Portfolio Manager Update

Ethna-DEFENSIV

Key points at a glance

- Yields are near the peak of the current hiking cycle

- Fund delivers positive performance despite rising yields

- Short positions in futures on German and U.S. sovereign bonds reduced to 10%

- Distribution: back to paying out more than the minimum

- Cautious increase in portfolio duration a possibility in the foreseeable future

30 April 2024 – In April, the rising trend in yields along the entire length of the yield curve continued from previous months. Ever since yields on 10-year sovereign bonds fell to 1.9% in Germany and to 3.8% in the U.S. at the end of 2023, they have been climbing continually. Inflation figures in the U.S. did not come down as investors had expected. April saw the PCE price gauge come in at 2.7% for March, an increase over February’s figure of 2.5%. Of course, this is the wrong direction for the Fed, leading U.S. central bankers to adopt a much more hawkish tone. They even cast doubt on the possibility of interest rate cuts in the U.S. before the end of the year. This was a contributing factor in yields rising to year-to-date highs both in the U.S. and Germany. In our view, these highs are very close to the peak of this cycle.

The next decisions taken by both the Fed and the ECB will concern interest rate cuts. In Europe, the ECB signalled relatively clearly that the first interest rate cut will take place in June. Something extraordinary would have to happen for the members of the ECB to change their minds. In the U.S., the situation is a bit trickier due to persistent inflation. But we are of the opinion that the Fed will effect at least one rate cut before the end of 2024. Against this backdrop, and to take profits (the fund has delivered a positive performance despite rising yields), we gradually reduced our short positions in futures on German and U.S. sovereign bonds from 20% to 10% over the course of the month. Furthermore, fund distribution took place in April, with the fund back to paying out more than the minimum again (1.5%): approx. 2.32% in the A class. Other Ethna-DEFENSIV parameters remained relatively unchanged over the course of the month: we remain conservatively invested in high-quality short-dated corporate bonds denominated in euro.

We can envisage cautiously increasing the portfolio duration in the near future. As already mentioned, yields are nearing a plateau, and the next logical step would be a shift into the longer end of the yield curve so as to benefit from falling yields along with the central banks’ rate cuts. Where (on what markets), when and to what extent we increase duration will depend entirely on the current assessment of the market. At the moment, bonds with maturities after 2030 make up only a small portion of the portfolio, but it is getting nearer the time to increase portfolio duration.

