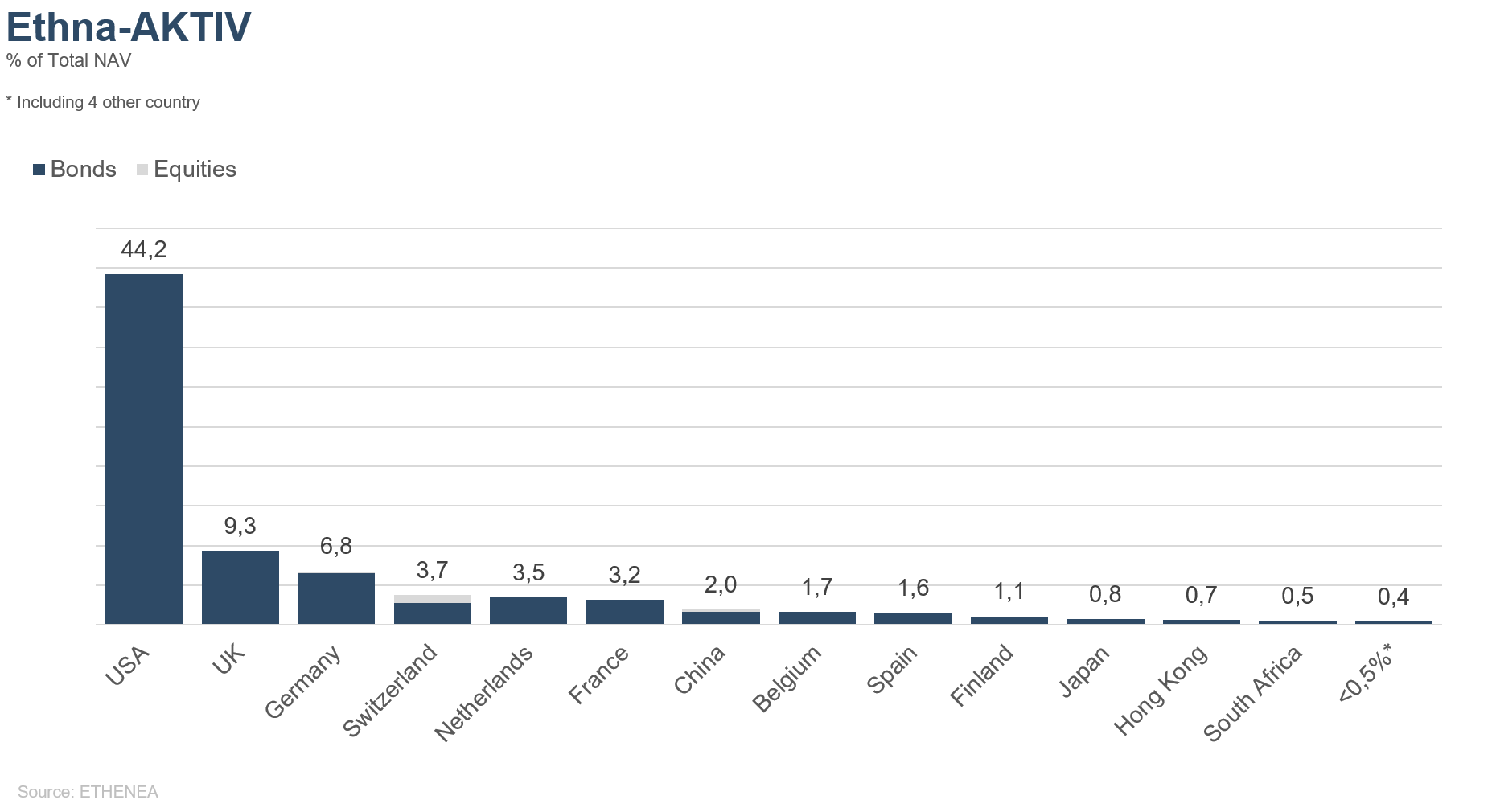

Figure 9: Portfolio composition of Ethna-AKTIV by country

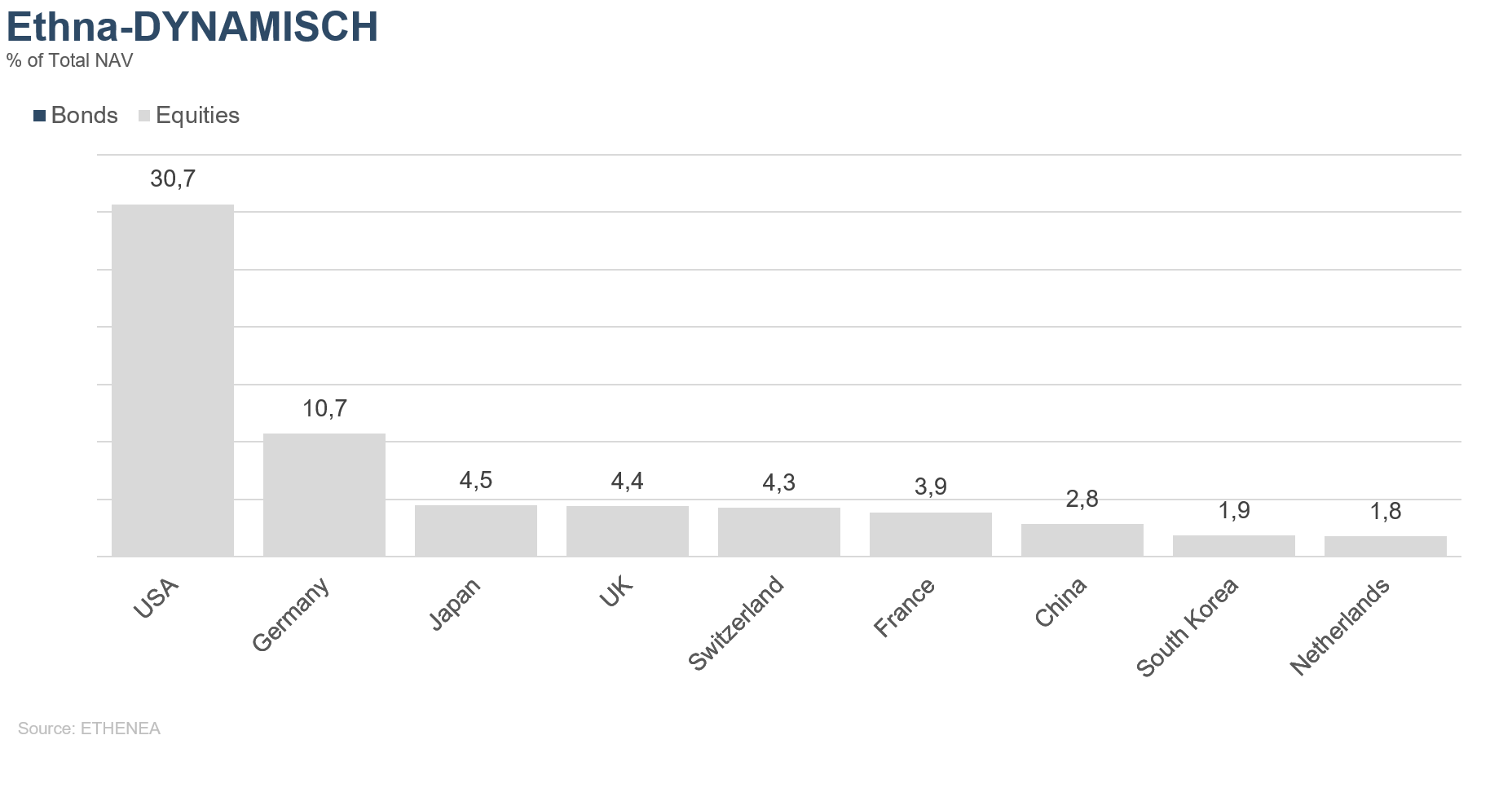

Figure 10: Portfolio composition of Ethna-DYNAMISCH by country

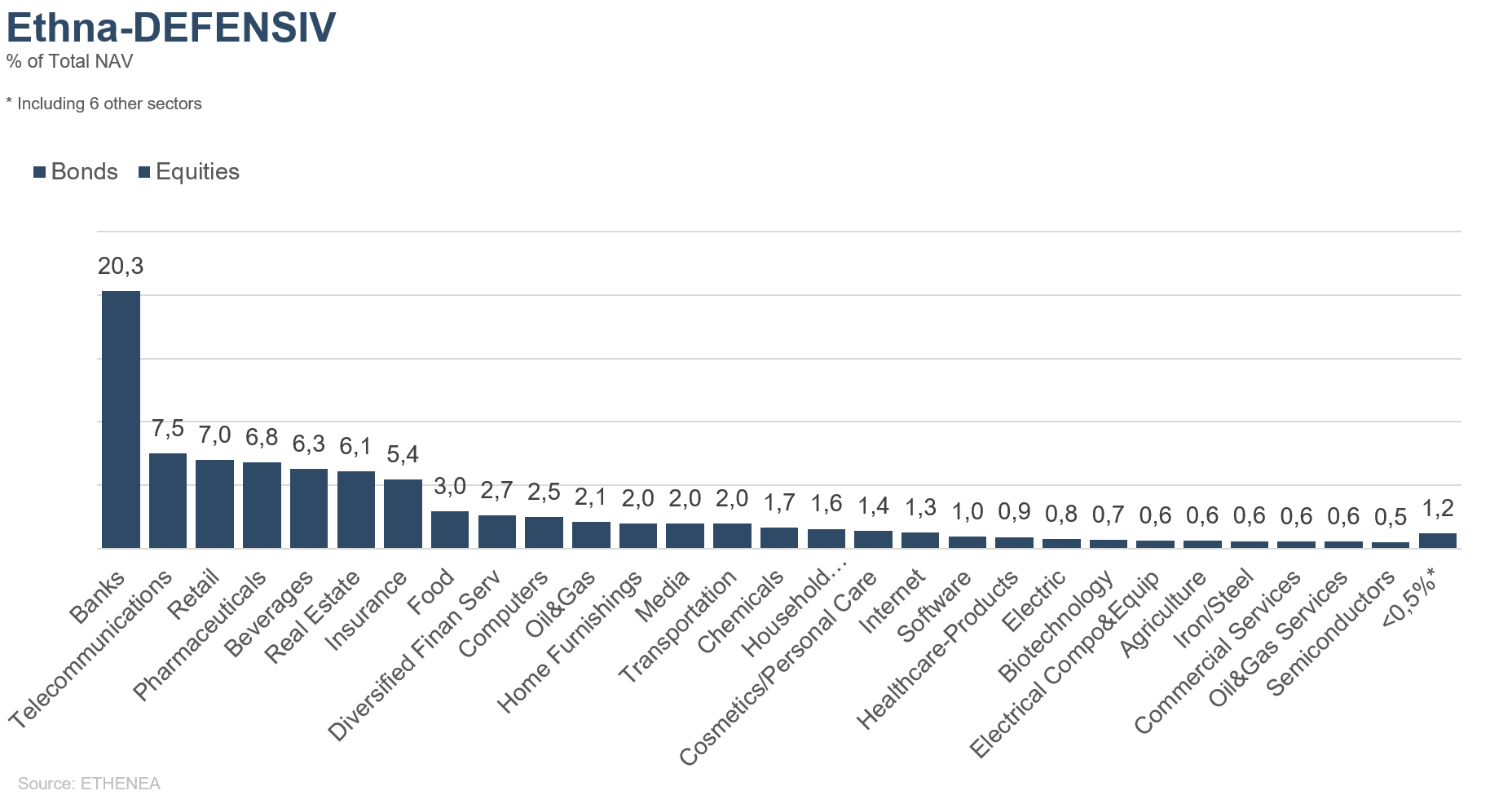

Figure 11: Portfolio composition of Ethna-DEFENSIV by issuer sector

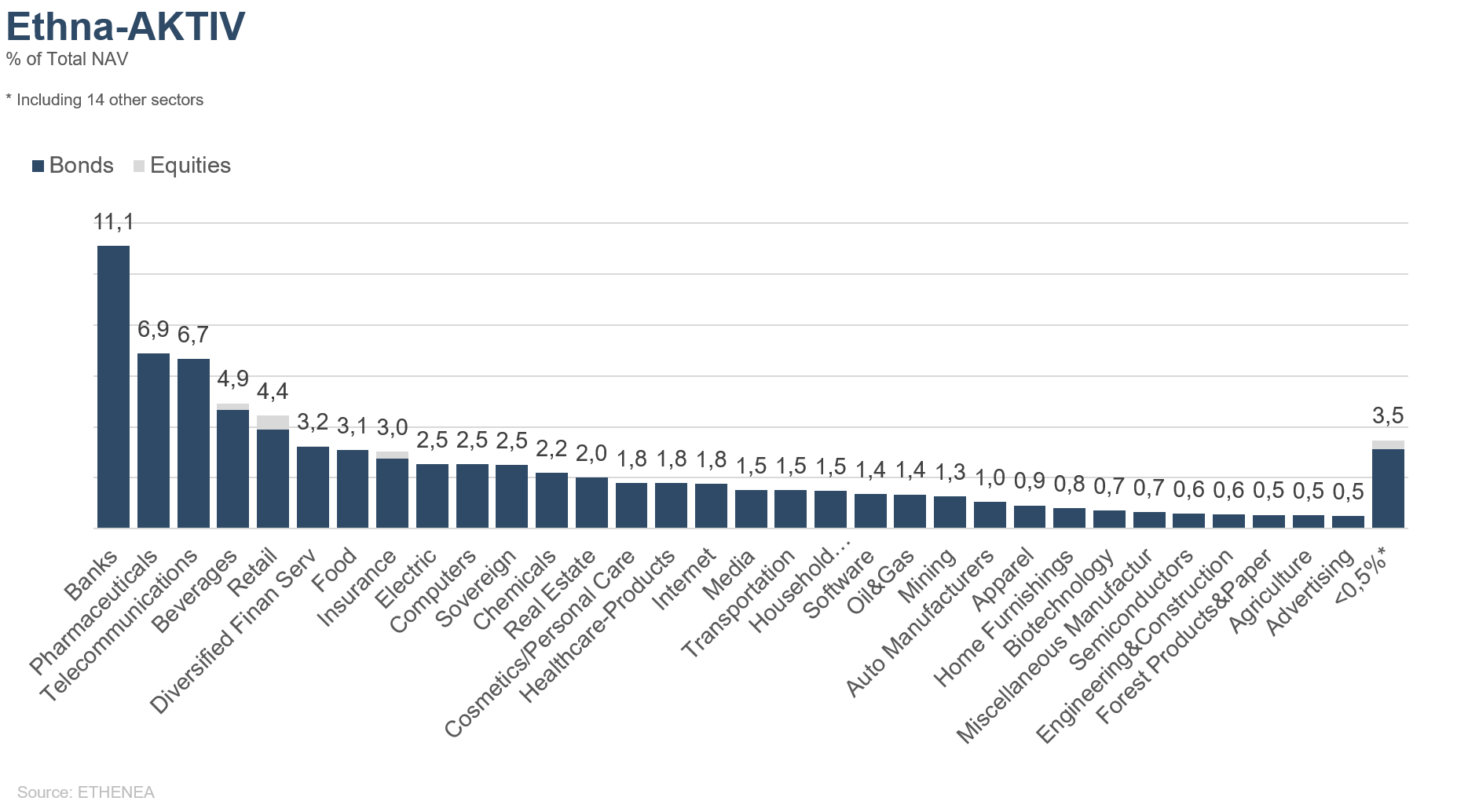

Figure 12: Portfolio composition of Ethna-AKTIV by issuer sector

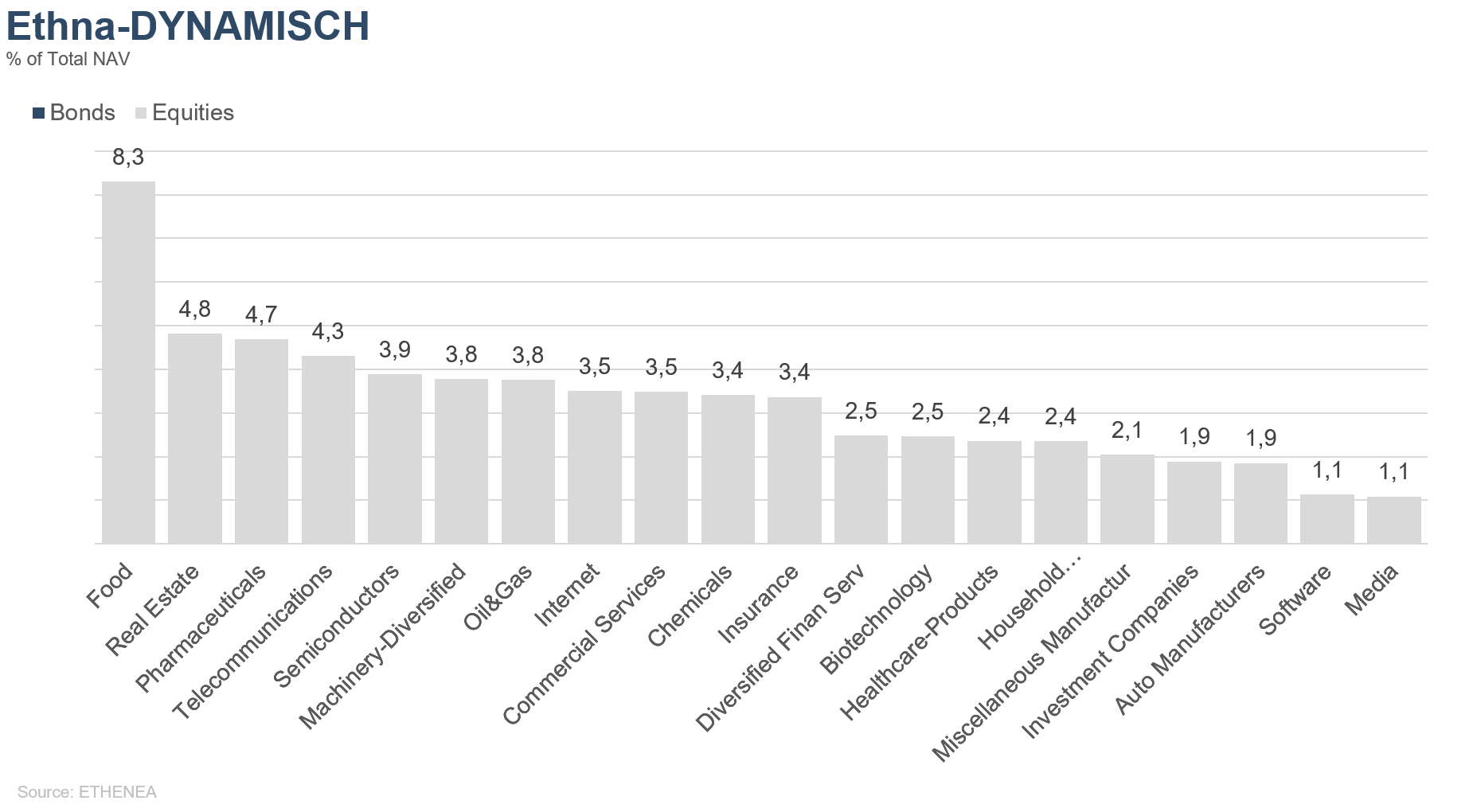

Figure 13: Portfolio composition of Ethna-DYNAMISCH by issuer sector

* “Cash” comprises term deposits, call money and current accounts/other accounts. “Equities net” comprises direct investments and exposure resulting from equity derivatives.

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

This marketing communication is for information purposes only. It may not be passed on to persons in countries where the fund is not authorized for