Herd mentality

Observations, though not necessarily hard evidence, do give us clear indications all the same. I strongly suspect that the majority of market participants are behaving like lemmings at the moment. It is understandable in a way, as we are all working with exactly the same information, which we get from the same sources at the same time. It’s almost inevitable that we should draw the same conclusions from it. Of course, the fact that it’s all the same doesn’t mean it’s wrong, but one must be extremely careful not to follow the lemmings over the edge of the cliff. One must extricate oneself from the herd in time.

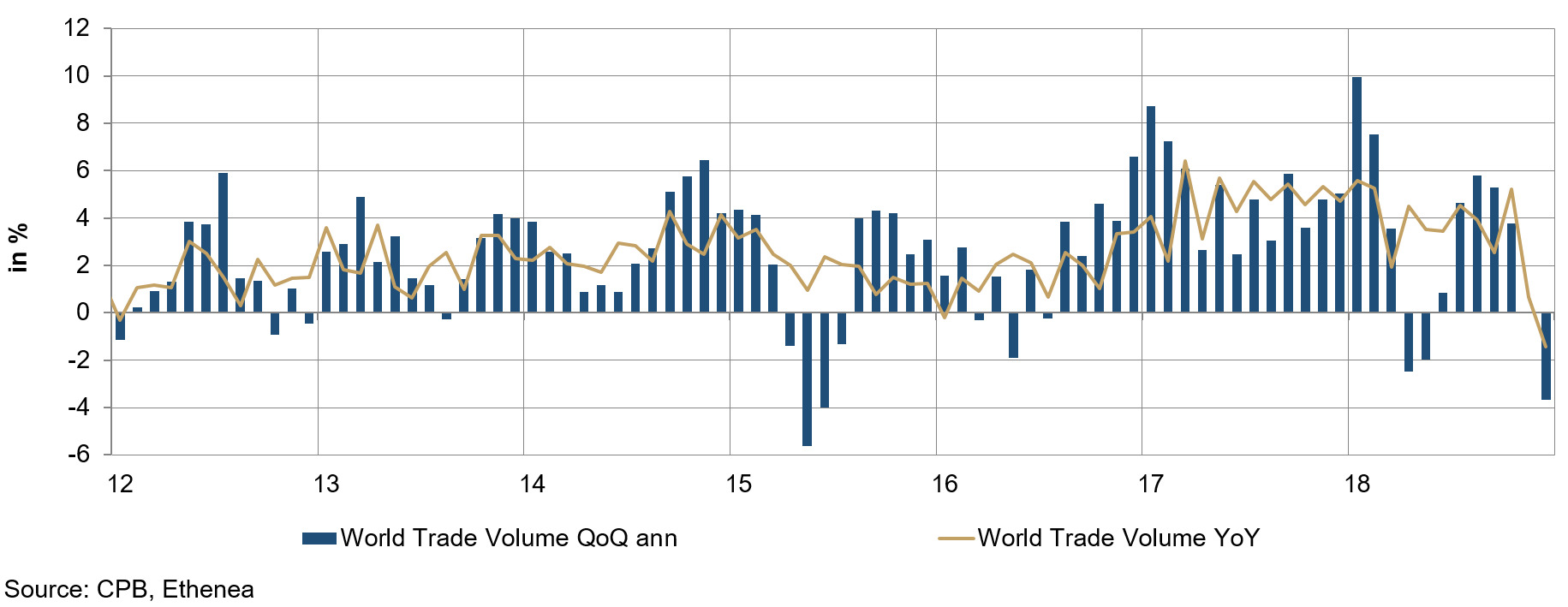

As we wrote of the global economy at the beginning of this year, we expect a bumpy landing¹ rather than a crash landing. Now that the first quarter is behind us, it would take some effort to disregard the signs of weakness. Figure 1 shows the global trade volume based on data from CPB, the Bureau for Economic Policy Analysis of the Netherlands, which is regarded as very reliable. To take some of the edge off the volatility in the data series, we look at the three-month average. Here, too, one can see a distinct slowdown in trade flow volumes at the end of 2018, which is also in keeping with the global weakness in the manufacturing sector that we are currently observing. The trade war between China and the US seems to be leaving its mark after all.

Figure 1: Global trade volume (three-month average)

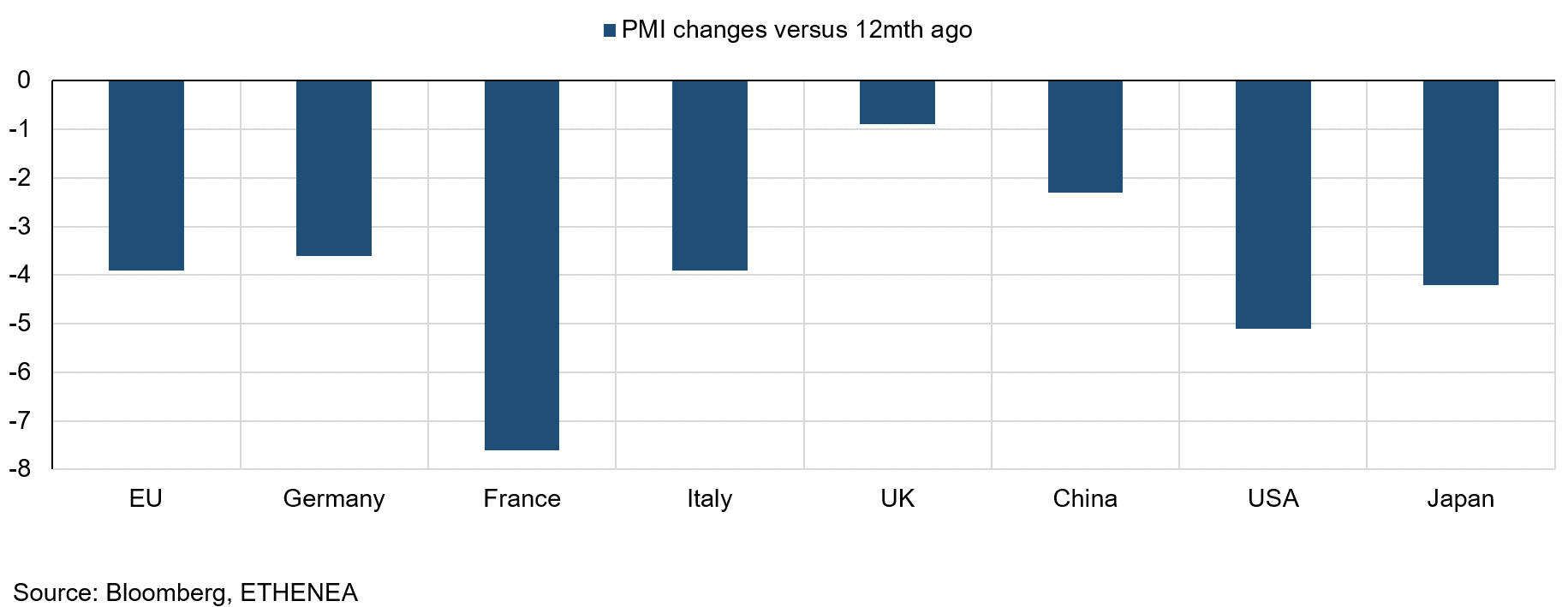

Figure 2: Purchasing managers’ index

The purchasing managers’ indices also deteriorated appreciably. Figure 2 shows the change in the PMI compared to 12 months ago. What is surprising about this chart is the very slight deterioration in the index for the UK, which is causing nothing but chaos with Brexit and has been holding European politics to ransom for many months. All I can do at this point is send a message to the British parliament. This quote is attributed to the Belfast-born author C.S. Lewis: You can’t go back and change the beginning, but you can start where you are and change the ending. Perhaps MPs will take heed. The rest of Europe would appreciate it.