Fund positioning

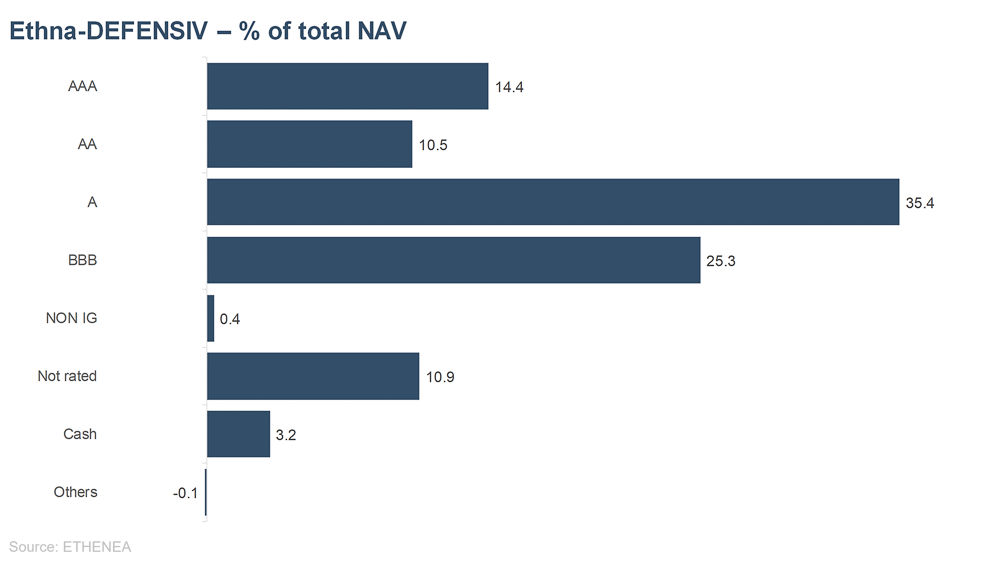

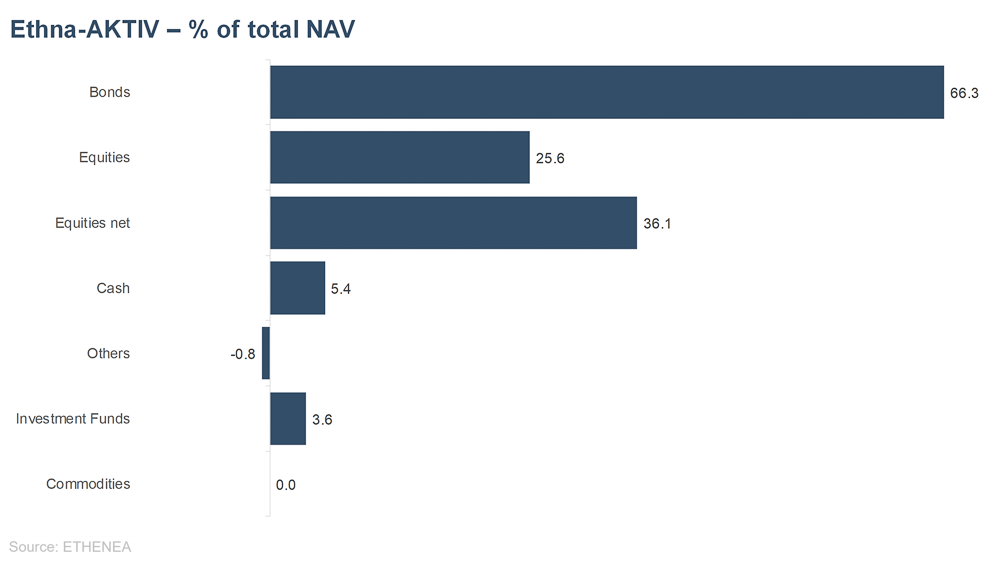

Figure 1: Portfolio structure* of the Ethna-DEFENSIV

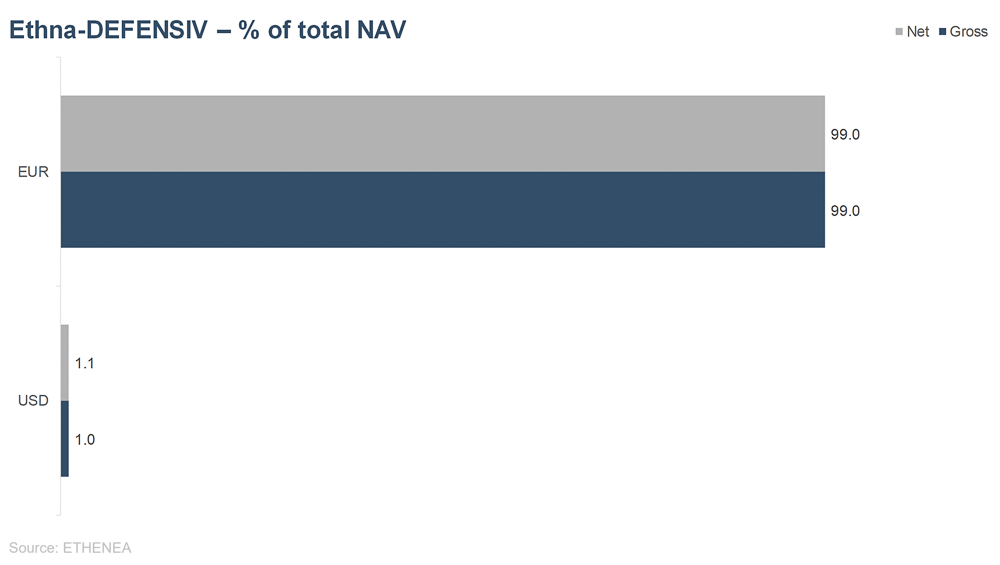

Figure 2: Portfolio composition of the Ethna-DEFENSIV by currency

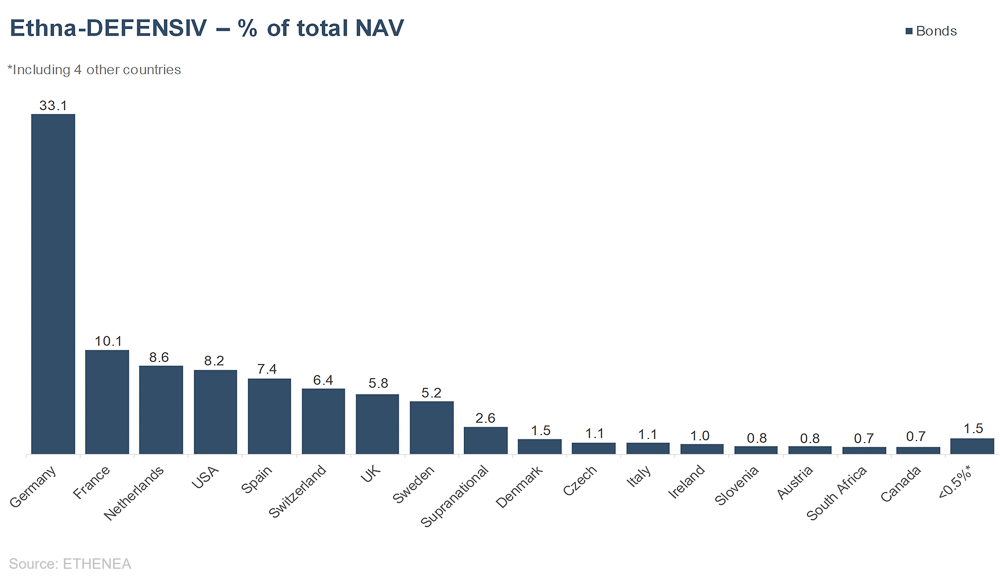

Figure 3: Portfolio composition of the Ethna-DEFENSIV by country

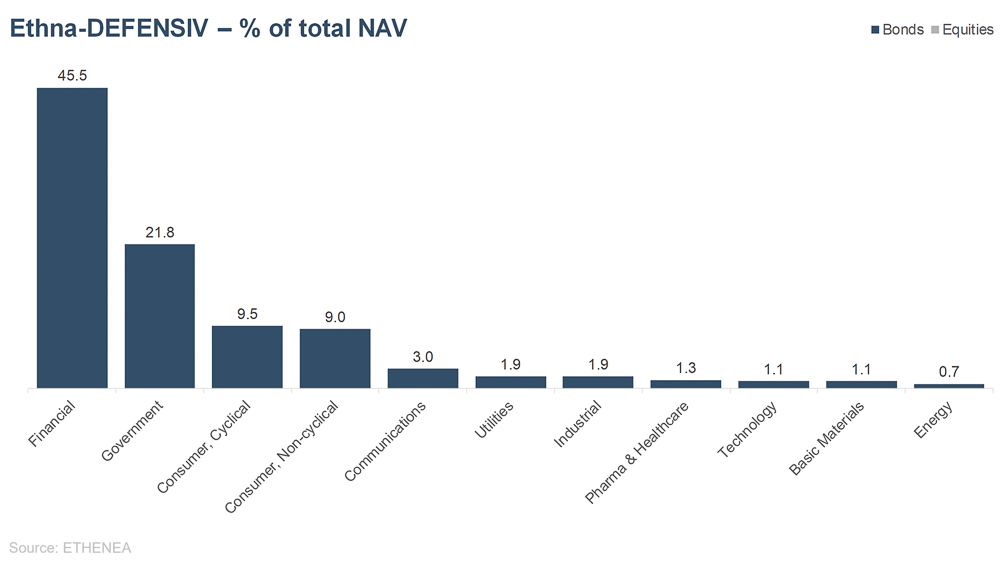

Figure 4: Portfolio composition of the Ethna-DEFENSIV by issuer sector

Ethna-AKTIV

Key points at a glance

- Portfolio remains geared towards an environment of moderate growth, falling but stubborn inflation and a rising stock market trend.

- At 35%, the equity component is in neutral territory, and is exclusively invested in US large caps

- High quality and short maturities continue to characterise the bond portfolio. Modified duration is 1.2.

