Charting a course for a sustainable future

Over the past few years, the consideration of sustainability factors has become an integral part of investing. Investments have always been assessed in terms of earnings potential, risk and liquidity, and these days it is also a matter of course to assess them using ESG criteria. The fact that ESG stands for Environment, Social and Governance does not need to be spelled out in 2021. However, what does need to be explained is precisely how sustainability factors are considered.

There are plenty of conventional investment indicators for performance, risk (e.g. volatility, maximum drawdown) and liquidity, and these allow for the objective comparison of various investments options. Though this evaluation is mainly ex-post, even when used ex-ante it can give informed investors a very good idea of the expected results. Given the various interpretations of sustainability, this does not really apply to ESG criteria. First and foremost, the interpretation of sustainability factors has so far invariably reflected the product provider’s subjective point of view.

To establish more solid and objective criteria for assessing the sustainability of individual investment products, the European Union has enacted the Sustainable Finance Disclosure Regulation (SFDR), which comes into force on 10 March 2021. The prime objective of this EU Regulation is to provide the transparency and comparability that has been lacking to date. Even though the Regulation will not be fully implemented right from the start and further important ESG-relevant provisions will follow, such as the EU Taxonomy and amendments to the MiFID II Directive, it can without doubt be seen as agenda-setting for investment funds.

Initially, the most visible distinguishing feature for all funds will be the classification based on their ESG strategy, with all mutual funds having to decide on one of the following three product categories:

- Article 6 funds are normal funds that do not pursue any explicit sustainability strategy.

- Article 8 funds pursue a sustainability strategy. The companies in which they invest must follow good governance (G) practices and the fund must take environmental (E) and/or social (S) criteria into account in its investment process.

- Article 9 funds target sustainable investments often described as impact strategies. They must have a specific sustainability objective, such as reducing carbon emissions.

Regardless of the particular classification, in future all funds must make disclosures on whether and how sustainability risks are integrated in the investment decision-making process. In addition, regular reports on the main adverse sustainability impacts of the investment must be made by 30 December 2022 at the latest.

At ETHENEA, both the three Ethna funds and the HESPER FUND – Global Solutions are classified as Article 8 funds under the new Sustainable Finance Disclosure Regulation. This reaffirms our resolve to offer our clients responsible investment solutions with a competitive and sustainable return. ESG is and will remain a cornerstone. Furthermore, we thereby ensure that our funds can continue to serve as a core investment in our investors’ allocation.

The high degree of flexibility of the Ethna Funds has always been key to their success in adapting to changing markets and circumstances over time. The products are constantly evolving in order to move with the times while remaining timeless. Our investment funds’ sustainability strategy has also undergone continual development and refinement in recent years.

What started in 2013 with the first product-related exclusion criteria, such as tobacco, has developed over time into a fully-fledged three-stage investment process in order to give due weight to the matter of sustainability in the selection of portfolio securities.

In a first step, we reduce the universe available for investment by setting broad exclusions: when selecting securities, it is our policy not to consider companies whose core activity is the area of armaments, tobacco, pornography, food speculation and/or the mining/distribution of coal.

We also do not invest in a company if it has been found to be in serious breach of the principles of the UN Global Compact and there is no convincing plan in place to remedy the situation.

In the case of sovereign issuers, we exclude investments in countries that have been designated as ‘Not Free’ in the annual analysis carried out by Freedom House (www.freedomhouse.org). This list of exclusions was recently aligned with the joint proposal of the German Investment Funds Association (Fondsverband – BVI), the German Derivatives Association (Deutsche Derivate Verband – DDV) and the German Banking Industry Committee (Deutsche Kreditwirtschaft – DK), to ensure that it would meet the generally accepted criteria for sustainable products going forward.

On top of the aforementioned exclusions, which primarily relate to fixed standards and company products, the second step sees the exclusion of equity and bond issuers that do not meet the minimum threshold for our combined environmental, social and governance requirements. An ESG risk assessment is conducted to measure the extent to which the economic value of a company is put jeopardised by ESG factors or – in more technical terms – the magnitude of a company’s exposure to unmanaged ESG risks. This risk assessment can be done quickly and efficiently for a large investment universe by working with a specialised provider: Sustainalystics.

Lastly, an individual assessment of each issuer of a stock or bond forms an integral part of every investment decision. When deciding whether investments are suitable for our portfolios, we consider the individual ESG criteria in addition to traditional parameters for expected risk and earnings as well as liquidity. Thus, every issuer and every single security is individually assessed under the environmental, social and governance headings. In addition, any existing controversies are considered in the analysis. This enables us to increase the sustainability of our portfolios overall without having to compromise on the risk/return profile.