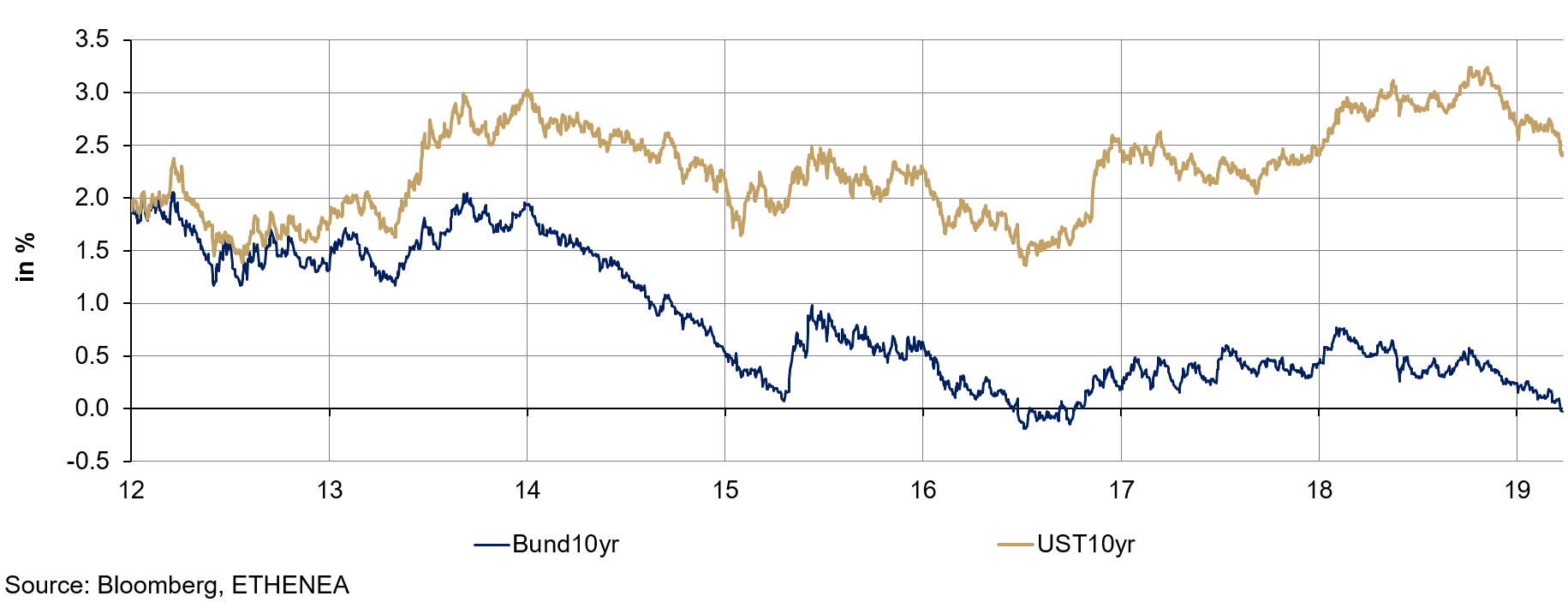

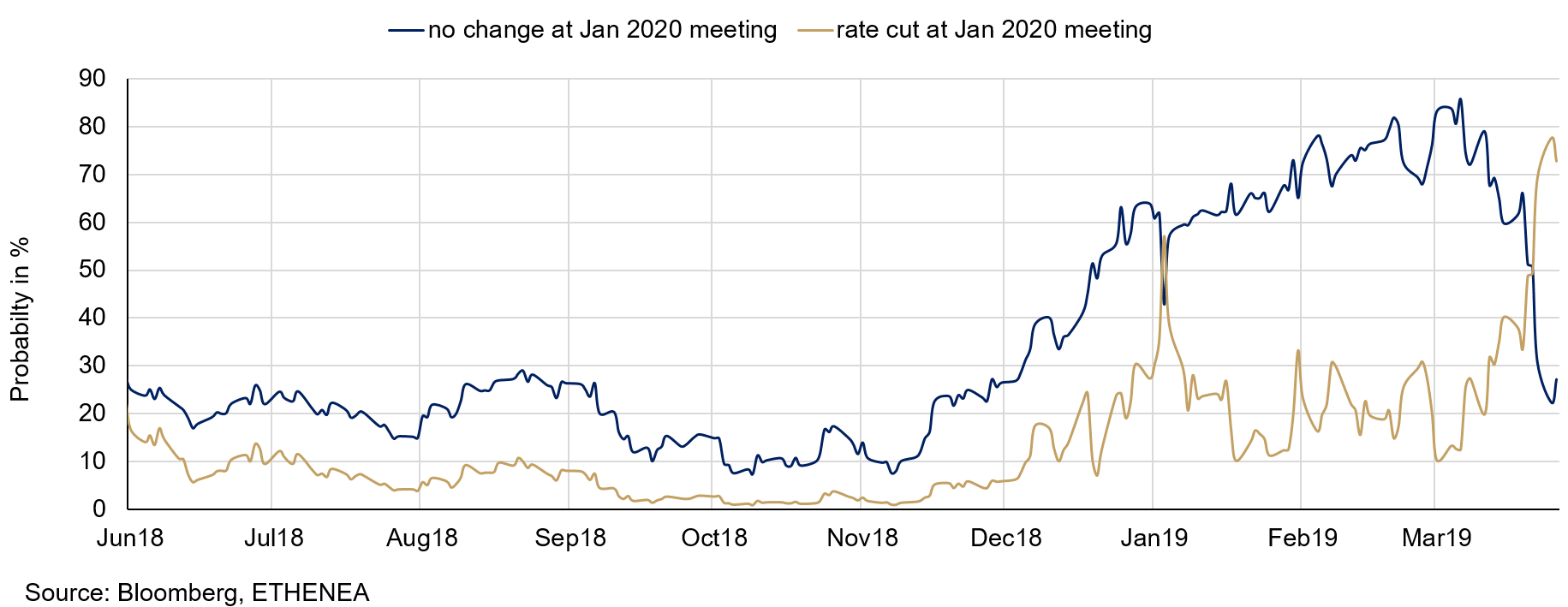

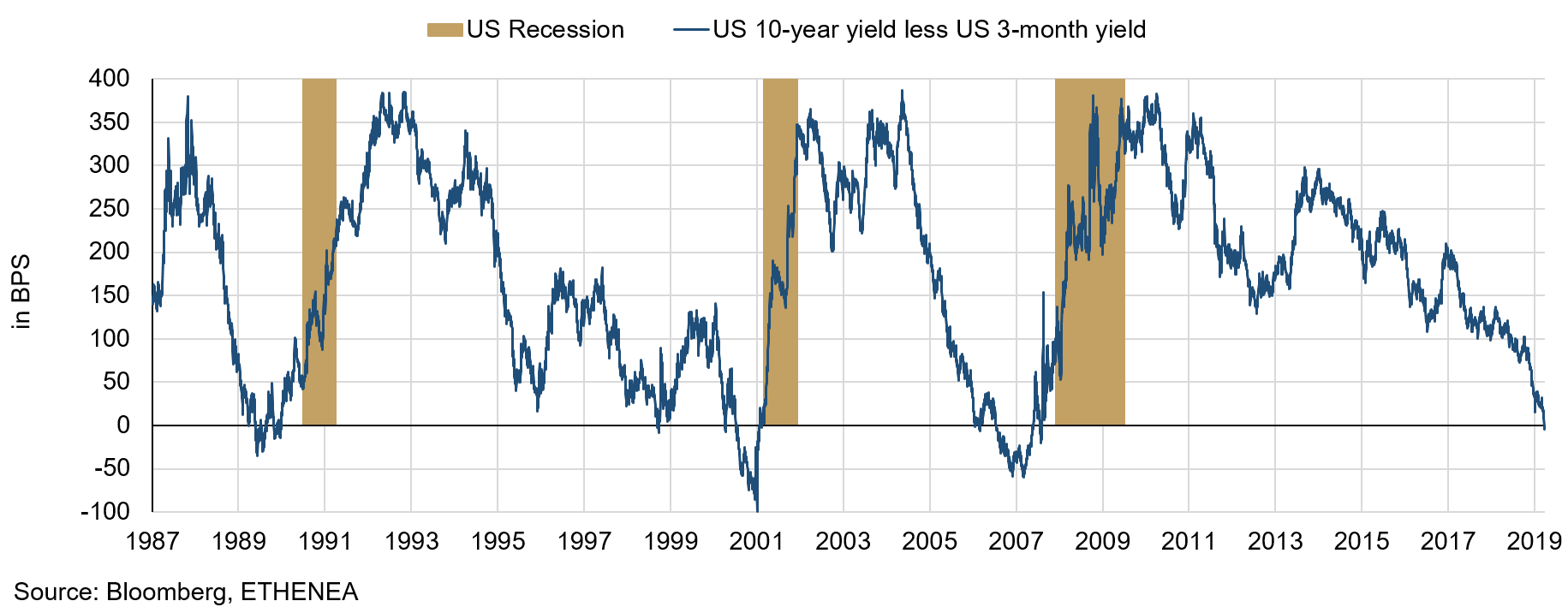

Another strong indicator of the market view of the future economy is the yield level of the 10-year Bund and US Treasury (see Figure 3). On Friday, 22 March 2019, the current 10-year Bund traded at a negative yield for the first time since 2016. This may not be due solely to the market view in relation to a future economic downturn, but also to the fear of possible chaos, if a disorderly Brexit does happen on 12 April 2019. The yield on the 10-year US Treasury thus also fell below 2.5%. This level is not all that important in itself. However, what startled market participants was the fact that for the first time since 2006 the yield curve in the US inverted, with 10-year yields falling below 3-month yields (see Figure 5). The past six recessions in the US were always preceded by a yield curve inversion 12 to 18 months beforehand. To that extent, it was understandable that the market reacted by re-assessing future rate changes by the US central bank (see Figure 4). After the curve inverted, the market (on the basis of US interest rate futures) markedly increased the probability of a rate cut by the Federal Reserve in its meeting at the end of January 2020, from almost 50% to almost 80%, while the probability of no rate change fell by a corresponding degree!

Figure 3: Yield on 10-year Bund and 10-year US Treasury

Figure 4: Implied probability of US central bank’s action at their meeting in January 2020, based on money market futures.

Figure 5: Yield differential between the 10-year and the 3-month Treasury.

