How did it come to this? When will it come to an end?

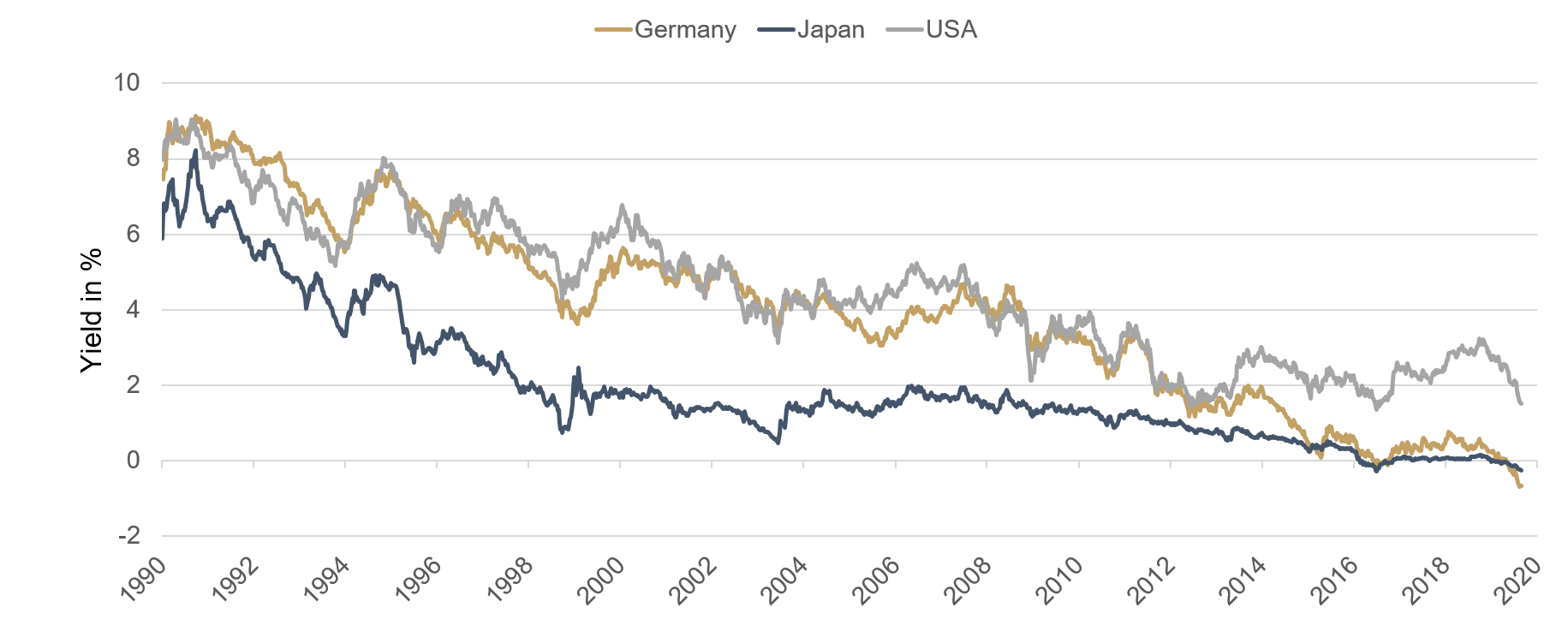

Stock markets trade in expectations for the future. Past and even current events often play a marginal role. In any case, as a rule, closer analysis of the past is not particularly interesting, as fairly logical explanations can be found for capital market developments with the benefit of hindsight. German Bund yields have constituted an exception to this rule for some time now. The yield on 10-year German Bunds serves as a reference for almost all eurozone securities and is therefore highly regarded among investors. Around five years ago, in August 2014, this important barometer of the capital markets dropped below a 1% yield for the first time. Since then the yield has climbed above the 1% mark on only a few occasions. For most of the time, it has been closer to 0% than 1%. The now entrenched low interest rate environment in the eurozone is clearly at its most pronounced here.

While the minuscule yields of +0.20% for a fixed ten-year maturity – such as around the end of 2018/beginning of 2019 – caused some head-shaking but did not lead to the collapse of whole paradigms, today we are much further down that road. Since the beginning of the year, the yield has steadily slid further and hit a low of -0.73% last month. From investors’ point of view, this means: an investor lends €107.60 to the German state and gets back exactly €100 in ten years’ time without receiving any interest between now and then. How’s that for a bargain?

What’s that you say? You didn’t go for it because it’s not a good deal? We didn’t either. But let’s get back to the original question. How did it come to this? And have we come to the end of it? At the moment there is no more talk of yields falling to -0.80%, -1.00% or even -1.20% among capital market experts than there was of yields of -0.20%, -0.40% and -0.60% a few short months ago. Could yields continue to fall against all expectations?

The fact is that the main drivers of recent years are more or less unchanged. Frequently, a fatal combination of insufficient growth and high debt lies at the heart of a sustained downward spiral of yields/interest rates. It is quite obvious that this phenomenon originated in Japan at the end of the 1990s. Since as far back as 1997, 10-year Japanese sovereign bond yields have found it virtually impossible to top the 2% mark. Demographic change, for one, and record-breaking national debt of almost 250% of GDP, for another, have seen the Japanese central bank (BoJ) act as a pioneer of unconventional central bank policies for many years. Europe is following in its footsteps, albeit with some delay. In the end, the vicious circle always has the same result: high (national) debt, which can only be sustained by keeping interest rates artificially low and which would put the countries affected into a sociopolitical bind in the medium-term if interest rates were to rise even slightly. In short, interest rates and yields cannot increase in Japan. The same goes for Italy and thus for the whole of the eurozone. Of course, each region has its own individual characteristics, but what is crucial here is the direction. China’s demographics and America’s exploding national debt could therefore well mean that they are next in line. However, it will be some time before it comes to that. Of greater relevance is the current effect of the above scenario on the capital markets.

The whole world thinks globally these days. Capital, too, has a global orientation. Thus, opportunities and possibilities to increase the expected yield keep arising: this can be done from a local perspective with the aid of a few tricks, by having an intelligently structured, global portfolio. Between summer 2013 and early 2016, EUR or JPY investors, for example, managed to significantly increase their bond yields by buying much higher-yielding USD bonds and very cheaply eliminating the currency risk. This happened more and more, triggering a convergence of yields and pushing the German ten-year Bund into negative territory in 2016 for the first (albeit brief) time. Since then, the hunt for yield has continued, and found a new attractive source of yield in recent months in the purchase of USD bonds – this time without the currency hedging that has become much more expensive in the meantime. The yield on 10-year US Treasuries fell to close to its all-time low; that is, from 3.25% in November 2018 to 1.44% in August 2019. The gloomier economic forecast was doubtless an additional factor here. However, the global hunt for returns did more than just speed up the development, as evident from comparison with equity markets, which rose almost in parallel. Obviously, the downward spiral in yields leads to significant spin-off effects and feedback mechanisms.

Figure 1: Yields on 10-year sovereign bonds over time

In particular, the feedback mechanisms could be a factor in how German Bund yields will develop in the future. Take the following scenario for example: assuming that the US Treasury yield will continue to head towards 1% or even lower (and all other things being equal), the German Bund yield stays at -0.70%. The persistence of the EUR-USD interest rate differential means EUR-USD currency hedging would earn the USD investor around 2.40% for one year. The USD investor would thus have a choice between a US Treasury with a USD yield of 1.00% or a USD-hedged Bund with +1.70% (resulting from -0.7% EUR yield plus a 2.40% return on the hedge). It may seem crazy at first, but it could put further considerable – and previously unexpected – pressure on European yields. As long as the EUR-USD interest rate differential remains as large as it is at the moment, investors should prepare for yield trends to remain in alignment; that’s regardless of the current level, and whether they are positive or negative.