In the not-too-distant future, investment advisors will have to ask their clients by default whether ESG aspects are to be taken into consideration in their investment. At ETHENEA, we firmly believe that a true core product has to meet the higher sustainability standards of today’s investors. At the same time, earnings potential, risks and liquidity cannot be sidelined. With the entry into force of the Sustainable Finance Disclosure Regulation in March 2021, we have set the three Ethna Funds and the HESPER FUND – Global Solutions on course to strike a successful balance between these four elementary investment objectives.

Positioning of our funds

Ethna-DEFENSIV

It was the worst start of year for the global bond market since 2015. Yields on 10-year U.S. Treasuries briefly topped the 1.5% mark for the first time since the beginning of the pandemic, with yields at the long end rising the most and the yield curve steepening sharply. The U.S. pressure to sell also spread to Europe, with yields on UK, French, German and Italian sovereign bonds rising. German Bunds yielded around -0.25% for a short time, compared to a yield of -0.55% at the beginning of the year.

The fall in price is the latest manifestation of a broad exodus from sovereign bonds regarded as safe, driven by the roll-out of Covid-19 vaccines and a rapid economic recovery. At the same time, for the first time in decades, concerns about a serious rise in inflation are mounting. That said, we are of the opinion that the economy has a long road to recovery ahead of it and the first signs of rising prices will not necessarily lead to persistently high inflation. As we wrote in last month’s Market Commentary, we believe that price rises are largely due to short-term effects, such as rising oil prices and semiconductor supply shortages. The unemployment rate remains high and the labour market is a long way off full employment, so unit labour costs are likely to remain under pressure. At the same time, central banks on both sides of the Atlantic have made it clear that monetary policy will remain supportive for the foreseeable future and that, should it come to that, they will intervene if yields rise further.

However, this barely seems to have calmed investors at all for now. Corporate bonds followed the downward trend in sovereign bonds, and the risk premia scarcely changed at all on average. While less interest-rate-sensitive high yield bonds as well as cyclical sectors such as banks and commodities producers did comparatively well, the performance of other investment grade bonds slipped. The broad Bloomberg Barclays Index for investment grade bonds in Europe lost around 0.90% since the beginning of the year, with February alone accounting for around 0.78% of that. Investment grade bonds denominated in USD actually lost 4.12% since the beginning of the year. Note that the average corporate bond denominated in USD has a duration of almost 9, while the bonds denominated in USD in the Ethna-DEFENSIV have a duration of less than 5 and, accordingly, lost less. The pressure in the bond market to sell spread to the equity market to some extent. However, both markets stabilised again towards the end of the month.

We reduced the duration within the bond portfolio of the Ethna-DEFENSIV (T class) early (back at the beginning of February), which enabled us to limit the price losses on the bond side. However, we sold the U.S. Treasury futures we had been using as a hedge against the interest rate rise too early. As a result, the fund was not completely unaffected by the global rises in yields: the bonds denominated in USD in the Ethna-DEFENSIV lost around 0.70% last month while bonds denominated in EUR remained largely stable and closed the month with a performance of plus/minus zero. With sustainability in mind, we also switched our equity exposure into sustainable equity ETFs. The fund’s sustainable net equity allocation is currently around 3%. On balance, while the Ethna-DEFENSIV put in a solid performance considering the quite significant and greater-than-expected rises in yield, as well as the losses on the U.S. equity markets, it still posted a negative YTD performance of -0.75%. In this turbulence caused by the interest rate changes, all asset classes were down at the same time, and equities/currencies were unable to compensate in our bond-focused portfolio. However, we are optimistic looking ahead. There were signs of a turnaround in U.S. yields in the last few trading days in February and it seems to be continuing in March.

Ethna-AKTIV

The accelerating steepening of yield curves both in Europe and in the U.S. again interrupted the equity market rally that has been under way for a good year now. In particular, technology securities, which are regarded as highly interest-rate-sensitive due to their high expected growth being discounted, made losses from mid-February onwards. The picture is not quite so dramatic, though, on closer examination. For example, the rate for 10-year U.S. Treasuries increased over the month from 1.04% to more than 1.6%, closing most recently, however, at 1.4%. While this is a historically fast rise, it has not even regained its pre-crisis level in absolute terms. While the rise in interest rates can actually be regarded as a positive sign for economic development, in this instance it was the speed of the rise that led to volatility, originally in the bond market and spreading to the market as a whole. However, this too must be put into perspective. Despite the equity market losses suffered during the month, most indices still closed inside positive territory for the month. In fact, many capital investors are still running a positive performance for 2021, which is why no panic selling is to be expected at the moment.