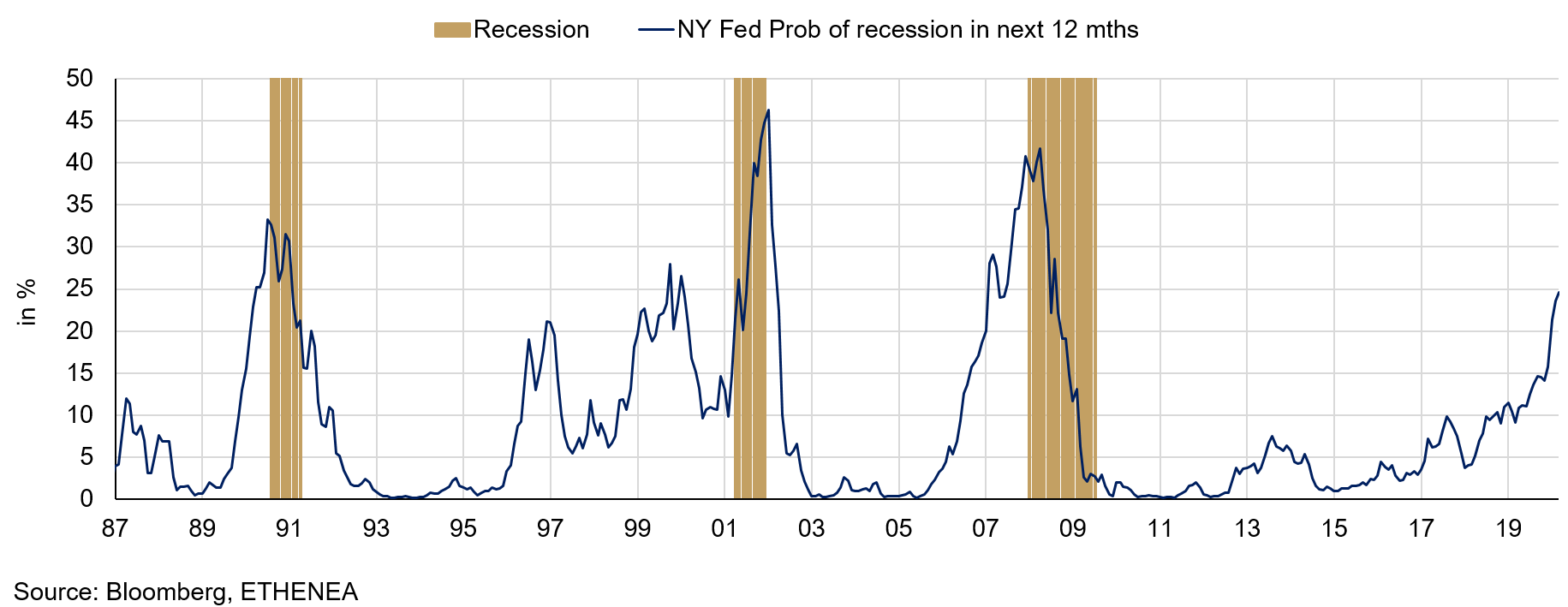

Figure 6: Implied probability of a recession in the next 12 months, calculated by the NY Fed.

The probability of recession in the coming year as calculated by the New York Federal Reserve – a widely regarded metric – also rose steadily (see Figure 6). Yet another sign.

It is now important to distance ourselves a little from the herd. The indicators described above all point to a recession in the US starting in the next 12 months and, thus, doubtless in the rest of the developed world as well. Now, this doesn’t necessarily mean that things will turn out that way. We are working with probabilities, and not with a deterministic system! It is by all means possible for a soft landing – that is, a gradual slowdown without a subsequent recession – to be engineered through the skilful interplay of monetary and fiscal measures. However, that would require the presence of an interplay in the first place. It worked well during the financial market crisis, and could do so again. After all, no one has any interest in a recession actually occurring, neither governments nor central bankers.

The opinion we have advanced quite frequently in the recent past therefore stands: that we see a slowdown on the cards and also think further worse economic data are quite possible. However, we rely on the skill of those responsible to avoid a real recession. Until the masses realise this, however, one can and should run on the flanks of the herd.

Are bonds currently a good investment?

In his role as Senior Portfolio Manager, Dr Volker Schmidt assists with composition of the Ethna-AKTIV bond portfolio. In our latest video, the bonds expert goes into how a positive performance contribution is currently possible with bonds.If you are having video playback issues, please click HERE.

Positioning of the Ethna Funds

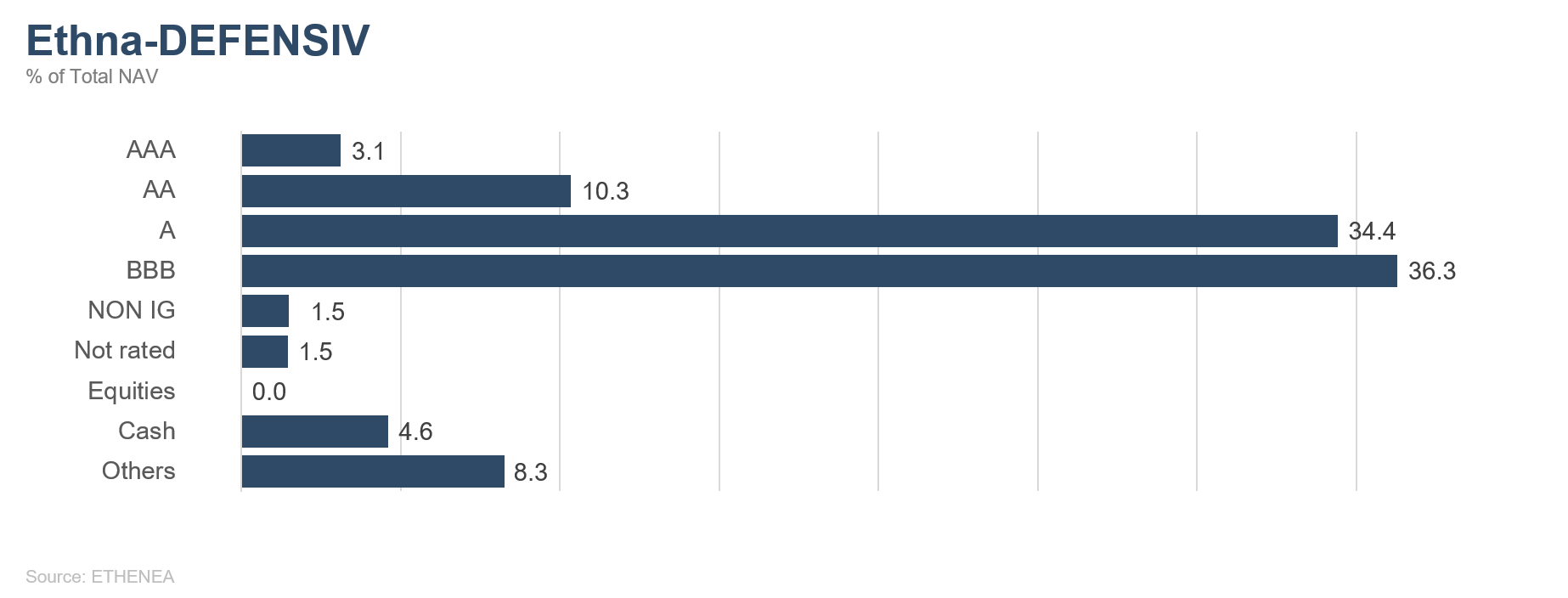

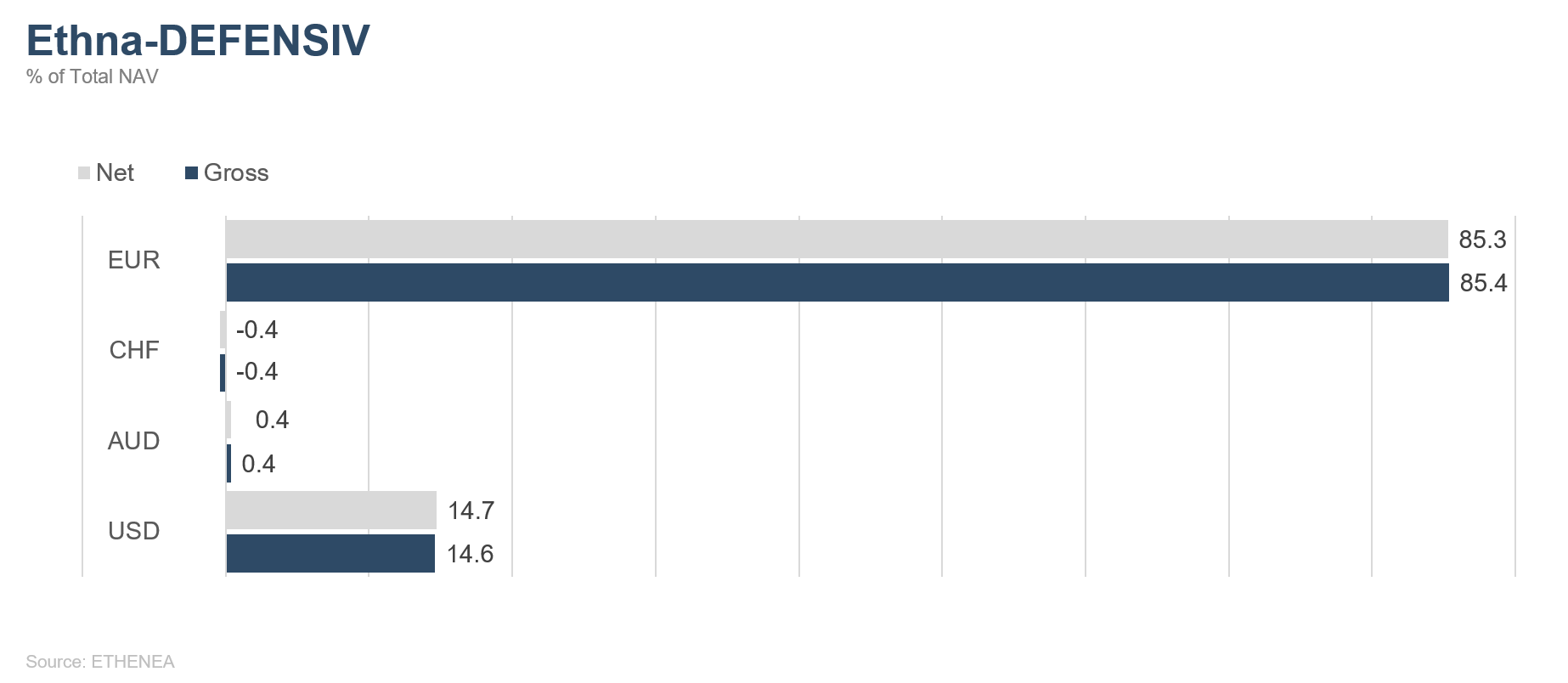

Ethna-DEFENSIV

Last month more or less confirmed the weakness in global economic growth. New data back up the theory that we are heading for a recession. However, we still believe that a soft landing – that is, a pronounced downturn without real negative growth rates – is possible, as stated above.