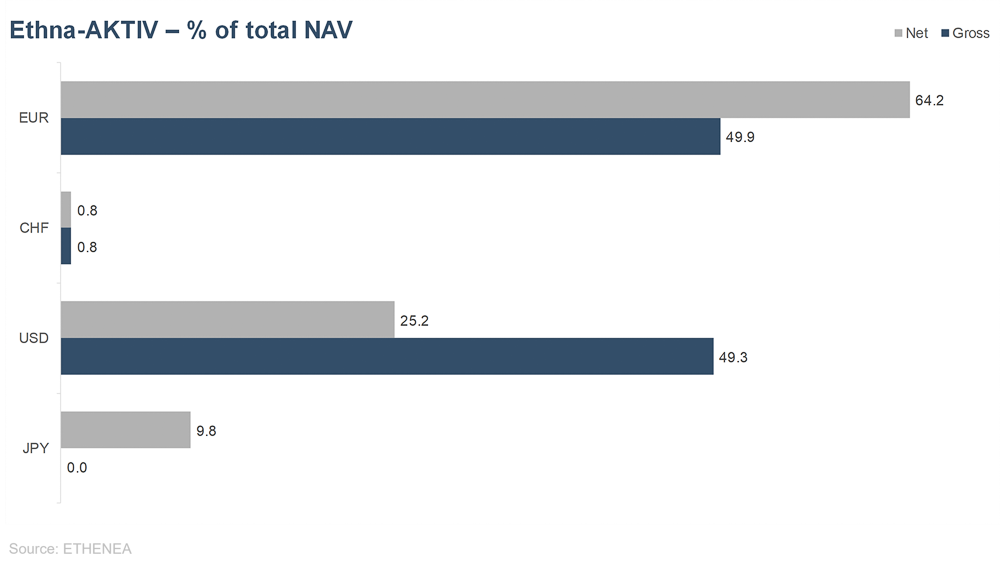

- 15% position in the Japanese yen reduced to 10%; portfolio still has USD exposure of 25%.

30 April 2024 – The month of April held an array of fundamental, macro-economic and, last but not least, geopolitical factors for capital markets. Altogether they caused volatility to pick up. As soon as the month started, the first correction to speak of since the beginning of the rally in November set in on the equity market. This was spurred on by another flare up in the conflict in the Middle East, which took the form of attacks and counterattacks between Iran and Israel. Fortunately, this conflict has not yet escalated further. What was notable about the reactions from the market was not the sell-off in equities and the initial flight to safe havens such as U.S. Treasuries but the relatively quick resumption of the original rising trend in interest rates. For example, 10-year U.S. Treasuries have now returned to a level that caused stress for equities last summer. Even though earnings season has so far gone better than expected, this presents a headwind for equities’ continued performance that must not be underestimated. Especially since, in all likelihood, there won’t be any added tailwind either from all that many interest rate cuts on the part of Western central banks. Against the backdrop of ongoing inflation, expectations for interest rate cuts this year have fallen to less than 1.5 in the U.S. and just under three in Europe.

In these circumstances, a solidly constructed and well balanced portfolio was called for. This is precisely why the Ethna-AKTIV did well. Both the USD position and the interest rate overlay made a positive contribution to performance in a challenging month, containing the need for additional risk management measures. Quite the contrary: after Israel’s most recent missile attack, we increased to 35% the equity allocation that had been reduced to 25% at the beginning of the month, as we see the current consolidation in the equity market as just that – a consolidation – and not the beginning of a bear market. Only slight changes were made to the basic composition of the equity portfolio. The only urgent need for action we saw was with regard to the interest rate overlay. When the aforementioned geopolitical escalation began, we quickly reversed the reduction in interest rate sensitivity, as a potential flight to safety would have flown in the face of our positioning towards rising interest rates. However, as this movement did not materialise, we reduced modified duration to 1.2. Looking ahead, communications from and the actions of central banks will be interesting. Western central banks have little scope to cut interest rates at the moment due to persistent inflation, and the resulting “higher for longer” mantra is supporting the U.S. dollar above all. The yen was particularly hard hit last month. With the yen at a 34-year low against the U.S. dollar, the Japanese central bank felt compelled at month-end to intervene in the currency market. As they began this intervention much later than we expected, the yen position had already been reduced over the course of the month by 5% down from 15%. We are currently waiting to see what happens, but expect a turnaround in the trend in the short term in favour of the yen.