Even though we still stand by our forecasts with regard to a growth surprise and higher equity prices during the year, we took advantage of the strong performance in the first two weeks to take some of the accrued profits for tactical reasons. While the indices for the Japanese market and emerging markets were sold just before the correction, the position in European banks futures, which we had also closed out, also climbed almost unwaveringly. We also took profits early on the duration management, which was designed for rising interest rates. We did not expect that movement in interest rates would accelerate to such an extent towards the end of the month. Since we expect volatility in equity markets to last for a while yet, we reduced the net equity allocation (including funds) to 26.6% towards the end of the month. We want to see a calming of the interest rate market as well as a stabilisation of equity prices before we raise the equity allocation back up to the maximum level based on fundamentals. The currency positions contained in the fund for balancing purposes detracted from performance this month. Obviously, the demand for safe-haven currencies was not sustainable in the context of this correction. In principle, this can be regarded as a positive sign going forward. Given that we reduced equity risk, we also reduced the currency position to 20%. Thanks to the measures we carried out, we are in the comfortable position of being able to observe the current price fluctuations from the sidelines to some extent. As soon as the reflation trade – which we believe is absolutely still valid – picks up again, we will increase our risk allocation in the fund again.

All in all, the Ethna-AKTIV got through the first two months of the year with relatively low volatility and was rewarded with a YTD performance of more than 1% for consistently adhering to the fundamental assessment but also taking tactical management measures.

Ethna-DYNAMISCH

Global equity markets were unsettled in the shortest month of the year. The beginning of February saw a record weekly inflow (of almost USD 60 billion) into global equity funds, which for one can be seen as a manifestation of worldwide progress in the fight against the pandemic and of the prospect of economic recovery. Underpinned by this liquidity and coupled with a strong reporting season, equity markets reached new all-time highs. After a temporary consolidation around mid-month, the sharply rising yields on long-dated (U.S.) Treasuries ultimately brought about a market correction in the second half of the month.

Inflation expectations continue to increase, manifesting in higher yields and increasing the risk of a departure from the ultra-accommodative monetary policy, which has been a major driver for equity markets since the 2007/2008 financial crisis. At the same time, the central banks are unrelenting in their desire to maintain current monetary policy. The U.S. central bank, the Fed, has expressed that it is prepared to live with a potential inflation overshoot without coming under pressure to hike interest rates. Thus the recent rise in yields, while comparatively steep in a short length of time, remains structurally low. Since national debt levels, which have already taken on new dimensions due to the pandemic, could quickly become unsustainable at high interest rates levels – especially in Japan and the eurozone (Italy) – we consider a substantial rise very unlikely. Central banks have also demonstrated many times over that they do not wish to go down that road.

In that respect, we regard the interest-driven correction as a purging of the market because it mainly affected those market segments that, as mentioned in last month’s Market Commentary, had overheated. We do not see any risk to boarder market valuations in the medium term. On the contrary, the other structural equity market drivers – fiscal support, accelerated economic growth and base effects – are still intact.

In this environment, we retained our equity allocation of around 75%. On the one hand, we closed positions that no longer met our original investment case. Cisco Systems is one example of this. We are no longer convinced that more attractive areas of the company’s business (e.g. Cybersecurity) can overcome the headwind in the network solutions segment. On the other hand, we built up new positions in structural quality companies. These include Dynatrace, a leading provider of monitoring solutions in cloud environments. Dynatrace is benefiting from the acceleration of digitisation in companies and the complexity of hybrid and/or multi-cloud architectures that goes with it. We assume that the company, which is profitable thanks partly to its penetration of related market segments (e.g. Cybersecurity), can maintain its annual turnover growth rate in the region of plus/minus 20%. In addition, we participated in the AUTO1 IPO in February with a small allocation. Its sales platforms (Wirkaufendeinauto.de, AUTO1.com and Autohero) make the German AUTO1 Group a digital disruptor in the European used car market. Since online penetration is still in its infancy and AUTO1 already has an established competitive position, we expect the company to benefit disproportionately more from a maturing market.

We will continue to focus on such quality companies into the future, paying attention to the balance of attractive growth and appealing valuation to avoid biased positionings; for example, towards value or growth stocks. Thus, the Ethna-DYNAMISCH remains well positioned in the current stock market environment.