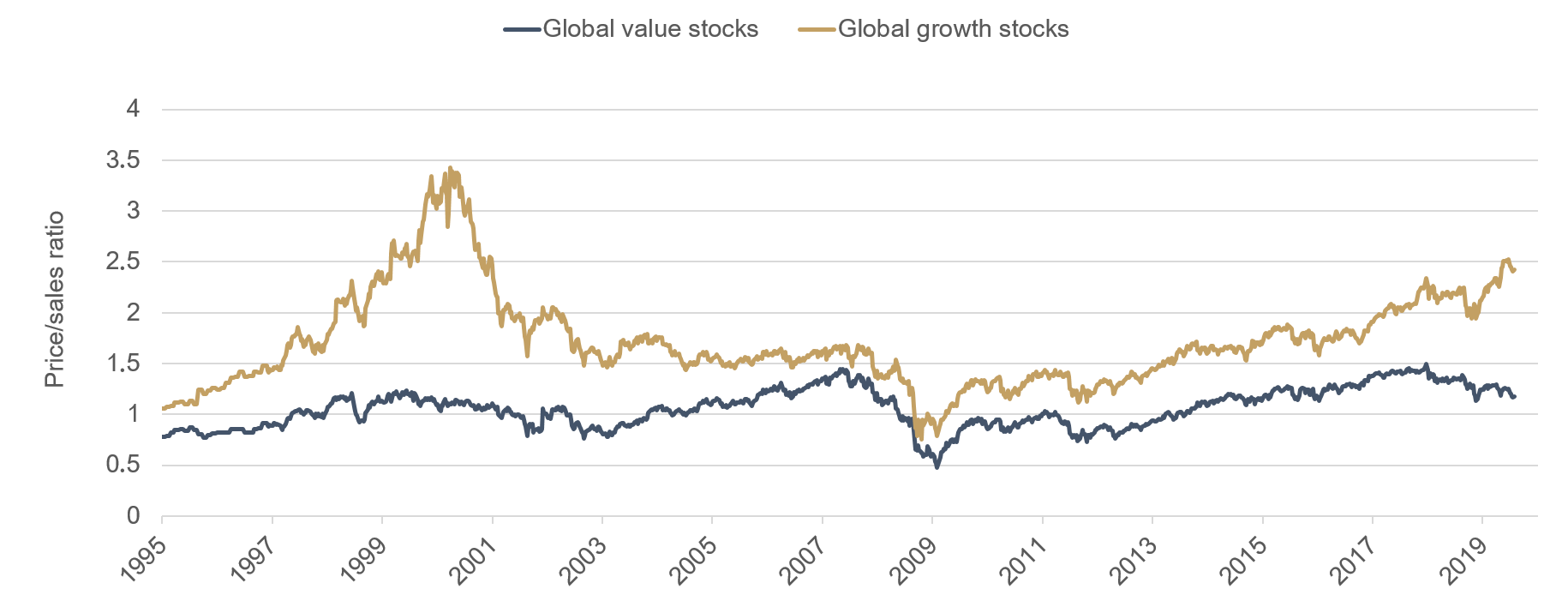

A word about the undeniable spin-off effects of the fact that bond yields are dissipating globally: just as bond prices are being driven up by falling yields, the prices of real estate, art, classic cars, gold and equities have been soaring in recent years. There has been a growing focus recently on high and top quality, which has made it increasingly difficult for price-conscious investors to participate to an adequate extent. In the past few years, for instance, the valuations of the 20% most expensive equities in the US S&P 500 index rose steadily, while those of the 20% cheapest equities fell in parallel. In addition, the debate currently underway in Berlin about a rent control law shows that the spin-off effects are not confined to capital markets and savings earning no interest, but are affecting society in ever-widening ripples due to second-round effects.

Figure 2: Equity valuations over time

So, what does this mean for the future? There are few signs that we have come to the end of the downward spiral. In light of the upwards of 16 trillion US dollars in outstanding bonds with negative yields globally, in addition to politicians and central banks that are resolutely combating the tough and unpleasant upheavals, investors will find it harder to earn attractive investment income in future. Doing so efficiently, and within reasonable risk limits, is what the ETHENEA Portfolio Management Team is all about.

From trade conflict to currency war?

The latest tariff increases marked a new phase in the trade conflict. China’s additional, calculated devaluation of the yuan is a clear shot across the bows to the US that it means to use the currency as a weapon. In our latest video, Frank Borchers explains what this means for the management of the Ethna-AKTIV.If you are having video playback issues, please click HERE.

Positioning of the Ethna Funds

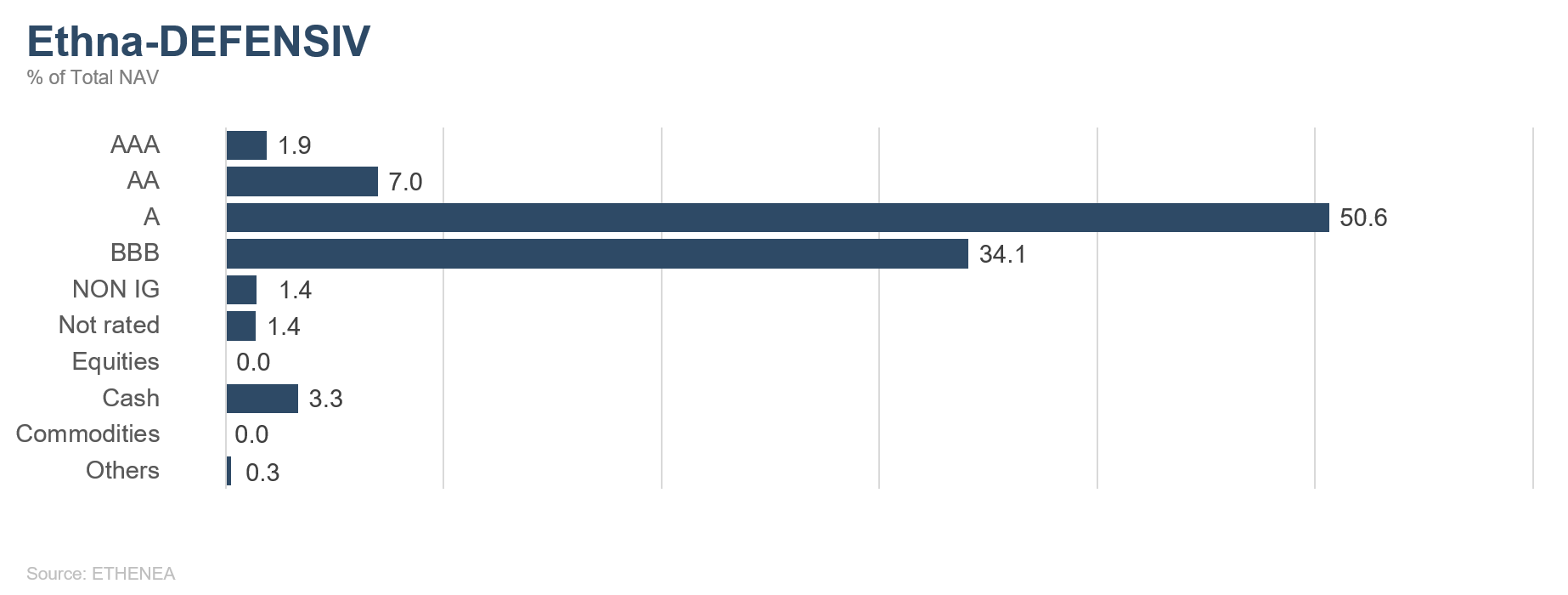

Ethna-DEFENSIV

Increasing geopolitical uncertainty dominated August. In the UK, Prime Minister Boris Johnson is testing the limits of democracy by suspending parliament just weeks before the UK’s scheduled EU exit date. In Italy the anti-establishment party Five Star Movement and the centre-left Democratic party, which had been in opposition, agreed to form a new government. This came after a political coup by the former Minister of the Interior and Federal Secretary of the Lega party, Matteo Salvini, who scuppered the previous coalition to bring about fresh elections and force his party’s coalition partner out of government. Argentina is heading for another state bankruptcy. After opposition leader Alberto Fernandez and former president Cristina Kirchner won the preliminary elections, the Macri government suspended interest payments due on state debt in local currency. In Hong Kong, anti-extradition protests continued for the whole month, and seem to be as powerful as ever. The protest movement is exerting strong pressure not only on the local economy and civil society in the Special Administrative Region, but also on the government in Beijing, which is struggling to remain calm. The trade conflict between the US and China escalated further, with new and higher tariffs being imposed by both sides. The Chinese central bank’s devaluation of the renminbi is fuelling concerns that the trade conflict could turn into a currency war.