We have closed the equity position in the Ethna-DEFENSIV that we had built up to 4% (50% Europe, 50% US) and instead further expanded our risk position in the USD duration. We also increased the foreign currency allocation to USD by 6%, to almost 15%.

The modified duration of the overall portfolio was extended significantly, from 3.05 to its current level of 8.7, by reducing the short position in French OAT futures and at the same time purchasing US long bond futures.

Overall, taking profits on short-dated AAA and AA bonds, the yields on some of which were well down, reduced the average rating by one notch, to between A and A-. Despite that, almost 78% of the paper in the portfolio has a very good rating of between AAA and BBB+.

We also had to make adjustments to the maturities. Short-dated bonds, mainly denominated in euro, simply were no longer profitable enough from a carry point of view to hold them in the portfolio. We therefore extended our maturities. Despite that, almost 60% of bonds still have a residual maturity of between one and seven years.

Ethna-AKTIV

In our estimation, 2019 will, in all likelihood, be characterised by high volatility, and not just in equities. The month of March is a good example of this. While global equity indices, led by a strong Wall Street, climbed to new highs for the year right at the start of the month, prices fell for a few days immediately thereafter, before resuming their rally with even greater momentum just a short time later. In the meantime, the broad S&P500, for example, is back up more than 20% from the lows in December and valuations are again at levels that are more above-average than below-average. To our mind, this is not what fear of recession looks like.

However, one must admit that statements from central banks are likely to have fed into these movements. The ECB is starting up its TLTRO (Targeted Longer-Term Refinancing Operations) programme again and has let the market know that the way forward for the coming quarters is “lower for longer”. The Fed, on the other hand, is being patient. Not only has it announced the end of balance sheet reduction, but it has also virtually ruled out the probability of rate hikes in 2019. In the meantime, the market expects at least two rate cuts between now and the end of 2020. While, on the one hand, these supportive measures are no doubt positive for so-called risk assets, on the other hand, one wonders what (negative) growth prospects have prompted the central banks to make this relatively abrupt about-turn. The interest rate market seems to have answered this question for itself seeing as it’s been all one-way traffic since mid-November – downwards.

We are currently of the opinion that, in anticipation of weaker growth data, interest rates will continue to fall, and the upside potential for equities this year is relatively modest without further catalysts. For this reason, we are retaining a high duration, especially in the US, and sticking with an equity exposure of less than 20%, which is moderate for us.

Given the current spread level, we will also successively reduce the current bond exposure of 80%, since the additional credit risk is not adequately compensated, in our view. Rounding off this positioning is an open dollar allocation of more than 20%, which reflects our opinion that the US dollar will be structurally strong in the next three to six months.

In March we began investing in oil certificates and have now reached an allocation of 3.6%. Together with the gold certificate position (6.2%), commodities thus account for almost 10% of the fund assets.

Ethna-DYNAMISCH

March ended on a positive note for most of the major stock exchanges, even though gains were much more moderate than in the months prior. Considering the extremely strong start to the year, however, this development is not surprising. On the whole, the first quarter of 2019 was one of the strongest in stock market history. Valuations on the global stock markets have returned to normal thanks to the continued price rises in recent weeks. The temporary undervaluation following the correction in the fourth quarter of 2018 has been offset. We see current equity market valuations as neutral. Compared with bond yields, which fell sharply in March both in the eurozone and in the US, equities still offer the most attractive risk/return ratio for the Ethna-DYNAMISCH. Our market analysis, our proprietary Market Balance Sheet (MBS), depicts a distinct improvement in the picture since the beginning of March 2019 in comparison with previous months. The shorter-term indicators in particular show a distinctly supportive trend. Equity markets are currently in a risk-on mode, without being overbought in the short term. Since the global economy is in a cooling-off phase, the biggest challenge for markets is to realistically gauge expectations for corporate profits in the coming months. This and sharp price rises present a risk that developments in prices could be misjudged. We will keep an eye on this.

There were a few changes in the Ethna-DYNAMISCH’s equity portfolio last month. Two high-quality companies were bought: Reckitt Benckiser and Middleby. While the name Reckitt Benckiser is unfamiliar to many people, the company’s products are more widely known. With strong brands such as Calgon, Vanish and Cillit Bang, Reckitt is a leader in the counter-cyclical consumer sector. If the economic outlook dims further, Reckitt, with its defensive qualities, should be a winner. Middleby holds a similarly strong position. The US company makes high-quality kitchen appliances and boasts an impressive growth trajectory. In the past 10 years, earnings and revenues have multiplied, as has the share price. The company is planning to grow in the coming years, which should give the share a further boost in the medium term, especially since the valuation, over a prolonged period of consolidation, has again reached an attractive level. We sold KDDI and LG Uplus – two Asian telecoms companies – as we regard their upside potential as limited. In addition, we closed the Publicis and Lufthansa positions, which hold too much cyclical risk for us in light of the uncertain macroeconomic situation. The gross equity allocation of the fund over the course of the month was successively increased and is currently almost 59%. Exiting the futures positions raised the net equity allocation to approx. 52%. The expansions stem from a much better environment according to our market analysis (MBS).

March saw further, in some cases significant, falls in yields on the bond markets. As a result, the 10-year Bund traded in negative territory for the first time since 2016. In the US, too, there was a marked decline in interest rates in March. We further reduced our position in long-dated US Treasuries towards the end of March and took strong profits on them. Thus, they only hold a weighting of around 3% of the overall portfolio. With yields down again, investments in the bond market have become less attractive for us in the medium term. We remain cautious about this segment, and are not planning any significant expansion in the Ethna-DYNAMISCH for the time being.

Gold did not shine in the last month, almost completely losing the gains it had made since the beginning of the year. With a portfolio weighting of less than 3%, however, gold had only a slight influence on the performance of the Ethna-DYNAMISCH.

In our view, the fresh falls in interest rates continue to justify a substantial equity allocation in the portfolio. Then there’s the fragile economic outlook, at least in the short term. In this environment, we want to hold on to equities but are placing great emphasis on a hedging component that protects the portfolio in the event of high volatility.