HESPER FUND - Global Solutions (*)

In February, expectations of a quick post-pandemic recovery caused a worldwide surge in long-term yields. The Treasury selloff quickly moved US yields from 1.15% to 1.6% and then back to 1.4 %, while in the United Kingdom and the eurozone, sovereign bond yields jumped even further. The long-end of the German yield curve has also moved into positive territory. Despite assurances from both Christine Lagarde and Jerome Powell that the central banks are monitoring the situation closely, at times we saw recovery expectations mixed with fears and angst about inflation. Investors in mortgage-backed securities who are protecting long duration portfolios may have exacerbated the rate move. Although the reflation trade continued, higher yields started to hurt equity markets, which are currently experiencing higher valuations, and triggered an increase in volatility.

Despite a good quarterly earnings showing, equity markets were choppy. Although US equities set an all-time high on 12 February, they ended the month on a weak note. The equity market rotation continued to penalise technology stocks; however, the move was not as pronounced as at the end of 2020. For the month, the S&P500 posted a 2.6% gain, the Nasdaq 100 dropped slightly by 0.1%, the Nasdaq Composite edged up 0.9% and the Russell 2000 rose by 6.1%.

As we have mentioned previously, our base scenario for 2021 remains that of a cyclical recovery underpinned by vaccine rollouts and policy support. However, this recovery is still facing a number of hurdles and will be uneven across regions and sectors, due to a still high number of infections and the slow roll-out of vaccines around the world. As such, economic activity in 2021 will continue to be significantly affected by the development of the pandemic.

In light of the still uncertain economic recovery, coupled with the aforementioned delays in the roll-out of the vaccination campaigns, market valuations are quite high. After a strong start to the year, equity markets are balancing rising optimism fuelled by the Covid-19 vaccines and further US fiscal stimulus against rising yields across the board, stretched valuations, and the slower than expected roll-out of the vaccines. To maintain its current valuations, the market needs good economic data and an improvement on the pandemic front. At the same time, a rapid rise in inflation expectations, along with the corresponding swift increase in sovereign bond yields, expose the equity market to potential short-term corrections.

As convexity hedging began to haunt markets already reeling from the bond rout, the HESPER FUND – Global Solutions reduced its equity exposure, as many stop loss limits were triggered. We reduced duration markedly, shorting Treasuries and divesting ourselves of long investment grade bonds. The overall equity exposure fell to 28% but was soon partially rebuilt to 40%. We sold our gold position completely and continued to back reflation, holding a very diversified range of equity indices, commodities, and high yield corporate bonds. Although we remain confident regarding the economic fundamentals that underpin the long-term appreciation of the Swiss franc, we have reduced our exposure to zero, as the currency does not fit with the reflation trade in the short term. On the currency front, we still hold a 20% USD exposure, as we believe that the currency’s weakening cycle may be nearing its end. Moreover, we built up an opportunistic position of 4% in the Russian rouble, given the fact that, for political reasons, this emerging currency is lagging, despite the sharp increase in commodity prices.

As we have seen many times, higher yields may have significant knock-on effect on equities, credit and more, particularly when the rise in yields is sudden and rapid. Nevertheless, given the still very early phase of the economic cycle and the considerable uncertainties about the future of the pandemic, we believe authorities will remain very cautious on the timing of any policy tightening and will be careful to avoid any policy mistakes. Therefore, we expect to continue to ride the risk-on waves throughout the year in a cautious manner while continuously looking for the appropriate hedges to reduce any potential drawdown in the portfolio.

In February, the HESPER FUND - Global Solutions EUR T-6 shares rose 0.61%, putting it at +1.46 ytd.

*The HESPER FUND – Global Solutions is currently only authorised for distribution in Germany, Luxembourg, France, and Switzerland.