Fund positioning

Figure 5: Portfolio structure* of the Ethna-AKTIV

Figure 6: Portfolio composition of the Ethna-AKTIV by currency

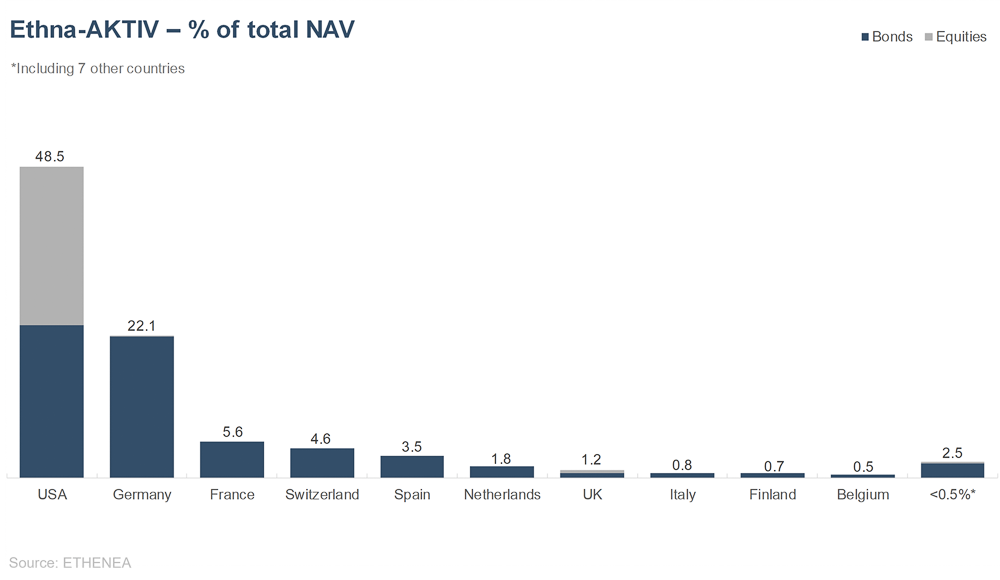

Figure 7: Portfolio composition of the Ethna-AKTIV by country

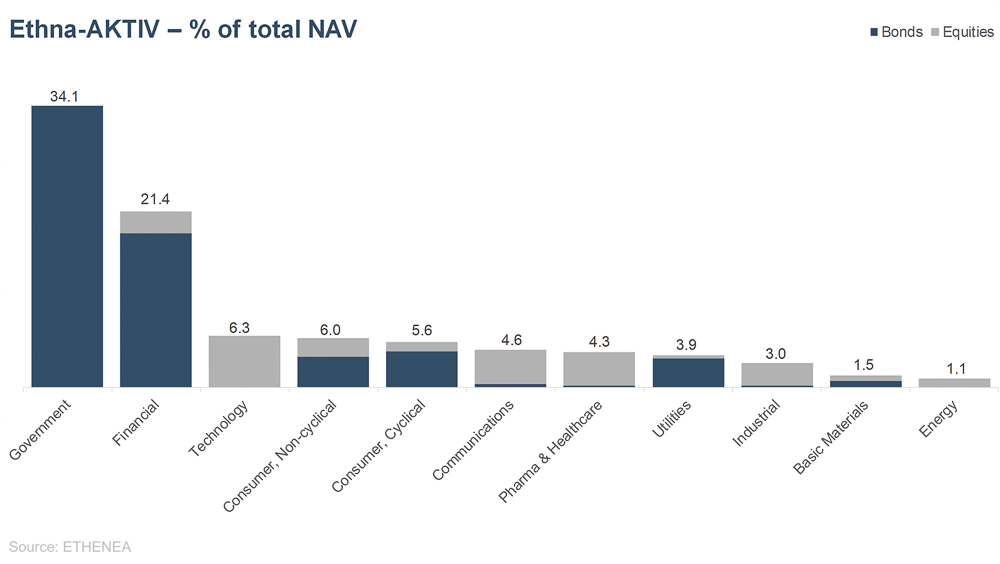

Figure 8: Portfolio composition of the Ethna-AKTIV by issuer sector

Ethna-DYNAMISCH

Key points at a glance

- In April, equity markets underwent the first significant correction this year.

- With its phased hedging of the equity component and good quarterly results from its portfolio stocks, the Ethna-DYNAMISCH bucked the rather unsettled trend.

- Lots of minor portfolio adjustments were made.

- Looking ahead, our assessment of the market remains constructive, even if volatility, which has recently increased, continues to be a factor for some time.

30 April 2024 – After a few comparatively quiet months, capital markets exhibited a little more jitteriness in April. It’s hard to pin down a single trigger. It was more a case of a confluence of higher bond yields, evaporated hopes for interest rate cuts in the U.S., small clouds on the economic horizon, equity prices that have, in some cases, run a little too far ahead, and very high levels of investment in the case of trend-following investors. Compounding this was the justified fear of a further immediate geopolitical escalation in the Middle East. No one factor by itself posed an appreciable danger to the basically constructive outlook, which we have gone into on more than one occasion in the past in our commentary. But altogether these factors were enough to bring the upward trend to a halt.

If we take a closer look at the correction, we see that it was most pronounced in small caps, even though this group was already one of the laggards. Thus, the hotly anticipated comeback of second-tier stocks has once again failed to materialise and many small-cap indices, such as the Russell 2000 in the U.S. and the MDAX in Germany, are back in negative territory since the start of the year. The discounts in valuations we are seeing in this segment do not as yet confirm the slowly improving economic prospects. Equity markets tend to remain divided; into more expensive, high-growth stocks, and cheaper, fundamentally stagnant ones.

Our task as portfolio manager of an asset-managed, equity-focused multi-asset fund is to continually weigh up the respective risks and opportunities – both macro-economic, in selecting an appropriate level of investment and asset allocation (top-down) and micro-economic, in selecting suitable individual stocks (bottom-up). The strengths of both approaches came to light in April.

Against the backdrop described above, at the start of the month we decided based on our top-down analyses to hedge one third of the equity component using derivatives, thereby reducing the Ethna-DYNAMISCH’s level of investment from around 75% to approximately 50%. With this reduced level of risk, we waited out much of the market correction before completely reversing the hedges over the rest of the month.

On the bottom-up side, the focus was on earnings season, which was successful for most companies in the Ethna-DYNAMISCH portfolio. This was the case in particular for some of our highest-weighted names that we regard as suitably attractive, and which we also regularly feature on ETHENEA’s LinkedIn profile under the hashtag #derAktienexpress. Also, thanks to the tailwind from stocks such as Alphabet, ResMed and Unilever, the fund finished up April close to its March value, despite the equity market correction in the intervening month. In parallel, over the course of the month, we made a number of adjustments to the weight of individual positions in order to reflect the risk-reward ratios within the fund that are changing with market volatility.

Only the currency position in the Japanese yen (JPY) opened in March did not perform as positively as hoped. The interest rate and yield differentials relevant for currency pairs drifted further apart and, also, Japan’s rhetoric concerning the increasingly weak JPY was much more restrained than we expected. Having timed the opening of the position well, losses were well contained, despite the JPY hitting a new year-to-date low against the EUR. Nevertheless, we halved the position from its original 10% to 5%. If there are no major foreign exchange interventions by the Japanese authorities in May, we will close the remaining position soon.

On the whole, the capital market climate is likely to remain quite bleak in the months to come. Without doubt, with its high degree of flexibility, its replete toolkit and its solid foundation of attractive individual securities, we consider the Ethna-DYNAMISCH to be well equipped to weather any storms not just adequately but also to actively seize any opportunities that develop from them.