The renunciation of the post-WWII world order, with its choreographed diplomacy and its institutionalised rules and regulations, in favour of unilateral decision-making and escalation mechanisms and the use of social media for communications, has already taken its toll. As a consequence, market participants are becoming more cautious both in the real economy and in the financial sector. Leading indicators such as the global purchasing managers’ indices (PMIs) in the manufacturing sector are deteriorating or remain at recession levels. Having said that, all in all, a recession has failed to materialise both in the US and in the eurozone.

Markets worldwide have reacted to the plethora of bad news in the form of a wholesale flight to safe havens. Most European sovereign bond yields dropped below zero and the US Treasury curve recently inverted. The latter is regarded as an indicator of recession. There was a big sell-off of equities at the beginning of August, but they recouped some of the losses later in the month, driven by the hope that the trade conflict between the US and China could be resolved in the near term after all.

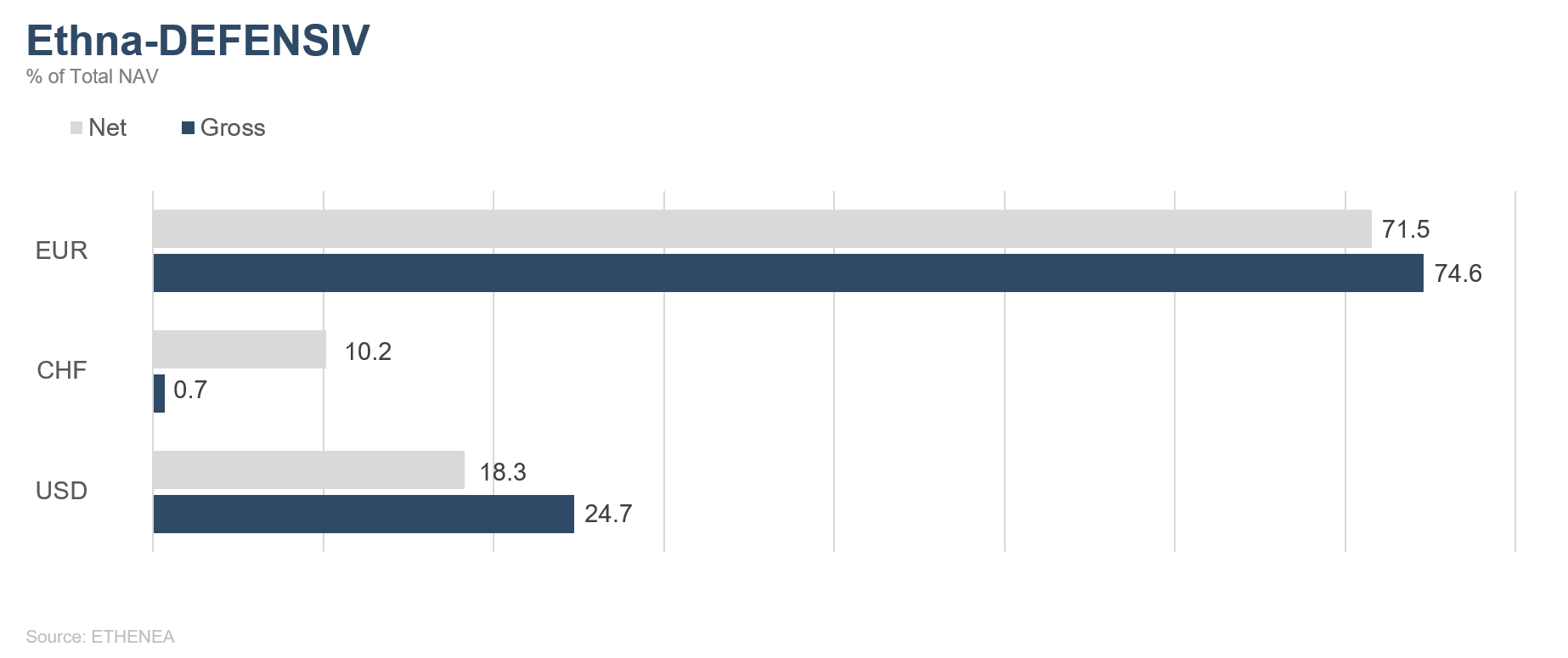

In this tug-of-war between fear and hope, the Ethna-DEFENSIV returned 1.81% in August, benefiting from the global increase in value of safe-haven assets. The high-quality bond portfolio contributed 1.33% and the long-term interest rate futures positions in US Treasuries and Gilts contributed 0.30% to performance for the month. The performance of the currency positions in USD and Swiss francs was also positive, contributing 0.27%. We will continue to manage the portfolio with care and attention in future. We feel it is highly likely that the current uncertainties will persist, but we cannot rule out a recovery of risk assets in the short term; e.g. because the probability of a resolution of the trade conflict could increase. For that reason, we have sold our long position in Treasuries and Gilt futures in its entirety in order to tactically protect the portfolio against rising interest rates in the short term. We remain approx. 10% invested in Swiss francs and hold around 18% of the fund volume in US dollar positions (as at 30/8/2019). We feel confident that interest rates will remain low in the long term, or could even fall further. We therefore retain our positive view of long-term bonds in non-cyclical sectors, which are issued by issuers with solid balance sheets and sound business models.