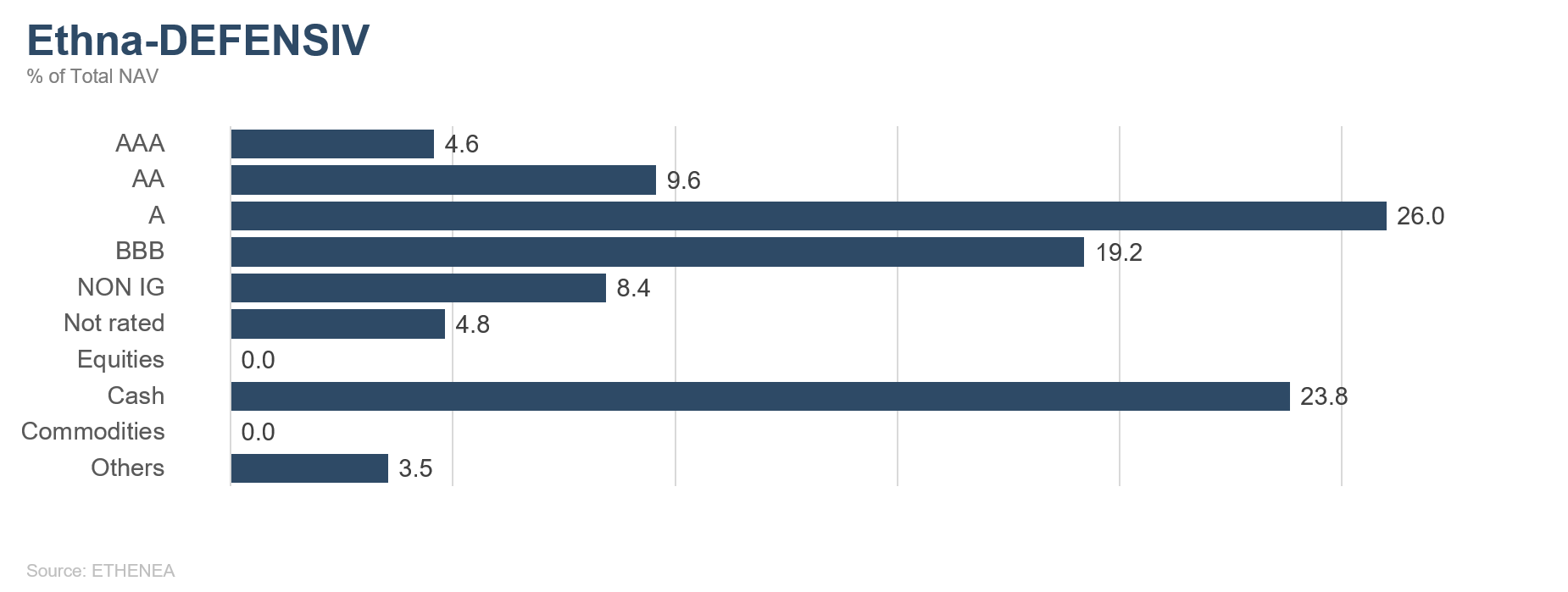

Figure 1: Portfolio structure* of the Ethna-DEFENSIV

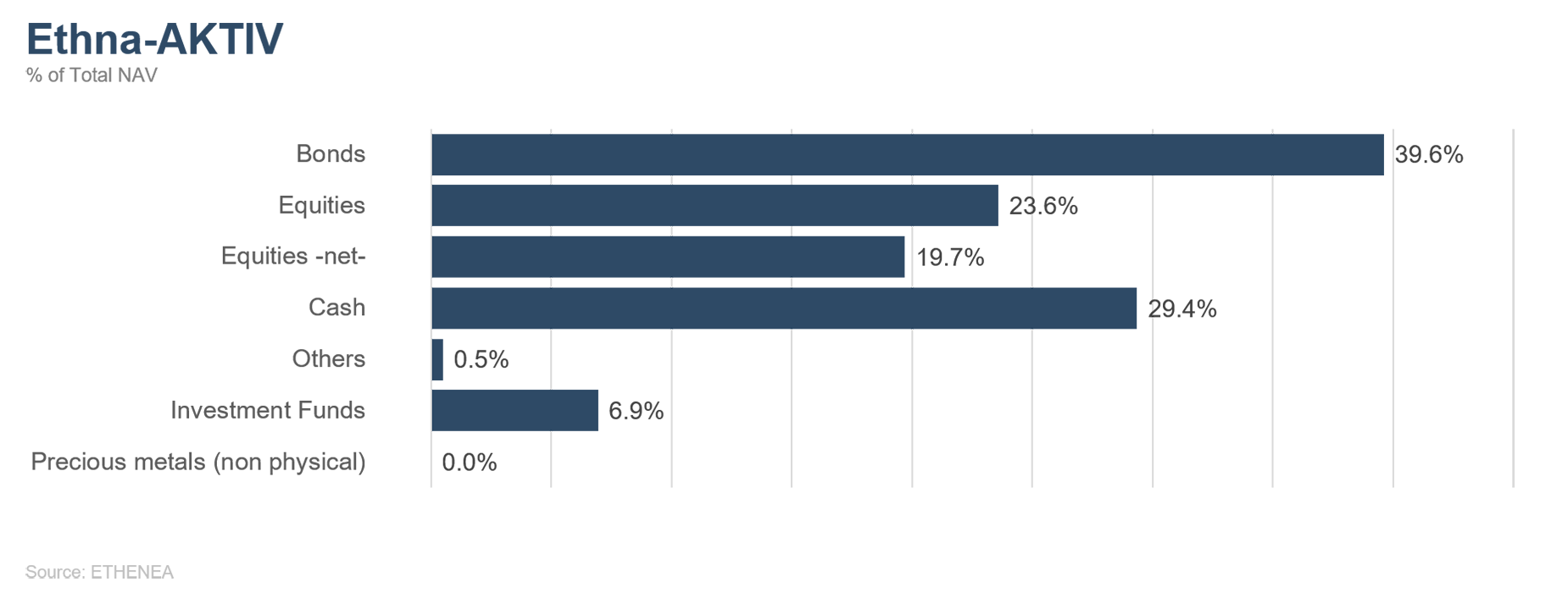