Figure 7: Portfolio ratings for the Ethna-DEFENSIV

Figure 8: Portfolio composition of the Ethna-DEFENSIV by currency

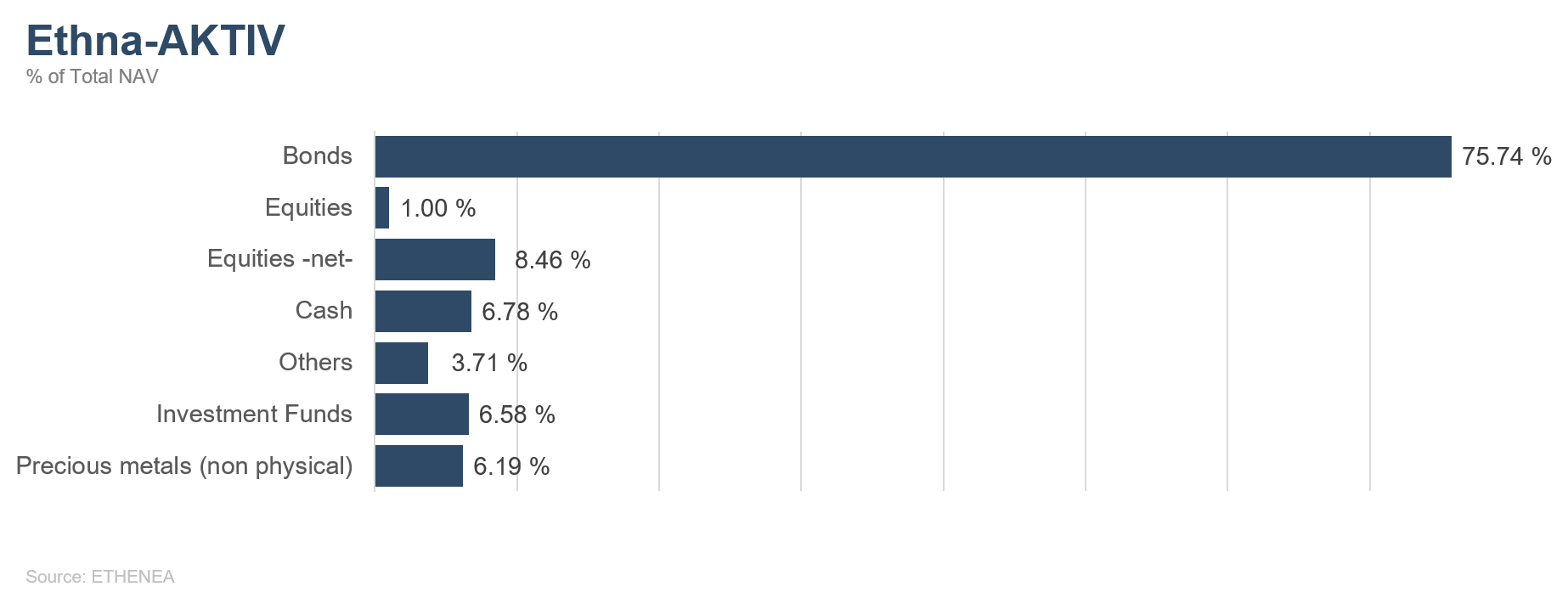

Figure 9: Portfolio structure* of the Ethna-AKTIV

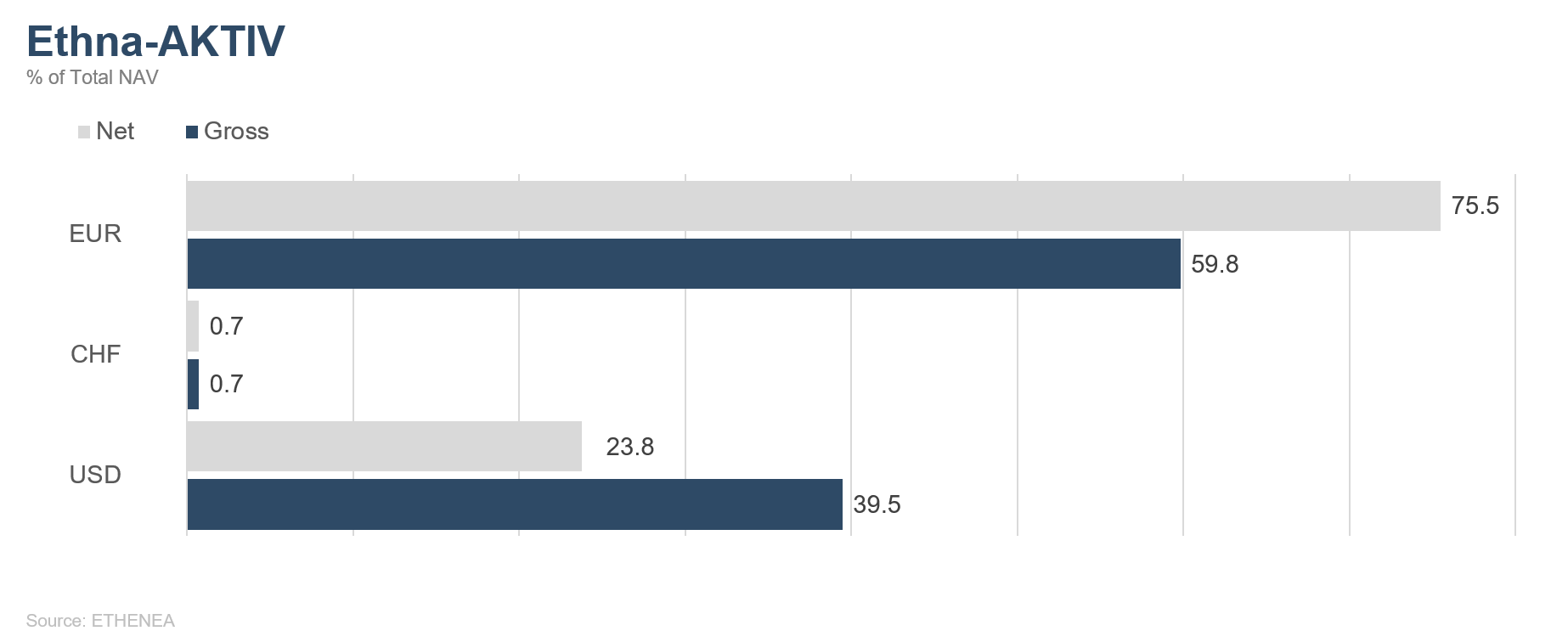

Figure 10: Portfolio composition of the Ethna-AKTIV by currency

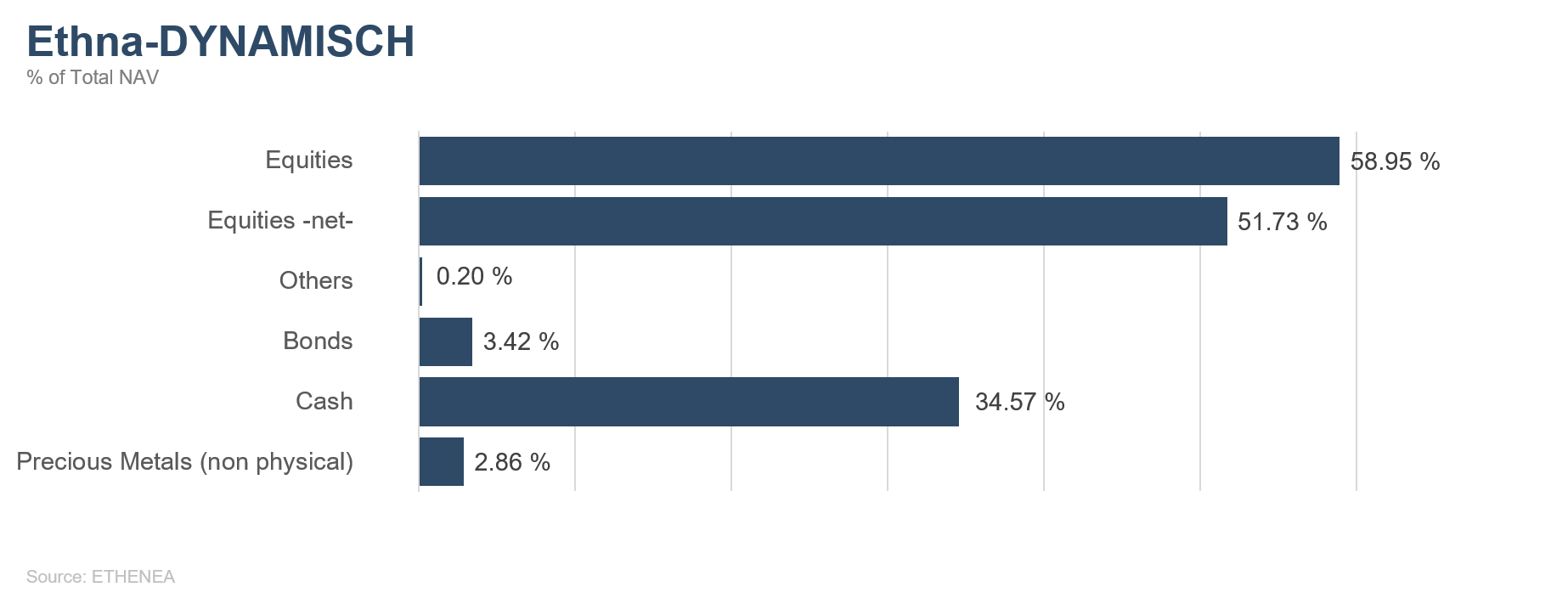

Figure 11: Portfolio structure* of the Ethna-DYNAMISCH

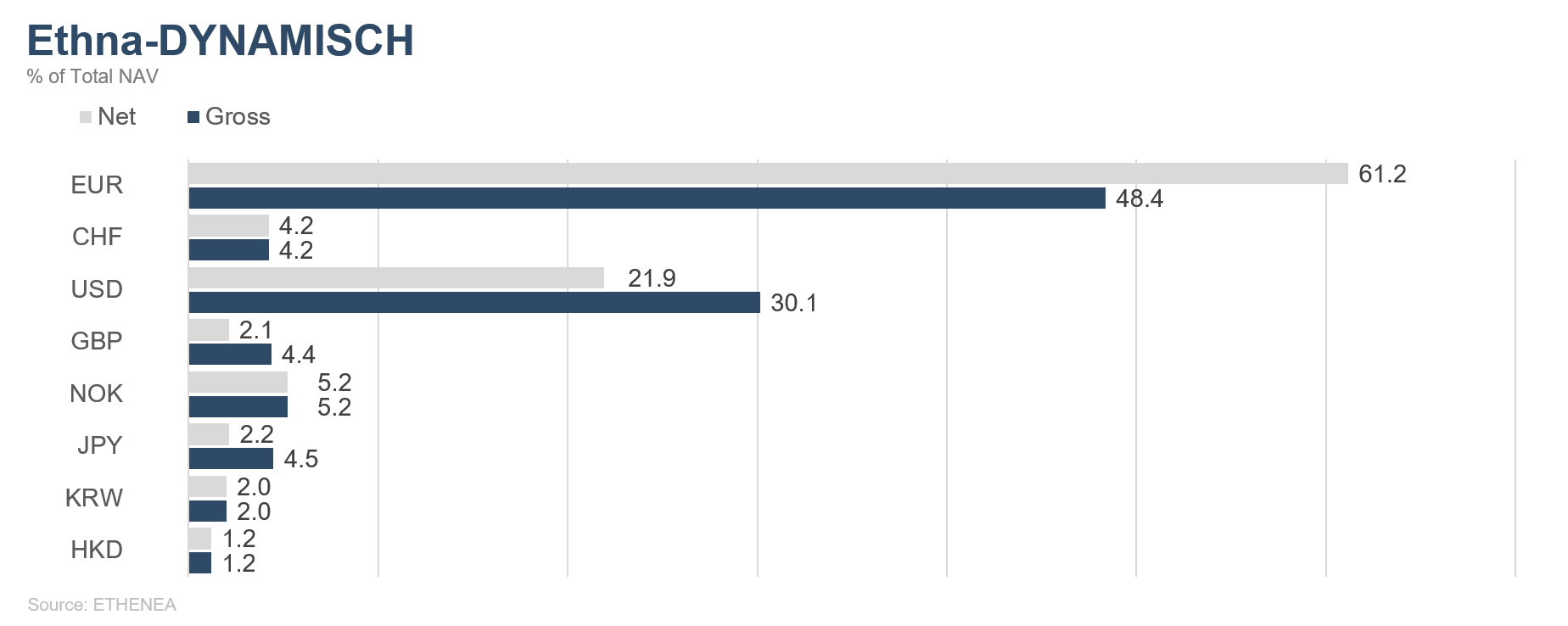

Figure 12: Portfolio composition of the Ethna-DYNAMISCH by currency

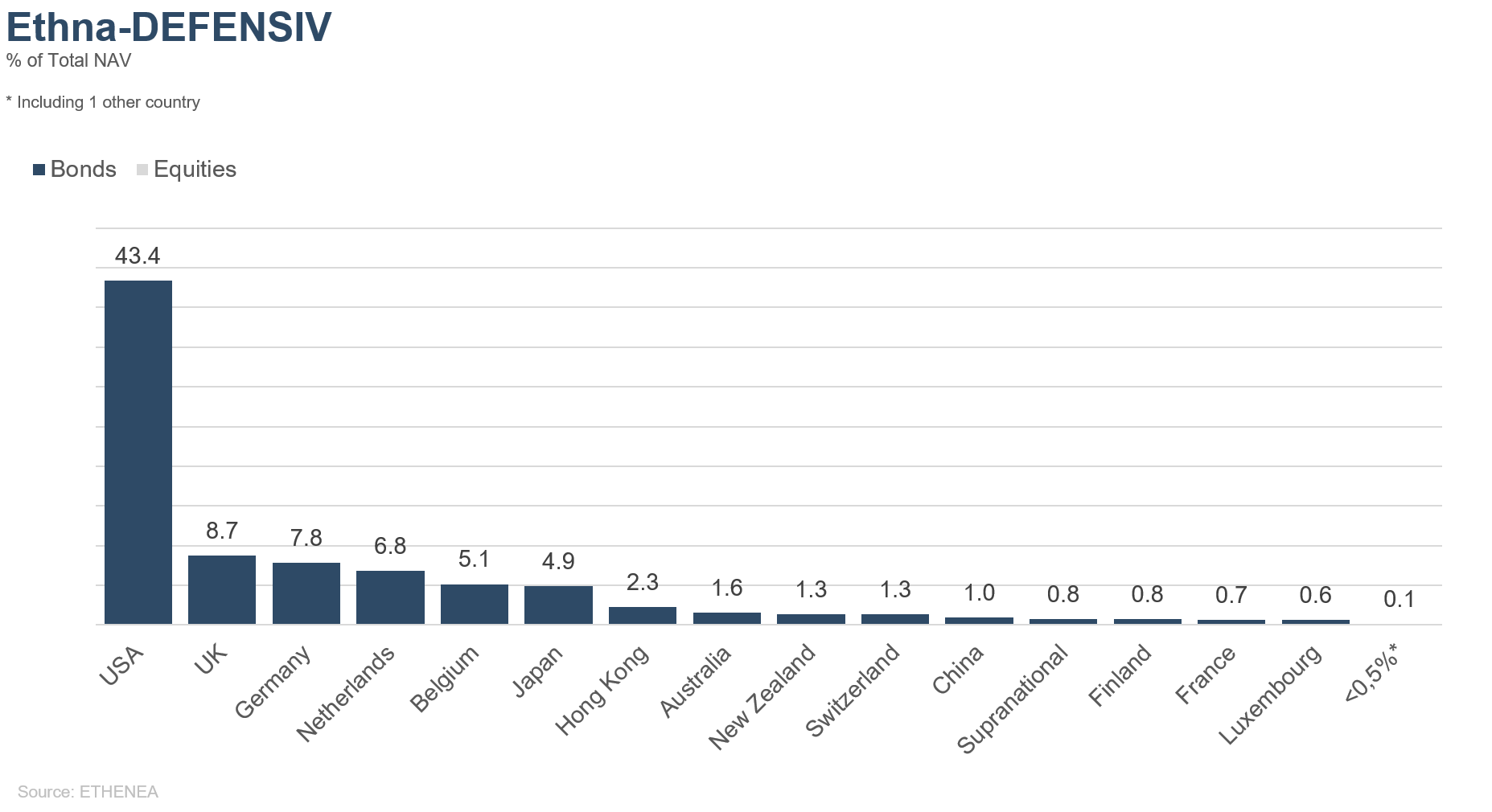

Figure 13: Portfolio composition of the Ethna-DEFENSIV by country

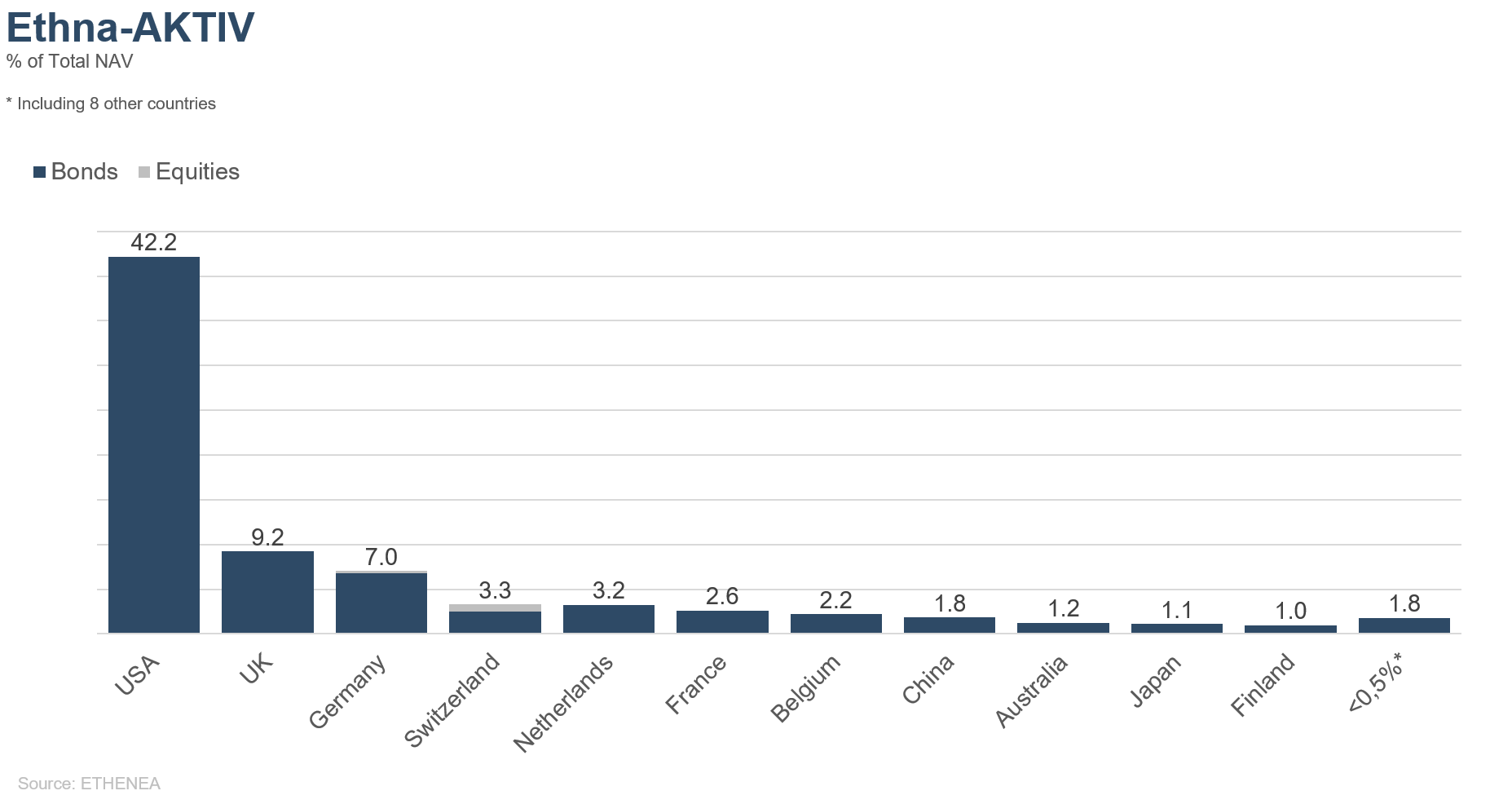

Figure 14: Portfolio composition of the Ethna-AKTIV by country

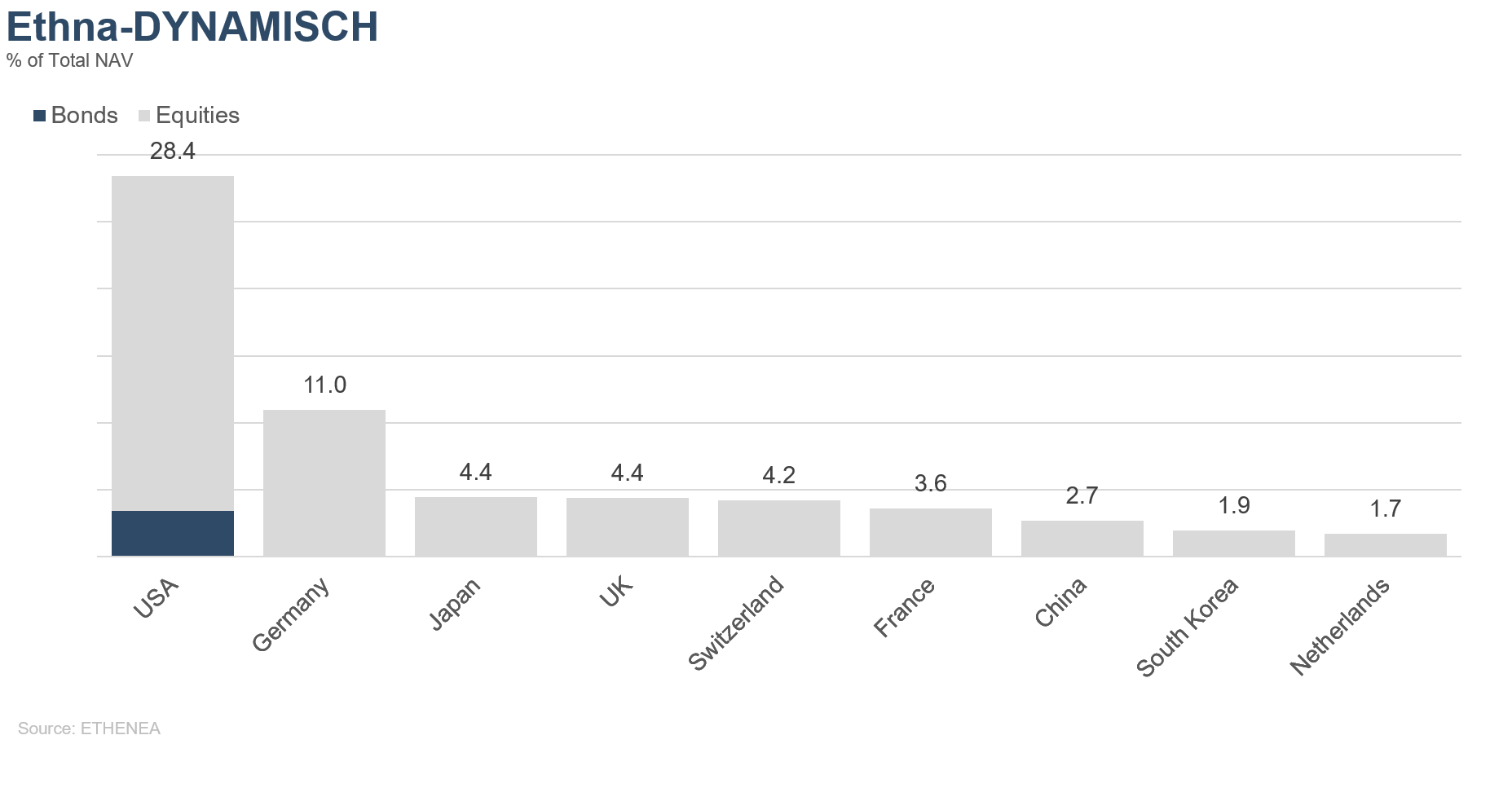

Figure 15: Portfolio composition of the Ethna-DYNAMISCH by country

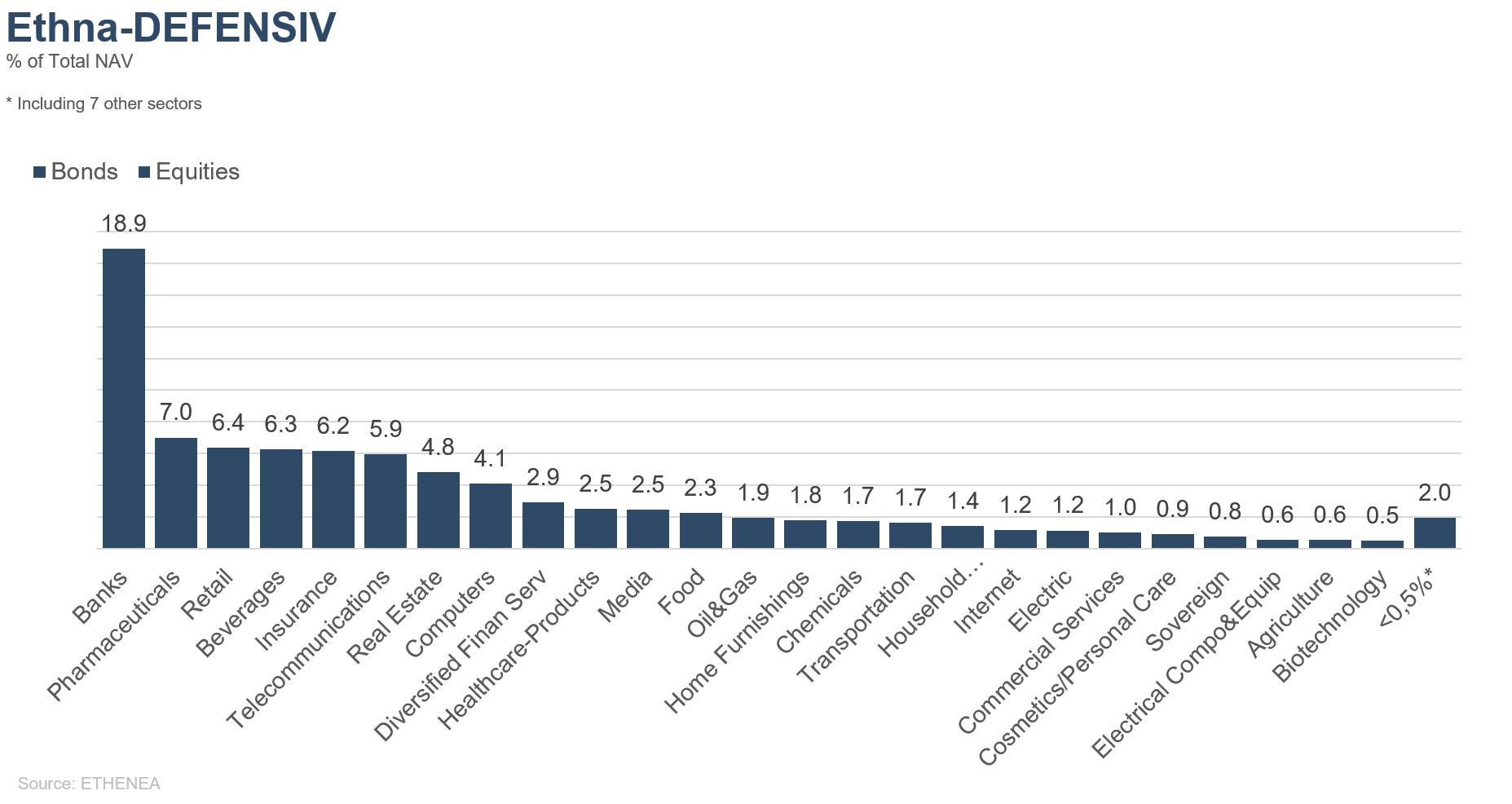

Figure 16: Portfolio composition of the Ethna-DEFENSIV by issuer sector

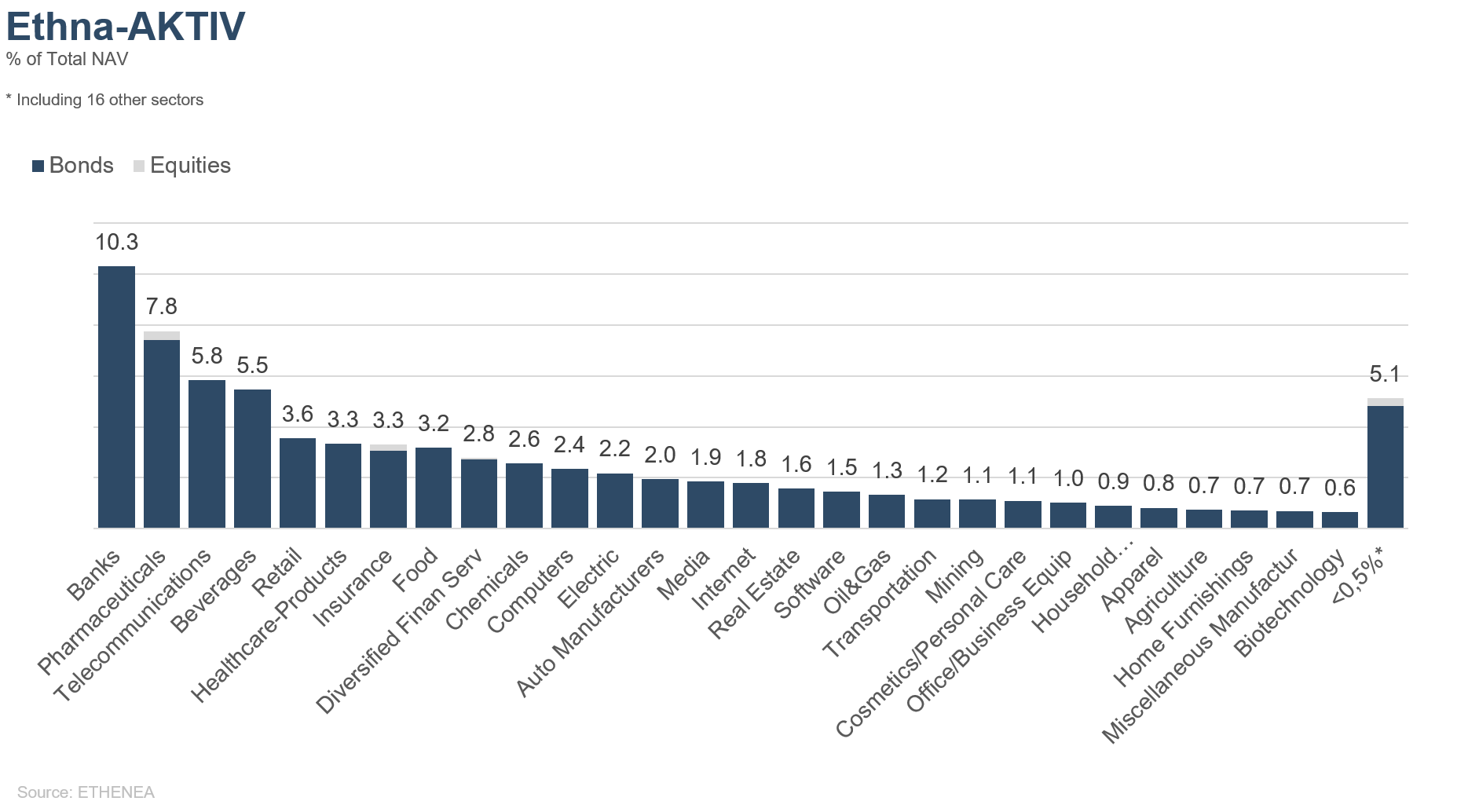

Figure 17: Portfolio composition of the Ethna-AKTIV by issuer sector

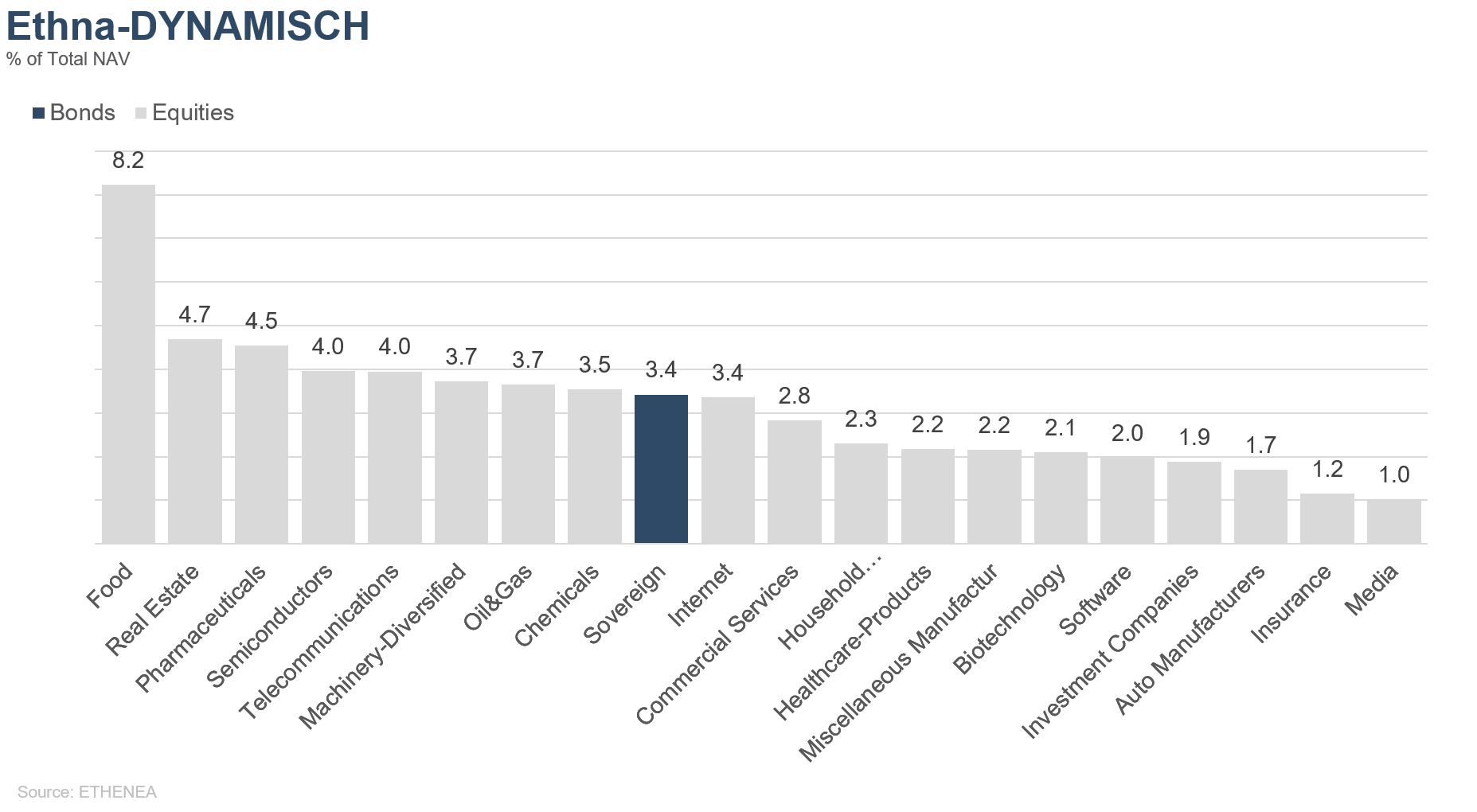

Figure 18: Portfolio composition of the Ethna-DYNAMISCH by issuer sector

* “Cash” comprises term deposits, call money and current accounts/other accounts. “Equities net” comprises direct investments and exposure resulting from equity derivatives.