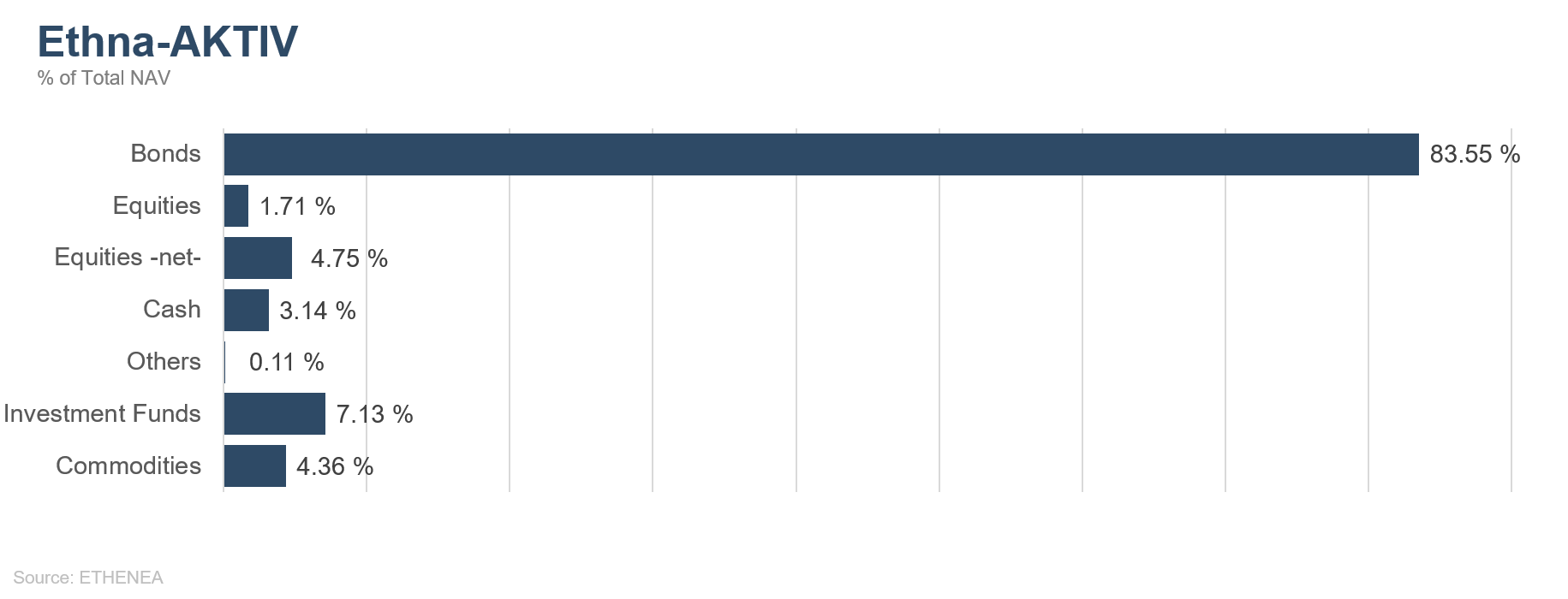

Ethna-AKTIV

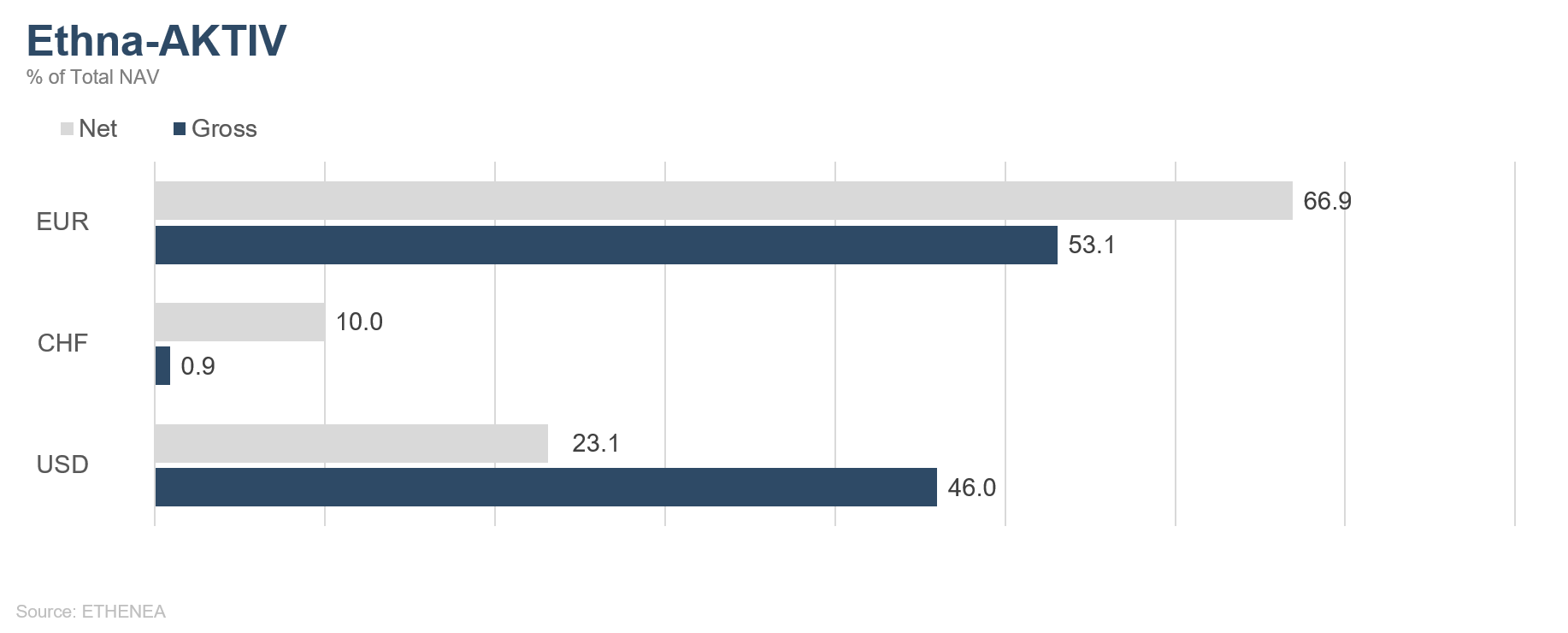

The month of August was, again, all about a re-escalating trade conflict. The overtures made towards the end of the month were not enough to make up for the losses on global equity markets. Meanwhile, we have become firmly convinced that this exchange of rhetoric without any real rapprochement between the two world powers will continue until the next US election. Even if another break in proceedings should arise, we can assume that the current tariffs and the uncertainty about those to come have already caused considerable damage in the form of lower growth on both sides of the conflict. That said, we do not believe that this slowdown in growth is enough to plunge the largest economy in the world into recession in the next twelve months. For this reason, at the moment we are not attaching as much importance to that oft-mentioned indicator of recession – the inversion of the US yield curve – as this inversion came about more as a result of a sharp decline in long-term interest rates than too fast an increase in short-term interest rates. Financing conditions in the US are none too restrictive at the moment, and further interest rate cuts can even be expected in the near future. Thus, as long as there is no external shock, we continue to expect moderate growth in the United States. The situation in Europe is somewhat different: with Germany having driven growth in recent years and now posting negative growth in the second quarter, a technical recession looks very likely. Due to this growth differential between Europe and the US, we further increased our allocation in US corporate bonds to above 44% and, at the same time, expanded the US dollar allocation to 23% (as at 30/8/2019).

Last month was an unusually eventful month in terms of movements in prices. The risk-off sentiment, from which our 4.4% gold position benefited with a price gain of more than 8%, also led to fresh record lows in 30-year US Treasuries and to the dollar exceeding the important mark of 7 renminbi.

While we will hold onto the position in the precious metal in the longer term as well, over the course of the month we took all profits on our active duration management due to the fresh acceleration in the movement of interest rates. Since, however, we still expect interest rates to fall further, we will increase portfolio duration again after consolidation.

While the fund’s equity allocation was already below average in July, we reduced it still further due to the escalation in the trade conflict at the beginning of August, as mentioned above. This is being addressed in the context of the current sideways movement. By doing so, we are trying to rid ourselves of the many negative factors which, to a large extent, are already priced in; we also want to seize opportunities again outside of the fixed-income and currency segments.

All in all, our positioning proved very positive in what was a volatile August, and the Ethna-AKTIV demonstrated its stabilising effect once again.