Figure 2: Portfolio structure* of the Ethna-AKTIV

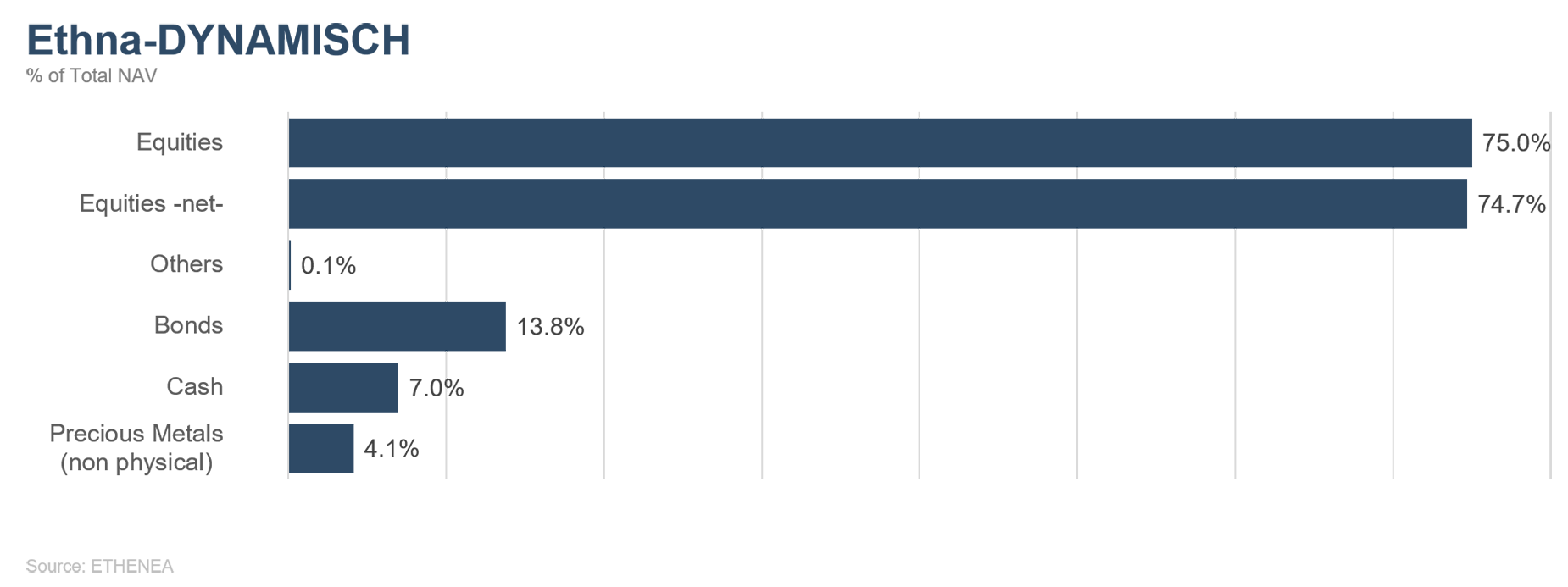

Figure 3: Portfolio structure* of the Ethna-DYNAMISCH