Fund positioning

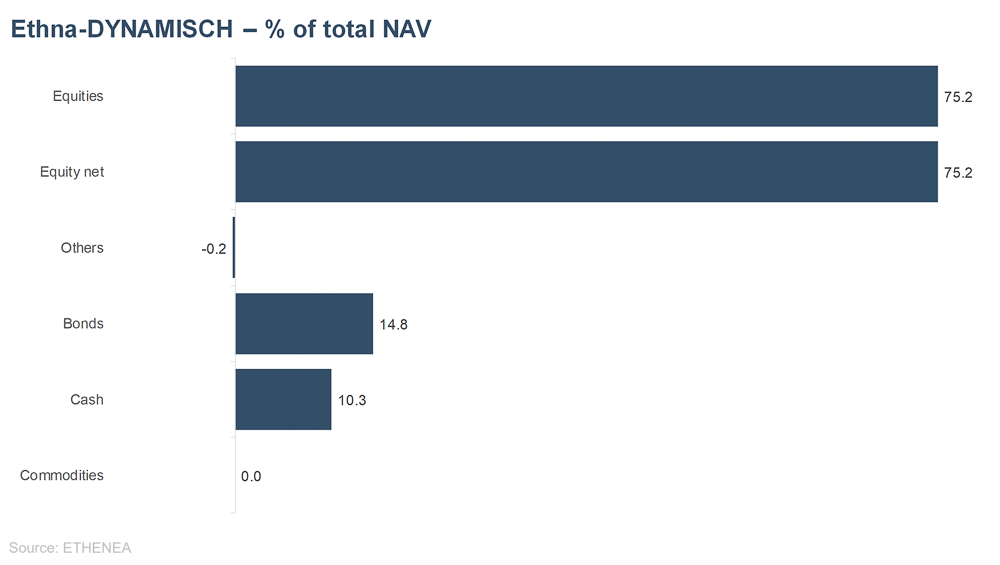

Figure 9: Portfolio structure* of the Ethna-DYNAMISCH

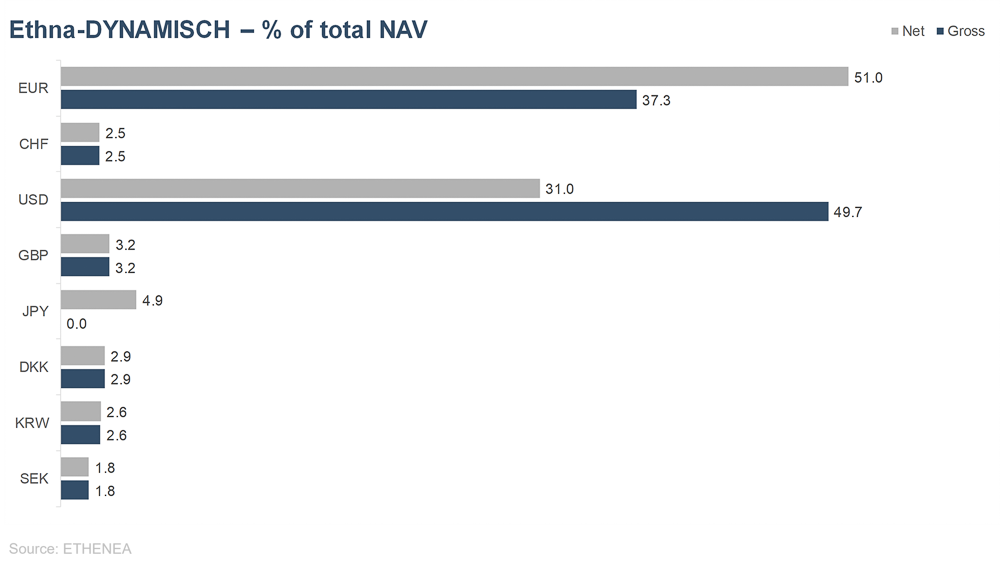

Figure 10: Portfolio composition of the Ethna-DYNAMISCH by currency

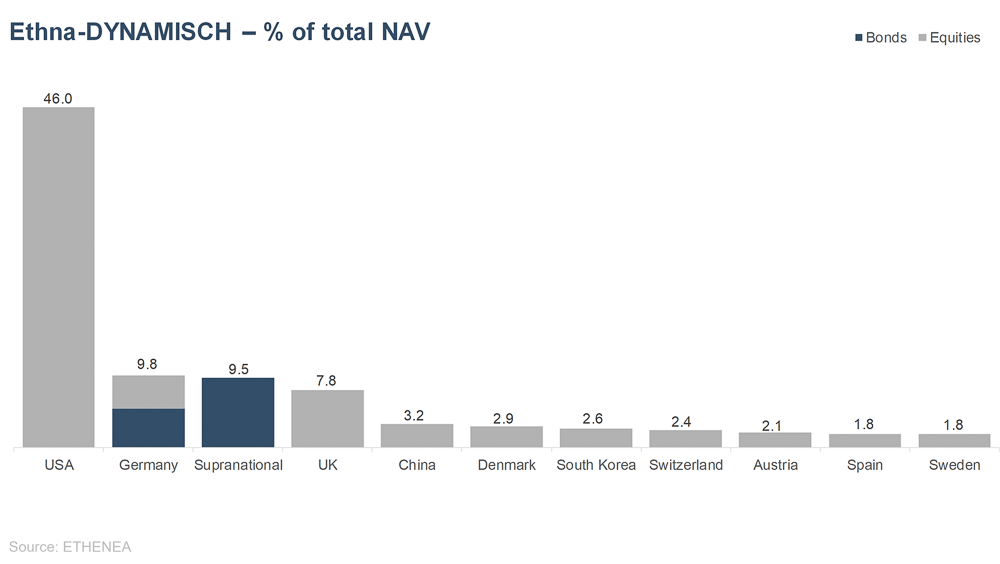

Figure 11: Portfolio composition of the Ethna-DYNAMISCH by country

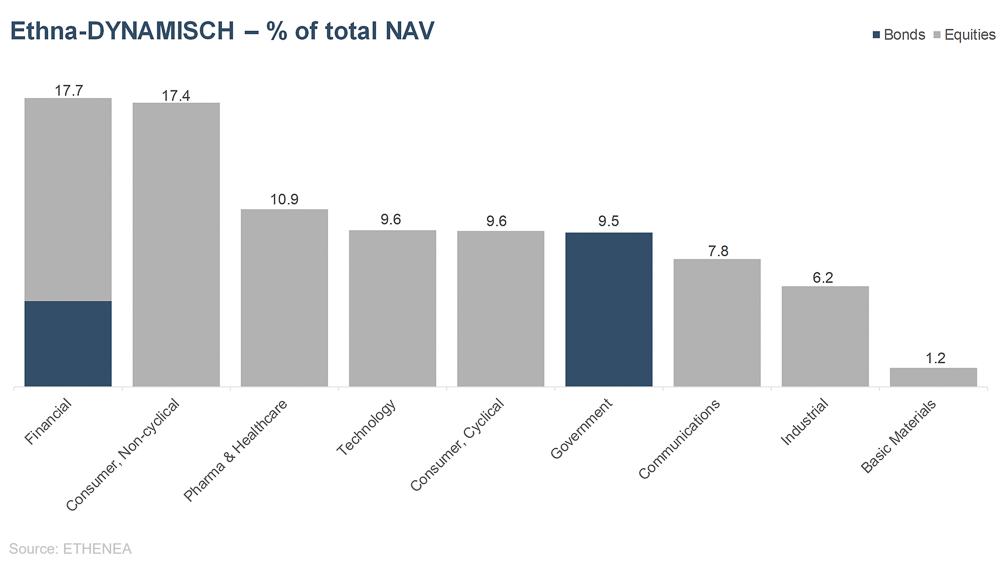

Figure 12: Portfolio composition of the Ethna-DYNAMISCH by issuer sector

* “Cash” comprises term deposits, call money and current accounts/other accounts. “Equities net” comprises direct investments and exposure resulting from equity derivatives.