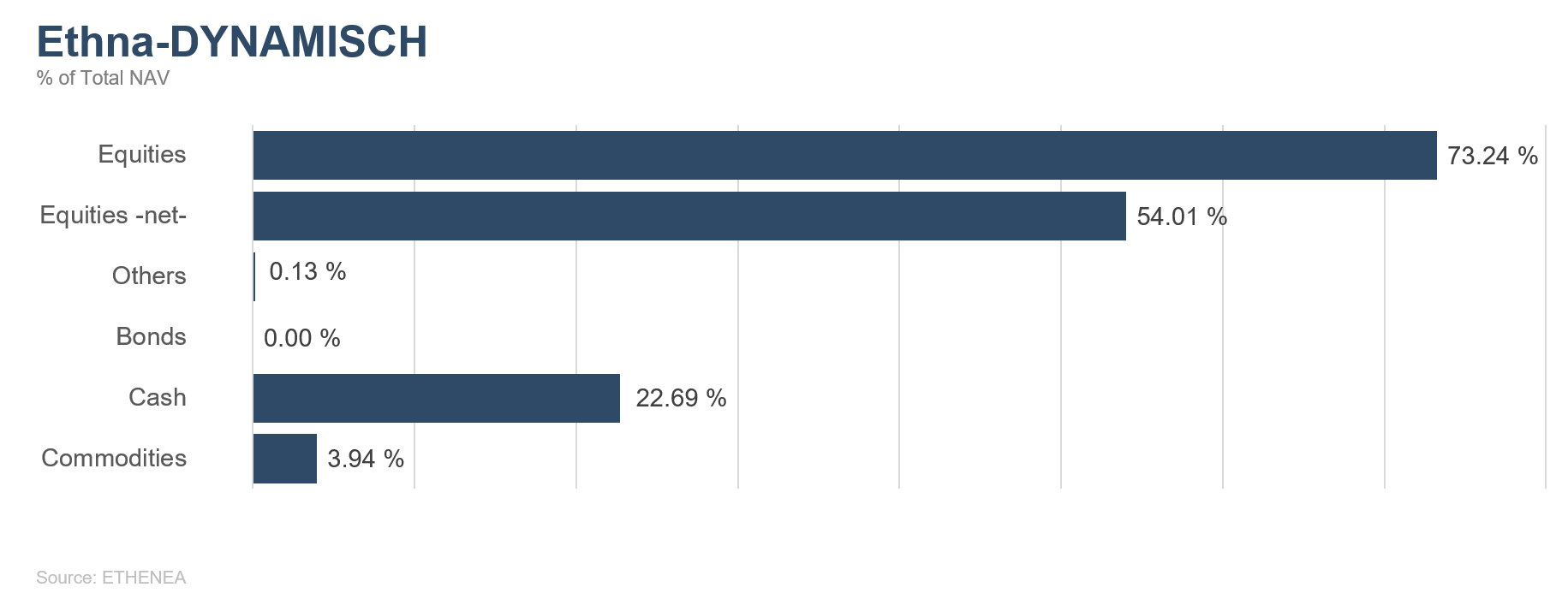

Ethna-DYNAMISCH

A market without a definitive trend features a zig-zag pattern, with strong movements upwards and downwards. Following the rally in June and July, equity prices fell very sharply in August and the lack of trend in the market became even more entrenched. The reasons why are manifold and not really new. The global economic slowdown is continuing, bringing some key EU countries to the brink of recession. For example, all of the economic barometers (especially in Germany) have deteriorated – some sharply – and are signalling a chilly economic climate in the manufacturing sector. The good news is that stock exchanges are scarcely reacting negatively to this, as much of it is already priced in. The US managed to buck the downward trend for a long time, but here too, after a 10-year upturn, signs are gradually emerging that growth has reached its limit. The unpredictability of US foreign policy – e.g. trade conflict – is impacting on the global economy. The export-led regions Europe and China are the most affected by this. Just one critical word or a single tweet on the subject of the trade conflict can still rattle the markets, as happened on 23 August, when a negative comment from Trump about China caused the S&P 500 to fall 3%. The European markets’ reaction to the falls in prices in the US was mild. Cyclical equities in particular have lost an enormous amount of value on this side of the Atlantic, and a lot of the negatives had already been priced in. Despite the fact that the policies of the central banks are supportive, some countries will enter at least a technical recession in the coming months (which has, however, already been priced in by the equities concerned). Meanwhile, investor pessimism is reaching a high point and the liquidity that has built up is seeking returns. Sooner or later, this money will end up back in the equity market. Like August, September is classed as one of the more difficult months. Should further weakness in the global stock markets arise, we will top up the equity allocation. The foundation for bottoming out and an end to the lack of trend has been laid.

In order to increase the allocation, we have already begun making purchases in the equity portfolio. New additions in August were: Associated British Foods, Inditex and Demant. Only insiders are likely to be familiar with the name Associated British Foods, which is the parent organisation of the rapidly expanding fast-fashion chain Primark. ABF also operates in the food business. Both divisions account for about half of group sales. Behind the Spanish Inditex name are brands such as Zara and Massimo Dutti. With logistics that are unique in the industry, Inditex has been on a growth trajectory for years and is regarded as the benchmark in the fashion industry for speed, efficiency and profitability. We took advantage of the weak price in recent weeks to stock up this position. Another new addition to the portfolio is the Danish Demant A/S, one of the leading hearing aid manufacturers in the world.

The fund’s hedging strategy once again proved successful in August; both the options and the futures made a substantial contribution to portfolio stability. As prices fell, a 10% hedge in Dax futures was completely closed. We also adjusted the existing options, which resulted in an increase in the investment quota. The net equity allocation at the end of the month was thus 54%.

Even though the economy is slackening, stock exchanges are no longer reacting negatively to poor economic data. For us, this is essentially a good sign that the correction has very nearly bottomed out. Our outlook for the further course of the year is promising and we expect that the fund’s equity allocation will remain substantial.