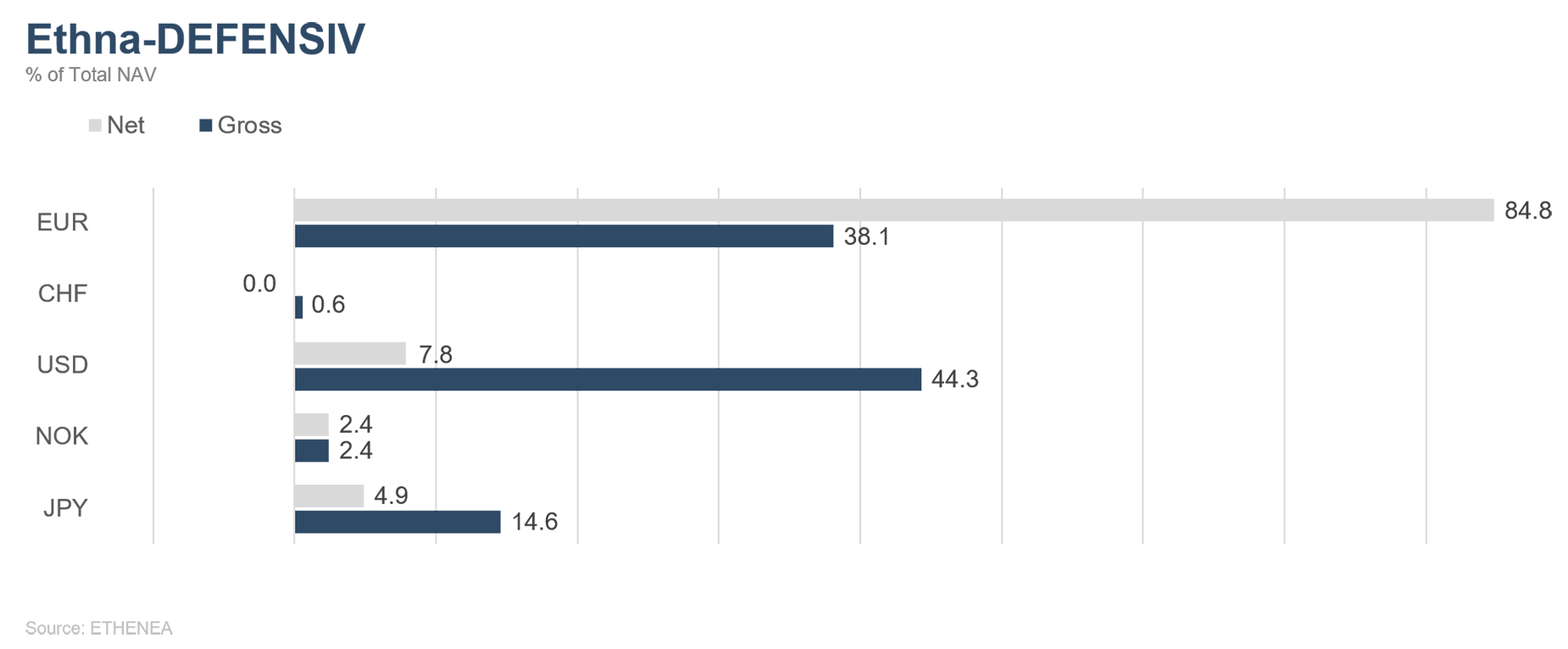

Figure 4: Portfolio composition of the Ethna-DEFENSIV by currency

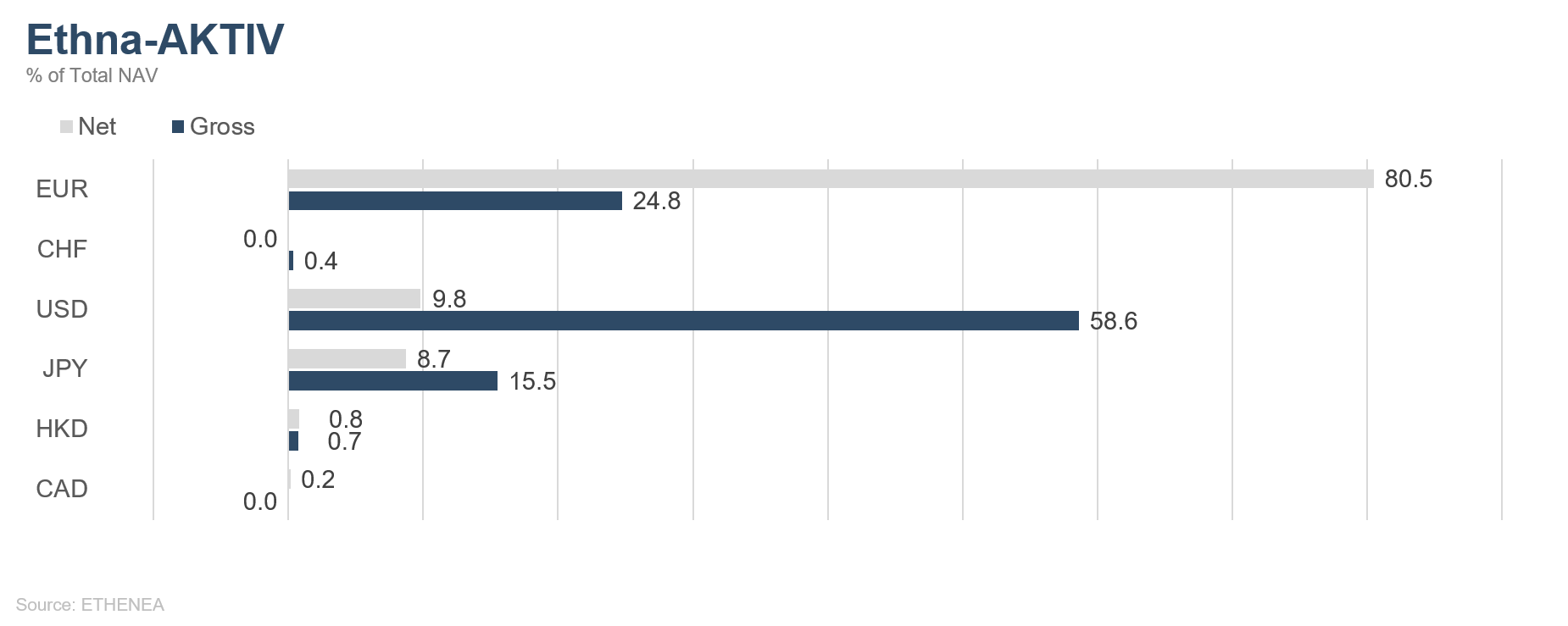