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

This marketing communication is for information purposes only. It may not be passed on to persons in countries where the fund is not authorized for distribution, in particular in the USA or to US persons. The information does not constitute an offer or solicitation to buy or sell securities or financial instruments and does not replace investor- and product-related advice. It does not take into account the individual investment objectives, financial situation, or particular needs of the recipient. Before making an investment decision, the valid sales documents (prospectus, key information documents/PRIIPs-KIDs, semi-annual and annual reports) must be read carefully. These documents are available in German and as non-official translations from ETHENEA Independent Investors S.A., the custodian, the national paying or information agents, and at www.ethenea.com. The most important technical terms can be found in the glossary at www.ethenea.com/glossary/. Detailed information on opportunities and risks relating to our products can be found in the currently valid prospectus. Past performance is not a reliable indicator of future performance. Prices, values, and returns may rise or fall and can lead to a total loss of the capital invested. Investments in foreign currencies are subject to additional currency risks. No binding commitments or guarantees for future results can be derived from the information provided. Assumptions and content may change without prior notice. The composition of the portfolio may change at any time. This document does not constitute a complete risk disclosure. The distribution of the product may result in remuneration to the management company, affiliated companies, or distribution partners. The information on remuneration and costs in the current prospectus is decisive. A list of national paying and information agents, a summary of investor rights, and information on the risks of incorrect net asset value calculation can be found at www.ethenea.com/legal-notices/. In the event of an incorrect NAV calculation, compensation will be provided in accordance with CSSF Circular 24/856; for shares subscribed through financial intermediaries, compensation may be limited. Information for investors in Switzerland: The home country of the collective investment scheme is Luxembourg. The representative in Switzerland is IPConcept (Suisse) AG, Bellerivestrasse 36, CH-8008 Zurich. The paying agent in Switzerland is DZ PRIVATBANK (Suisse) AG, Bellerivestrasse 36, CH-8008 Zurich. Prospectus, key information documents (PRIIPs-KIDs), articles of association, and the annual and semi-annual reports can be obtained free of charge from the representative. Information for investors in Belgium: The prospectus, key information documents (PRIIPs-KIDs), annual reports, and semi-annual reports of the sub-fund are available free of charge in German upon request from ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxembourg, and from the representative: DZ PRIVATBANK AG, Niederlassung Luxemburg, 4, rue Thomas Edison, L-1445 Strassen, Luxembourg. Despite the greatest care, no guarantee is given for the accuracy, completeness, or timeliness of the information. Only the original German documents are legally binding; translations are for information purposes only. The use of digital advertising formats is at your own risk; the management company assumes no liability for technical malfunctions or data protection breaches by external information providers. The use is only permitted in countries where this is legally allowed. All content is protected by copyright. Any reproduction, distribution, or publication, in whole or in part, is only permitted with the prior written consent of the management company. Copyright © ETHENEA Independent Investors S.A. (2026). All rights reserved. 02/04/2019