Figure 3: Portfolio structure* of the Ethna-DEFENSIV

Figure 4: Portfolio structure* of the Ethna-AKTIV

Figure 5: Portfolio structure* of the Ethna-DYNAMISCH

Figure 6: Portfolio composition of the Ethna-DEFENSIV by currency

Figure 7: Portfolio composition of the Ethna-AKTIV by currency

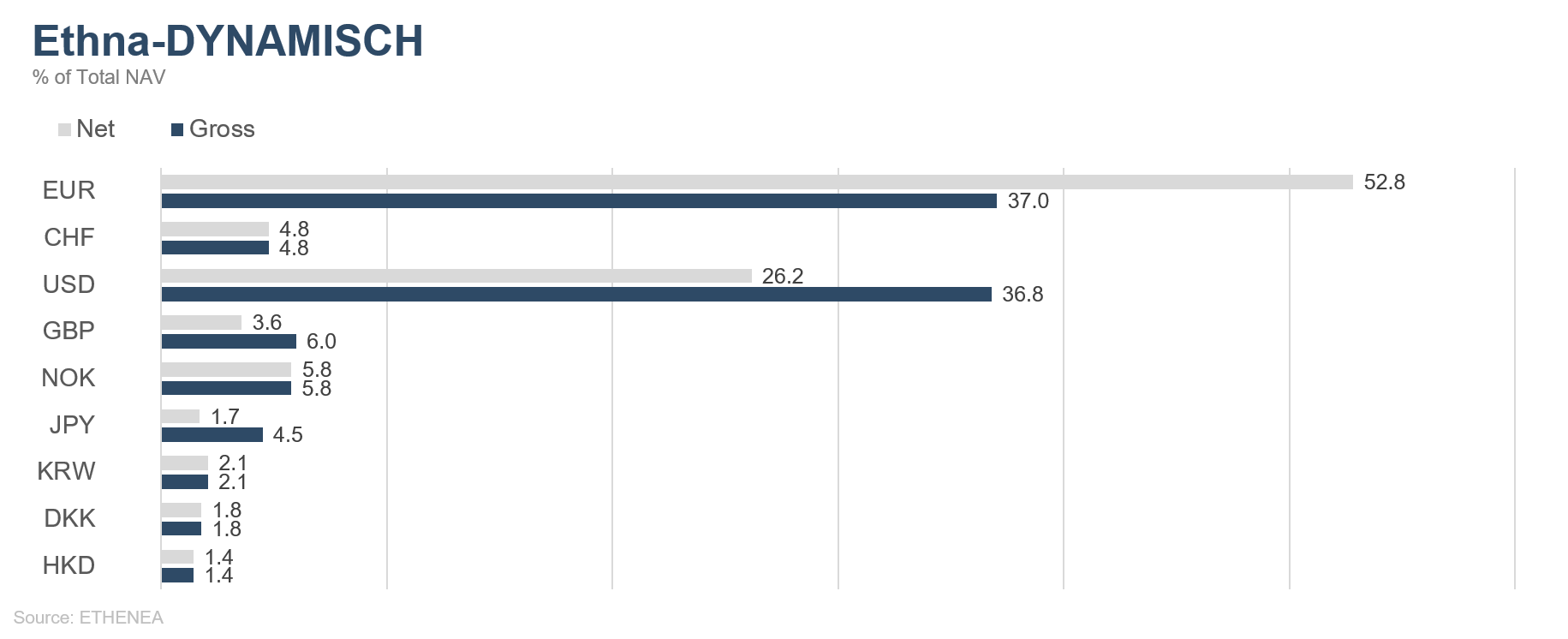

Figure 8: Portfolio composition of the Ethna-DYNAMISCH by currency

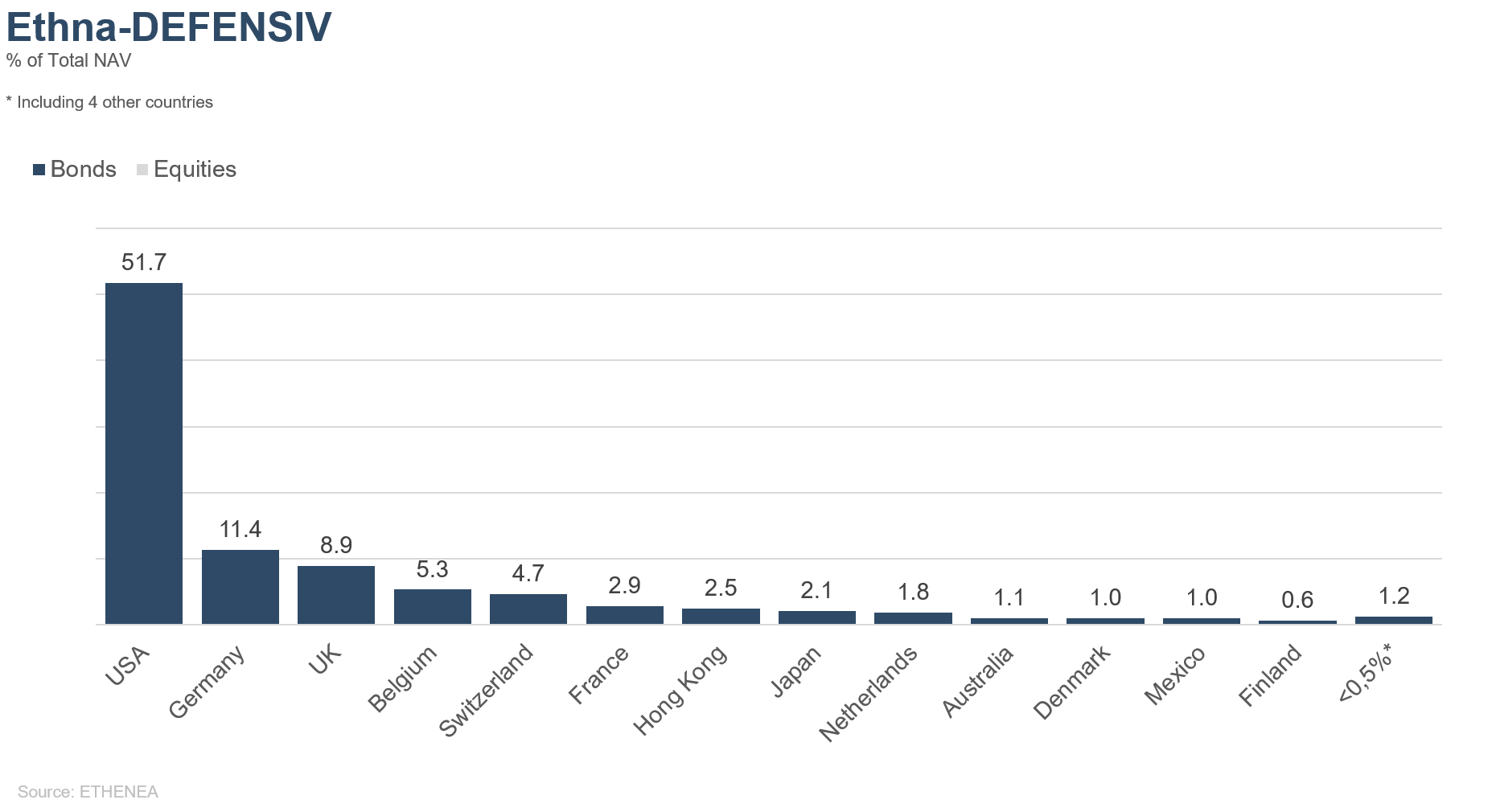

Figure 9: Portfolio composition of the Ethna-DEFENSIV by country

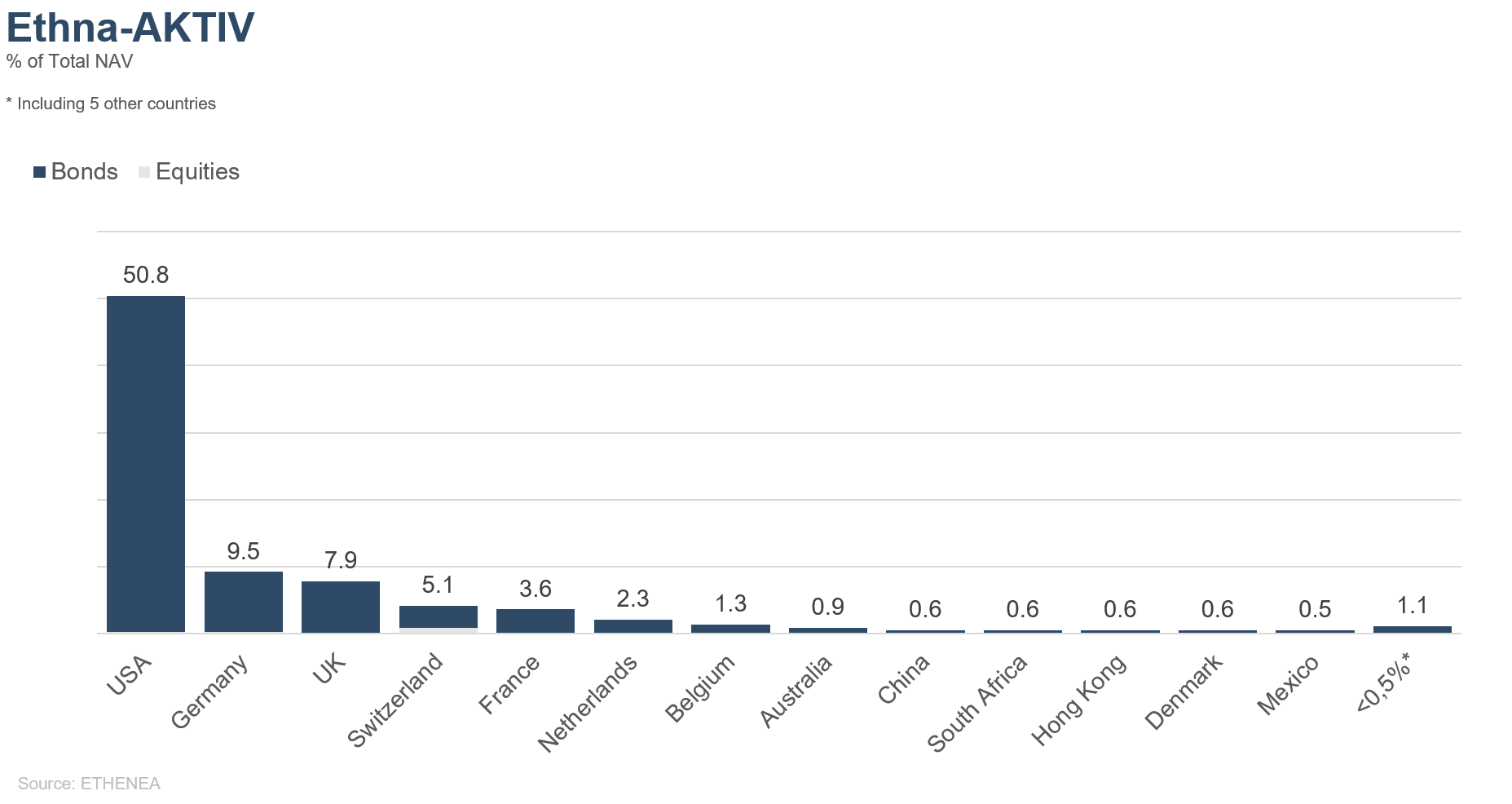

Figure 10: Portfolio composition of the Ethna-AKTIV by country

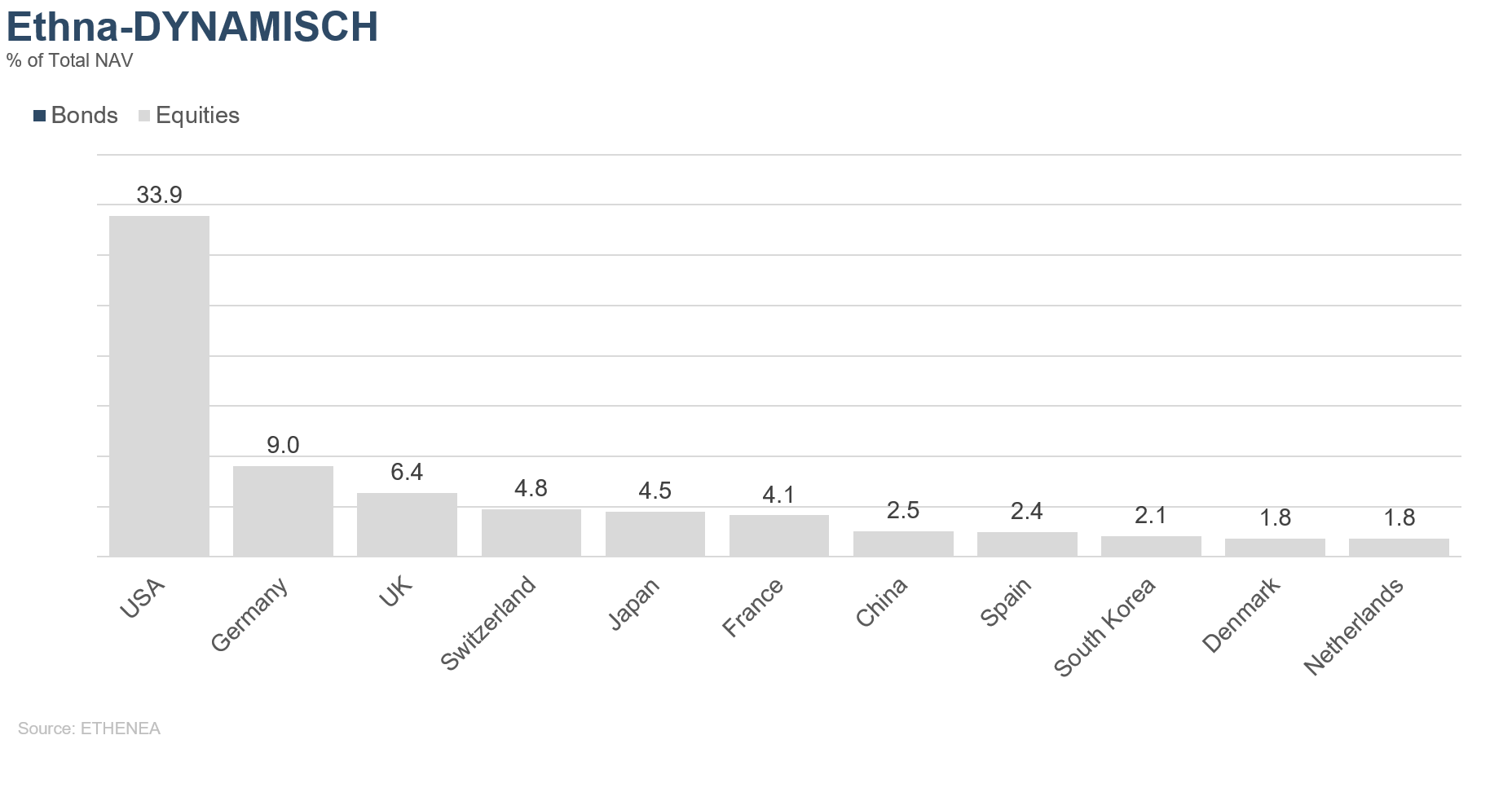

Figure 11: Portfolio composition of the Ethna-DYNAMISCH by country

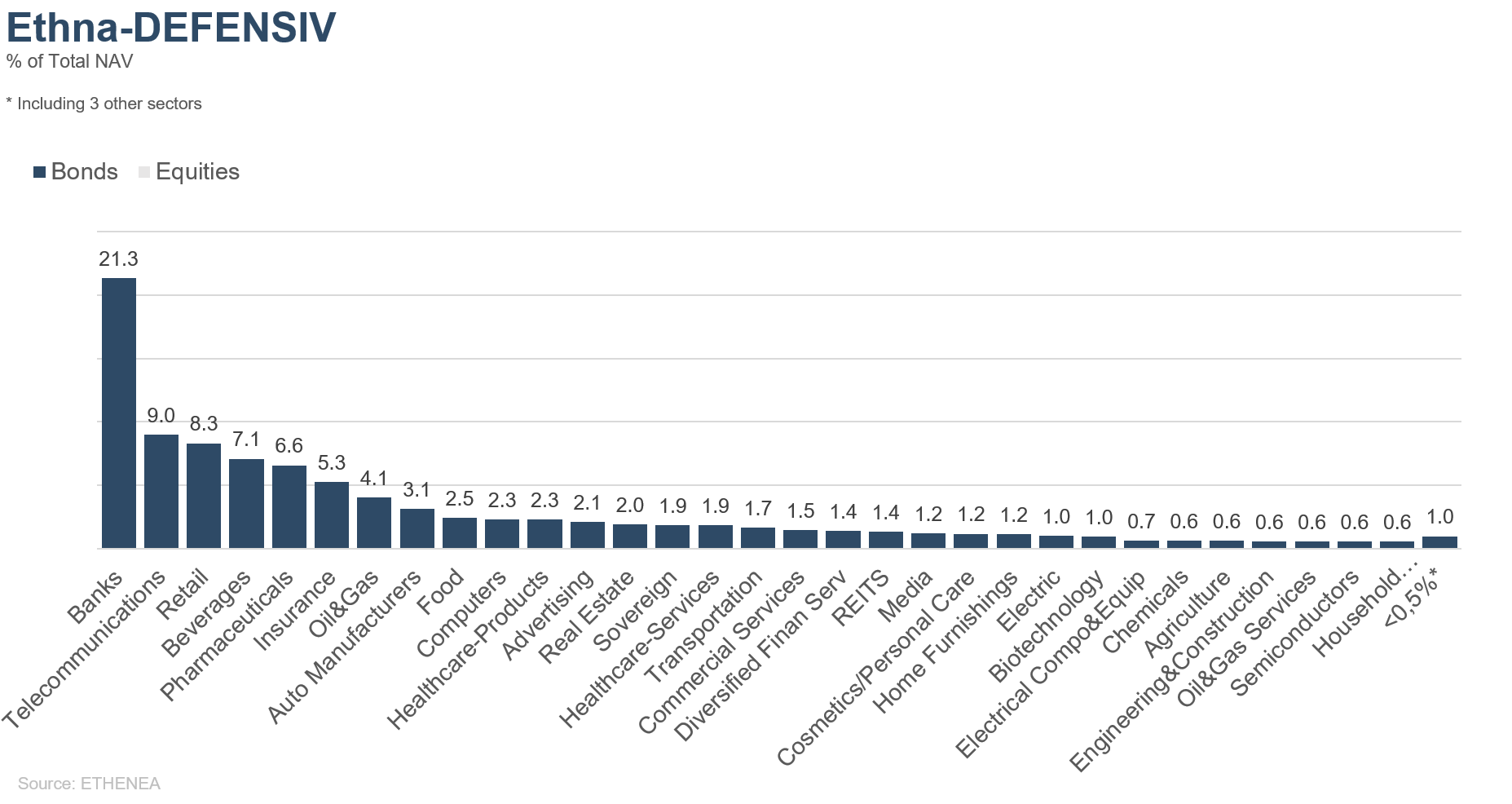

Figure 12: Portfolio composition of the Ethna-DEFENSIV by issuer sector

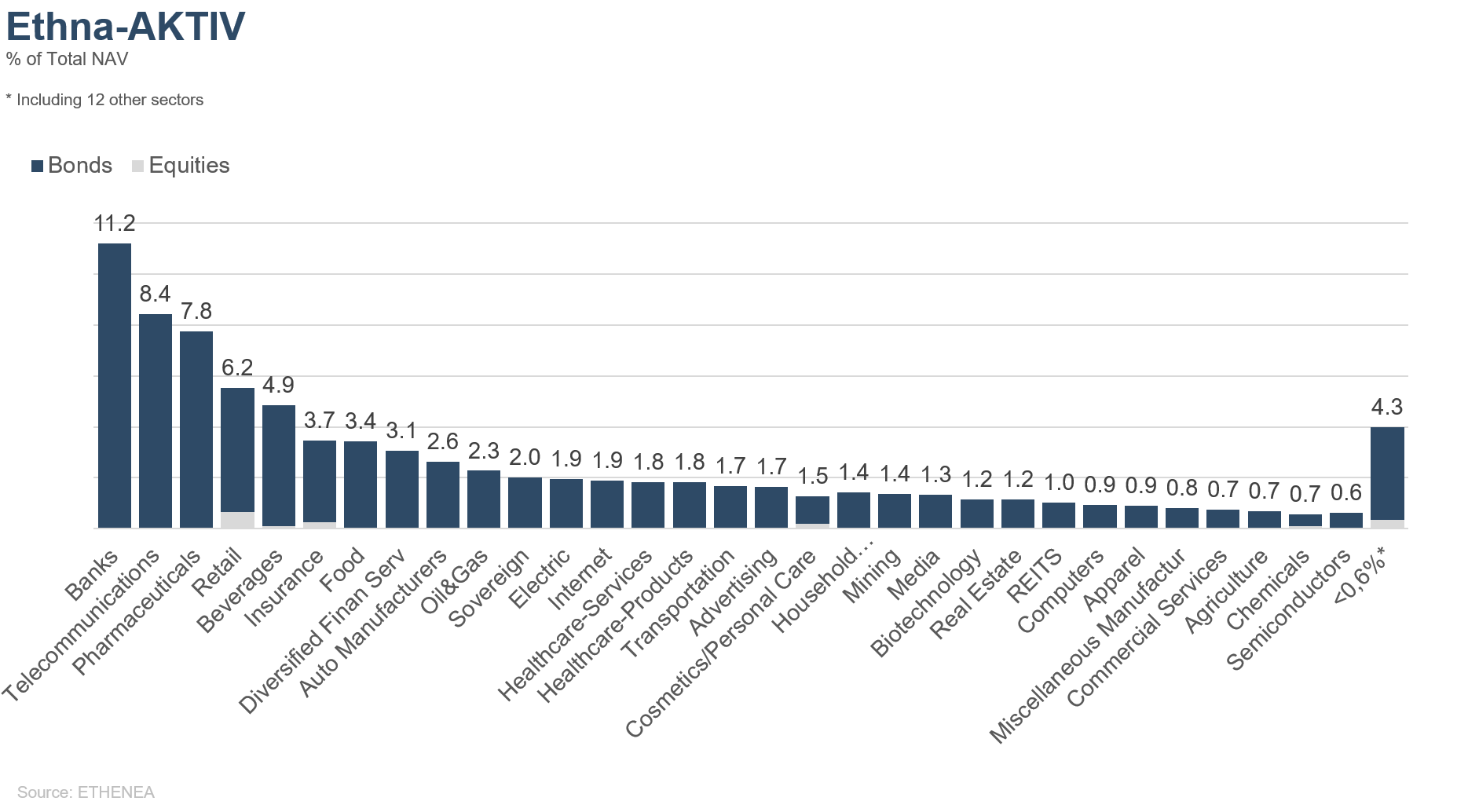

Figure 13: Portfolio composition of the Ethna-AKTIV by issuer sector

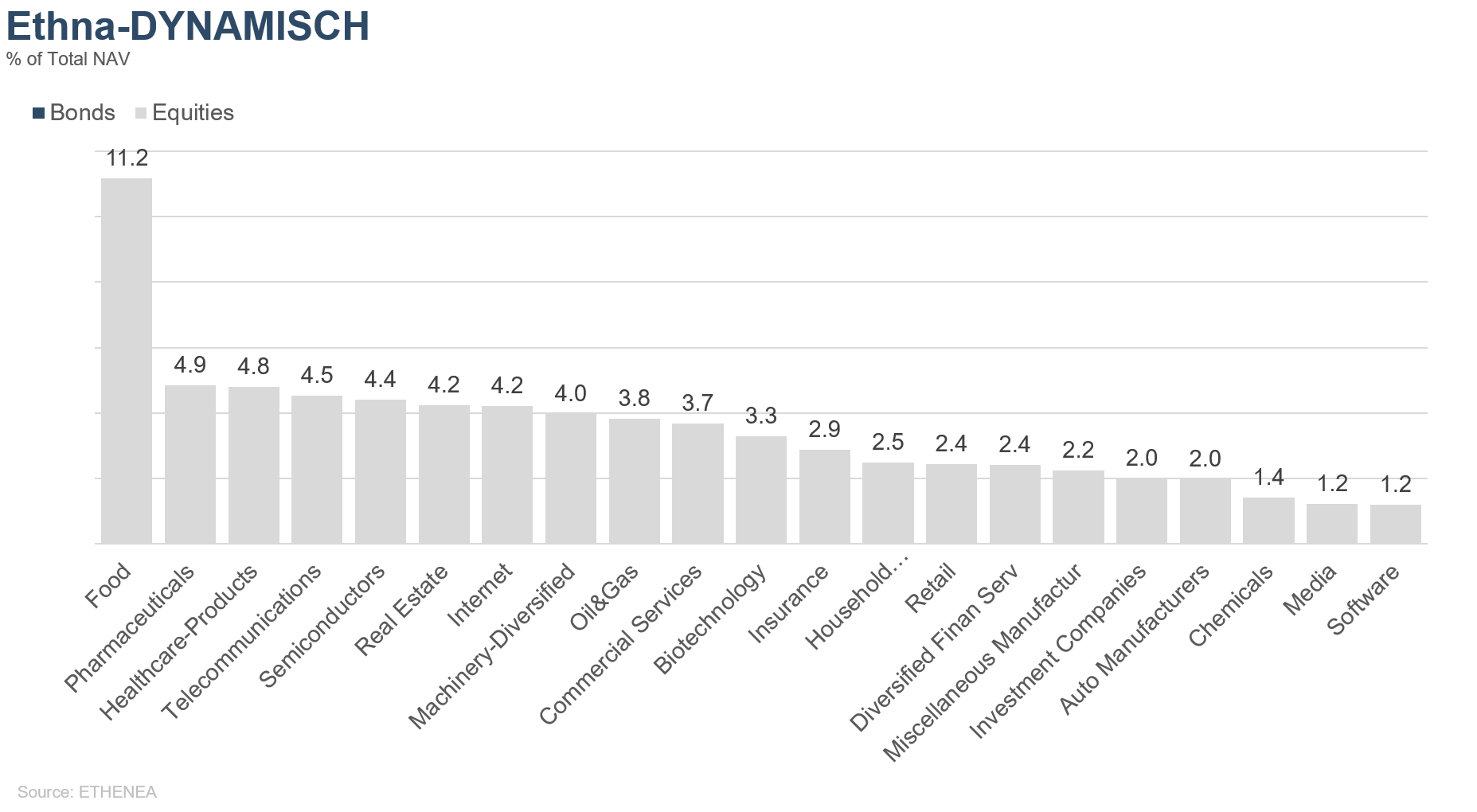

Figure 14: Portfolio composition of the Ethna-DYNAMISCH by issuer sector

* “Cash” comprises term deposits, call money and current accounts/other accounts. “Equities net” comprises direct investments and exposure resulting from equity derivatives.

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

This marketing communication is for information purposes only. It may not be passed on to persons in countries where the fund is not authorized for distribution, in particular in the USA or to US persons. The information does not constitute an offer or solicitation to buy or sell securities or financial instruments and does not replace investor- and product-related advice. It does not take into account the individual