HESPER FUND – Global Solutions (*)

Key points at a glance

Higher for longer….

- Sticky inflation derailed the rate-cut path expected by the market

- Global yields soared as inflation continues to surprise on the upside

- Stocks broke 5-months winning streak as rate-cut hopes waned

- Chinese equities rebounded as economic activity picks up pace

- Yen swung wildly after first slide past 160 since 1990 catching traders in short squeeze at the end of the month.

- The HESPER FUND – Global Solutions interrupted four months of positive returns.

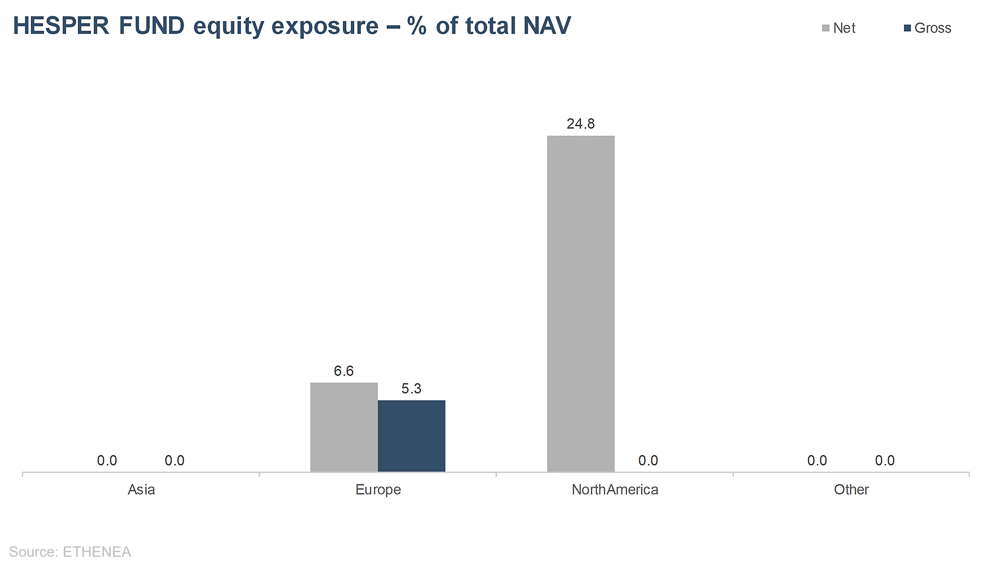

- The HESPER FUND – Global Solutions fine-tuned its portfolio allocation. Net equity exposure was reduced to 30% and duration cut into negative territory (-0.85). In FX, the fund rebuilt the long exposure to the Norwegian krone up to 20%, kept the US dollar at around 50%, and raised GBP short exposure to -40%.

30.04.24 - Rates will stay higher for longer than expected

Rate cuts are still on the Fed’s agenda, but they will likely come much later and less deep than markets discounted at the beginning of the year. For the time being, the direction of travel is still clear but it will take longer and rates will likely not come back to their pre-pandemic level. Sticky inflation, a buoyant economy and fiscal stimulus during an election year make the Fed’s job much harder. The sticky inflation of the first quarter may be more than a simple bump in the road, and even in the Eurozone disinflation is showing signs of stalling while the economy has bottomed out and may start to pick up.

Soaring yields hit equitie

US equities interrupted a five-month rally. Soaring yields, some big techs earnings misses and confusing signs about consumer confidence weighed on stocks during April.

Yields soared up as traders saw the Fed further delaying the first rate cut. Four months of higher-than-expected inflation readings reinforced the idea that the Fed is not yet confident enough that inflation will return sustainably to its target rate of 2%. “Higher for longer” seems to be the new Fed’s mantra.

In the US, the major indices corrected. The S&P 500 plunged 4.2% and the DJIA fell 5%. The tech-heavy NASDAQ lost 4.4% despite Microsoft’s and Alphabet’s strong first quarter earnings. The small cap index Russel 2000 tanked 7.1%.

In Europe, the Euro Stoxx Index fell 3.2% (-2% in USD), while the FTSE 100 rose 2.4% (+1.5% in USD) underpinned by miners and banks. The Swiss Market Index plunged 4% (-5.7% in USD, as the Swiss franc weakened further).

In Asia, stocks were mixed. China’s efforts to stabilise its financial markets showed promising results, as the economy grew better than expected 5.3% during the first quarter. China’s factory activity held up well in April. The Hang Seng jumped by 7.4% and the CSI 300 gained 1.9% (+1.6% in USD). The Korean stock market fell 2% (-4.6% in USD) and the Indian Sensex gained 1.1% (+1% in USD). The Japanese Nikkei plunged 4.9% (-8.1% in USD as the yen slid past 160 against the dollar, presumably forcing BoE intervention last Monday).

Yen weakness is something to handle with care

After 17 years, in March the Bank of Japan ended the era of negative interest rates but gave little indication of further policy tightening. Its dovish tone sent the weak yen drifting even lower and global yields were not dragged up as feared.

For Chinese and Korean exporters, the yen weakness has become a headache, troubling exports and delaying the economic recovery. On the other hand, unwinding the very crowded carry trade against the yen is a delicate task that could unleash extreme volatility through many markets, especially with yields soaring in Western countries.

As the yen slid to its weakest level since 1990, the BoJ stepped up its intervention warnings

The yen sharp and brief jump prompted chatter of BoJ intervention, although the BoJ decided to keep traders in the dark on its actions. Given the very crowded nature of the yen carry trade and the leverage chains financing the trade, yen intervention is a major source of markets’ concerns.

HESPER FUND – Macro Scenario: sticky inflation constrains Fed to delay rate cuts

Central banks are navigating a challenging scenario of uncertain disinflation, tepid economic activity amid political elections, and rising geopolitical tensions. Central banks need to carefully assess the risks of remaining hawkish for too long, with the risk of cutting rates too soon and missing their target. In the US, inflation readings have continued to disappoint, while economic activity remained solid, forcing the Fed to further delay any rate cuts and even raising questions on whether policy is tight enough. In the Eurozone, disinflation has been progressing at a better pace than in the US, but, with economic activity giving initial signs of picking up, it may also start to stall. With the supply side of the inflation equation having already delivered its benefits, we may still need to see some softening in demand to achieve the central banks’ inflation targets. The combination of a strong fiscal support, a healthy labour market, and geopolitical tensions, however, could further delay or even spoil the disinflationary path.