distribution, in particular in the USA or to US persons. The information does not constitute an offer or solicitation to buy or sell securities or financial instruments and does not replace investor- and product-related advice. It does not take into account the individual investment objectives, financial situation, or particular needs of the recipient. Before making an investment decision, the valid sales documents (prospectus, key information documents/PRIIPs-KIDs, semi-annual and annual reports) must be read carefully. These documents are available in German and as non-official translations from ETHENEA Independent Investors S.A., the custodian, the national paying or information agents, and at www.ethenea.com. The most important technical terms can be found in the glossary at www.ethenea.com/glossary/. Detailed information on opportunities and risks relating to our products can be found in the currently valid prospectus. Past performance is not a reliable indicator of future performance. Prices, values, and returns may rise or fall and can lead to a total loss of the capital invested. Investments in foreign currencies are subject to additional currency risks. No binding commitments or guarantees for future results can be derived from the information provided. Assumptions and content may change without prior notice. The composition of the portfolio may change at any time. This document does not constitute a complete risk disclosure. The distribution of the product may result in remuneration to the management company, affiliated companies, or distribution partners. The information on remuneration and costs in the current prospectus is decisive. A list of national paying and information agents, a summary of investor rights, and information on the risks of incorrect net asset value calculation can be found at www.ethenea.com/legal-notices/. In the event of an incorrect NAV calculation, compensation will be provided in accordance with CSSF Circular 24/856; for shares subscribed through financial intermediaries, compensation may be limited. Information for investors in Switzerland: The home country of the collective investment scheme is Luxembourg. The representative in Switzerland is IPConcept (Suisse) AG, Bellerivestrasse 36, CH-8008 Zurich. The paying agent in Switzerland is DZ PRIVATBANK (Suisse) AG, Bellerivestrasse 36, CH-8008 Zurich. Prospectus, key information documents (PRIIPs-KIDs), articles of association, and the annual and semi-annual reports can be obtained free of charge from the representative. Information for investors in Belgium: The prospectus, key information documents (PRIIPs-KIDs), annual reports, and semi-annual reports of the sub-fund are available free of charge in German upon request from ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxembourg, and from the representative: DZ PRIVATBANK AG, Niederlassung Luxemburg, 4, rue Thomas Edison, L-1445 Strassen, Luxembourg. Despite the greatest care, no guarantee is given for the accuracy, completeness, or timeliness of the information. Only the original German documents are legally binding; translations are for information purposes only. The use of digital advertising formats is at your own risk; the management company assumes no liability for technical malfunctions or data protection breaches by external information providers. The use is only permitted in countries where this is legally allowed. All content is protected by copyright. Any reproduction, distribution, or publication, in whole or in part, is only permitted with the prior written consent of the management company. Copyright © ETHENEA Independent Investors S.A. (2025). All rights reserved. 04/06/2019