investment objectives, financial situation, or particular needs of the recipient. Before making an investment decision, the valid sales documents (prospectus, key information documents/PRIIPs-KIDs, semi-annual and annual reports) must be read carefully. These documents are available in German and as non-official translations from ETHENEA Independent Investors S.A., the custodian, the national paying or information agents, and at www.ethenea.com. The most important technical terms can be found in the glossary at www.ethenea.com/glossary/. Detailed information on opportunities and risks relating to our products can be found in the currently valid prospectus. Past performance is not a reliable indicator of future performance. Prices, values, and returns may rise or fall and can lead to a total loss of the capital invested. Investments in foreign currencies are subject to additional currency risks. No binding commitments or guarantees for future results can be derived from the information provided. Assumptions and content may change without prior notice. The composition of the portfolio may change at any time. This document does not constitute a complete risk disclosure. The distribution of the product may result in remuneration to the management company, affiliated companies, or distribution partners. The information on remuneration and costs in the current prospectus is decisive. A list of national paying and information agents, a summary of investor rights, and information on the risks of incorrect net asset value calculation can be found at www.ethenea.com/legal-notices/. In the event of an incorrect NAV calculation, compensation will be provided in accordance with CSSF Circular 24/856; for shares subscribed through financial intermediaries, compensation may be limited. Information for investors in Switzerland: The home country of the collective investment scheme is Luxembourg. The representative in Switzerland is IPConcept (Suisse) AG, Bellerivestrasse 36, CH-8008 Zurich. The paying agent in Switzerland is DZ PRIVATBANK (Suisse) AG, Bellerivestrasse 36, CH-8008 Zurich. Prospectus, key information documents (PRIIPs-KIDs), articles of association, and the annual and semi-annual reports can be obtained free of charge from the representative. Information for investors in Belgium: The prospectus, key information documents (PRIIPs-KIDs), annual reports, and semi-annual reports of the sub-fund are available free of charge in German upon request from ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxembourg, and from the representative: DZ PRIVATBANK AG, Niederlassung Luxemburg, 4, rue Thomas Edison, L-1445 Strassen, Luxembourg. Despite the greatest care, no guarantee is given for the accuracy, completeness, or timeliness of the information. Only the original German documents are legally binding; translations are for information purposes only. The use of digital advertising formats is at your own risk; the management company assumes no liability for technical malfunctions or data protection breaches by external information providers. The use is only permitted in countries where this is legally allowed. All content is protected by copyright. Any reproduction, distribution, or publication, in whole or in part, is only permitted with the prior written consent of the management company. Copyright © ETHENEA Independent Investors S.A. (2025). All rights reserved. 03/09/2019