As long as the economy holds up and the carrot of upcoming rate cuts remains in sight, equity markets could shrug off higher yields. However, the Goldilocks scenario of the first quarter of this year seems (at least for the time being) gone and we expect higher volatility ahead.

Positioning and monthly performance

The HESPER FUND – Global Solutions decreased in April (unit class T-6 EUR -1.13%), dragged down by equities and mixed FX bets. YTD, the fund is up 2.38%

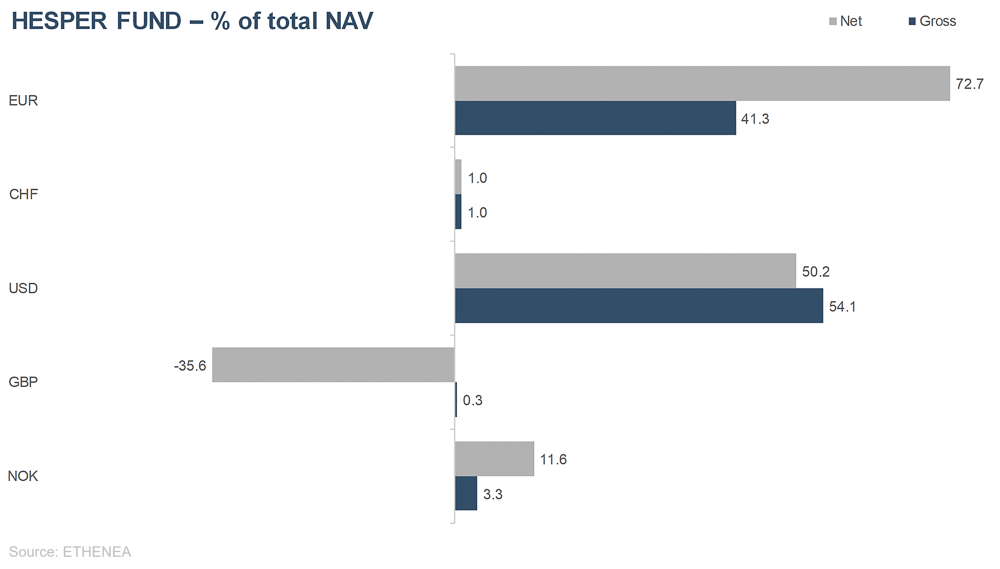

To hedge against this more challenging environment, the HESPER FUND reduced its overall equity exposure to 30%. Neutral duration exposure was cut further to become negative (almost -0.9 years). The fund continued to trade actively in the FX space, maintaining the dollar exposure at 50%. GBP short exposure was increased to -40% as we rebuilt long NOK bets (20%).

The breakdown of MTD (-1.13%) was +0.38% fixed income (-0.04% long positions, +0.42% short future positions), -1.60% equities, +0.03% commodities, +0.17% currencies and -0.13% fees and expenses. Decorrelation with traditional assets such as equities and bonds remained high.

Total assets fell to EUR 57 million at the end of the month. The unit class T-6 EUR unit class was 8.23% below its all-time high on 29 September 2022.

Volatility over the last 250 days ticked up to 6.1%, maintaining an attractive risk/return profile. The annualised return since inception has decreased to 3.26%.

Looking ahead to next month, the fund has continued to stay far away from its reference currency and to trade actively in the FX space. Currently, the currency exposure of the HESPER FUND – Global Solutions is as follows: USD 50%, NOK 20%, CHF 1% and GBP -40%.

As in the past, we will continue to monitor and calibrate the fund’s exposure to the various asset classes in line with market sentiment and changes in the macroeconomic baseline scenario.

*HESPER FUND - Global Solutions is currently only authorised for distribution in Germany, Luxembourg, Belgium, Italy, France, Austria and Switzerland.

Fund positioning

Grafik 13: Aktien-Exposure nach Regionen des HESPER FUND − Global Solutions

Grafik 14: Währungs-Allokation des HESPER FUND − Global Solutions

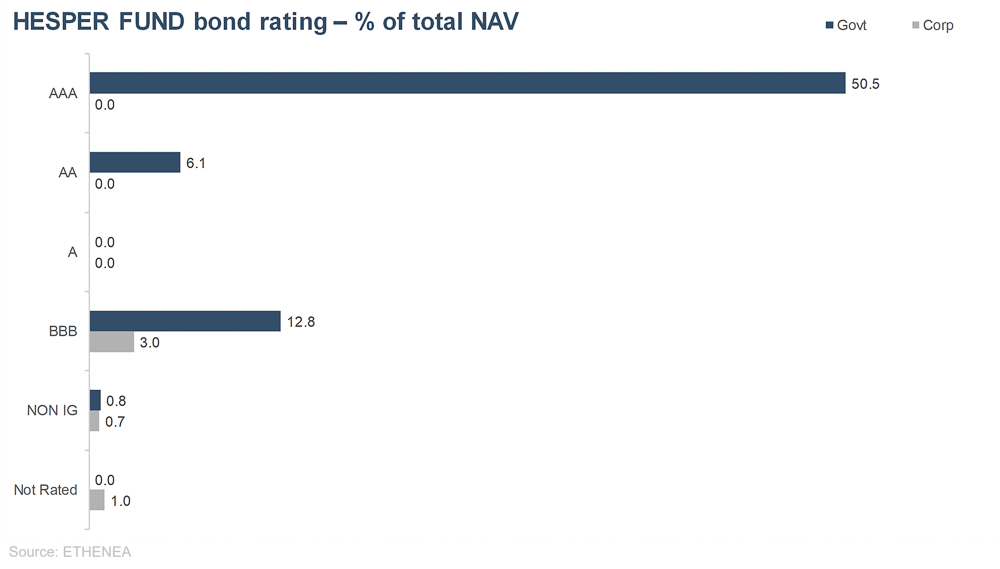

Grafik 15: Ratingstruktur der Anleihen des HESPER FUND − Global Solutions

The content of this page is intended for professional investors only.

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

This is a marketing communication. It is for product information purposes only and is not a mandatory statutory or regulatory document. The information contained in this document does not constitute a solicitation, offer or recommendation to buy or sell units in the fund or to engage in any other transaction. It is intended solely to provide the reader with an understanding of the key features of the fund, such as the investment process, and is not deemed, either in whole or in part, to be an investment recommendation. The information provided is not a substitute for the reader's own deliberations or for any other legal, tax or financial information and advice. Neither the investment company nor its employees or Directors can be held liable for losses incurred directly or indirectly through the use of the contents of this document or in any other connection with this document. The currently valid sales documents in German (sales prospectus, key information documents (PRIIPs-KIDs) and, in addition, the semi-annual and annual reports), which provide detailed information about the purchase of units in the fund and the associated opportunities and risks, form the sole legal basis for the purchase of units. The aforementioned sales documents in German (as well as in unofficial translations in other languages) can be found at www.ethenea.com and are available free of charge from the investment company ETHENEA Independent Investors S.A. and the custodian bank, as well as from the respective national paying or information agents and from the representative in Switzerland. The paying or information agents for the funds Ethna-AKTIV, Ethna-DEFENSIV and Ethna-DYNAMISCH are the following: Austria, Belgium, Germany, Liechtenstein, Luxembourg: DZ PRIVATBANK S.A., 4, rue Thomas Edison, L-1445 Strassen, Luxembourg; France: CACEIS Bank France, 1-3 place Valhubert, F-75013 Paris; Italy: State Street Bank International – Succursale Italia, Via Ferrante Aporti, 10, IT-20125 Milano; Société Génerale Securities Services, Via Benigno Crespi, 19/A - MAC 2, IT-20123 Milano; Banca Sella Holding S.p.A., Piazza Gaudenzio Sella 1, IT-13900 Biella; Allfunds Bank S.A.U – Succursale di Milano, Via Bocchetto 6, IT-20123 Milano; Spain: ALLFUNDS BANK, S.A., C/ Estafeta, 6 (la Moraleja), Edificio 3 – Complejo Plaza de la Fuente, ES-28109 Alcobendas (Madrid); Switzerland: Representative: IPConcept (Schweiz) AG, Münsterhof 12, Postfach, CH-8022 Zürich; Paying Agent: DZ PRIVATBANK (Schweiz) AG, Münsterhof 12, CH-8022 Zürich. The paying or information agents for HESPER FUND, SICAV - Global Solutions are the following: Austria, Belgium, France, Germany, Luxembourg: DZ PRIVATBANK S.A., 4, rue Thomas Edison, L-1445 Strassen, Luxembourg; Italy: Allfunds Bank S.A.U – Succursale di Milano, Via Bocchetto 6, IT-20123 Milano; Switzerland: Representative: IPConcept (Schweiz) AG, Münsterhof 12, Postfach, CH-8022 Zürich; Paying Agent: DZ PRIVATBANK (Schweiz) AG, Münsterhof 12, CH-8022 Zürich. The investment company may terminate existing distribution agreements with third parties or withdraw distribution licences for strategic or statutory reasons, subject to compliance with any deadlines. Investors can obtain information about their rights from the website www.ethenea.com and from the sales prospectus. The information is available in both German and English, as well as in other languages in individual cases. Producer: ETHENEA Independent Investors S.A.. Distribution of this document to persons domiciled in countries in which the fund is not authorised for distribution, or in which authorisation for distribution is required, is prohibited. Units may only be offered to persons in such countries if this offer is in accordance with the applicable legal provisions and it is ensured that the distribution and publication of this document, as well as an offer or sale of units, is not subject to any restrictions in the respective jurisdiction. In particular, the fund is not offered in the United States of America or to US persons (within the meaning of Rule 902 of Regulation S of the U.S. Securities Act of 1933, in its current version) or persons acting on their behalf, on their account or for the benefit of a US person. Past performance should not be taken as an indication or guarantee of future performance. Fluctuations in the value of the underlying financial instruments or their returns, as well as changes in interest rates and currency exchange rates, mean that the value of units in a fund, as well as the returns derived from them, may fall as well as rise and are not guaranteed. The valuations contained herein are based on a number of factors, including, but not limited to, current prices, estimates of the value of the underlying assets and market liquidity, as well as other assumptions and publicly available information. In principle, prices, values, and returns can both rise and fall, up to and including the total loss of the capital invested, and assumptions and information are subject to change without prior notice. The value of the invested capital or the price of fund units, as well as the resulting returns and distribution amounts, are subject to fluctuations or may cease altogether. Positive performance in the past is therefore no guarantee of positive performance in the future. In particular, the preservation of the invested capital cannot be guaranteed; there is therefore no warranty given that the value of the invested capital or the fund units held will correspond to the originally invested capital in the event of a sale or redemption. Investments in foreign currencies are subject to additional exchange rate fluctuations or currency risks, i.e. the performance of such investments also depends on the volatility of the foreign currency, which may have a negative impact on the value of the invested capital. Holdings and allocations are subject to change. The management and custodian fees, as well as all other costs charged to the fund in accordance with the contractual provisions, are included in the calculation. The performance calculation is based on the BVI (German federal association for investment and asset management) method, i.e. an issuing charge, transaction costs (such as order fees and brokerage fees), as well as custodian and other management fees are not included in the calculation. The investment performance would be lower if the issuing surcharge were taken into account. No guarantee can be given that the market forecasts will be achieved. Any discussion of risks in this publication should not be considered a disclosure of all risks or a conclusive handling of the risks mentioned. Explicit reference is made to the detailed risk descriptions in the sales prospectus. No guarantee can be given that the information is correct, complete or up to date. The content and information are subject to copyright protection. No guarantee can be given that the document complies with all statutory or regulatory requirements which countries other than Luxembourg have defined for it. Note: The most important technical terms can be found in the glossary at www.ethenea.com/glossary. Information for investors in Belgium: The prospectus, the key information documents (PRIIPs-KIDs), the annual reports and the semi-annual reports of the sub-fund are available in French free of charge upon request from the investment company ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxembourg and from the representative: DZ PRIVATBANK S.A., 4, rue Thomas Edison, L-1445 Strassen, Luxembourg. Information for investors in Switzerland: The country of origin of the collective investment scheme is Luxembourg. The representative in Switzerland is IPConcept (Schweiz) AG, Münsterhof 12, P.O. Box, CH-8022 Zurich. The paying agent in Switzerland is DZ PRIVATBANK (Schweiz) AG, Münsterhof 12, CH-8022 Zurich. The prospectus, the key information documents (PRIIPs-KIDs), and the Articles of Association, as well as the annual and semi-annual reports, can be obtained free of charge from the representative. Copyright © ETHENEA Independent Investors S.A. (2024) All rights reserved. 08/06/2021