Figure 5: Portfolio composition of the Ethna-AKTIV by currency

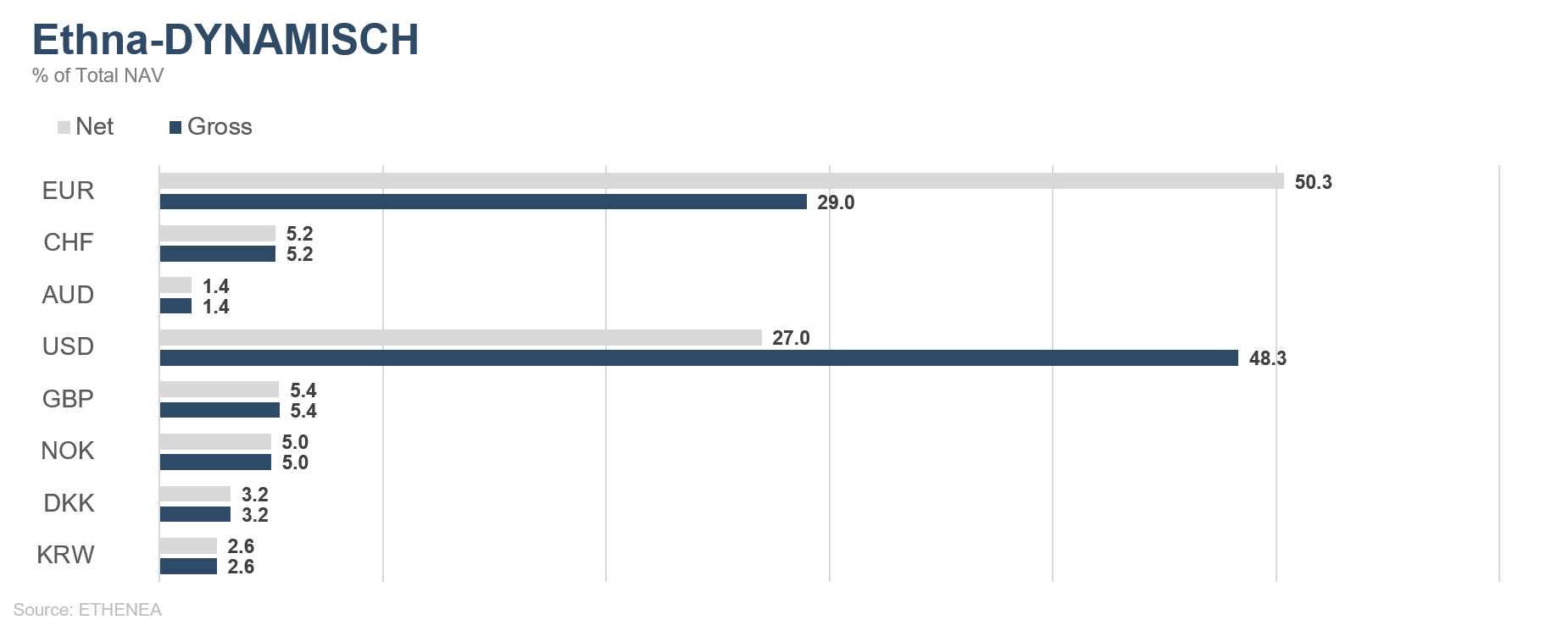

Figure 6: Portfolio composition of the Ethna-DYNAMISCH by currency

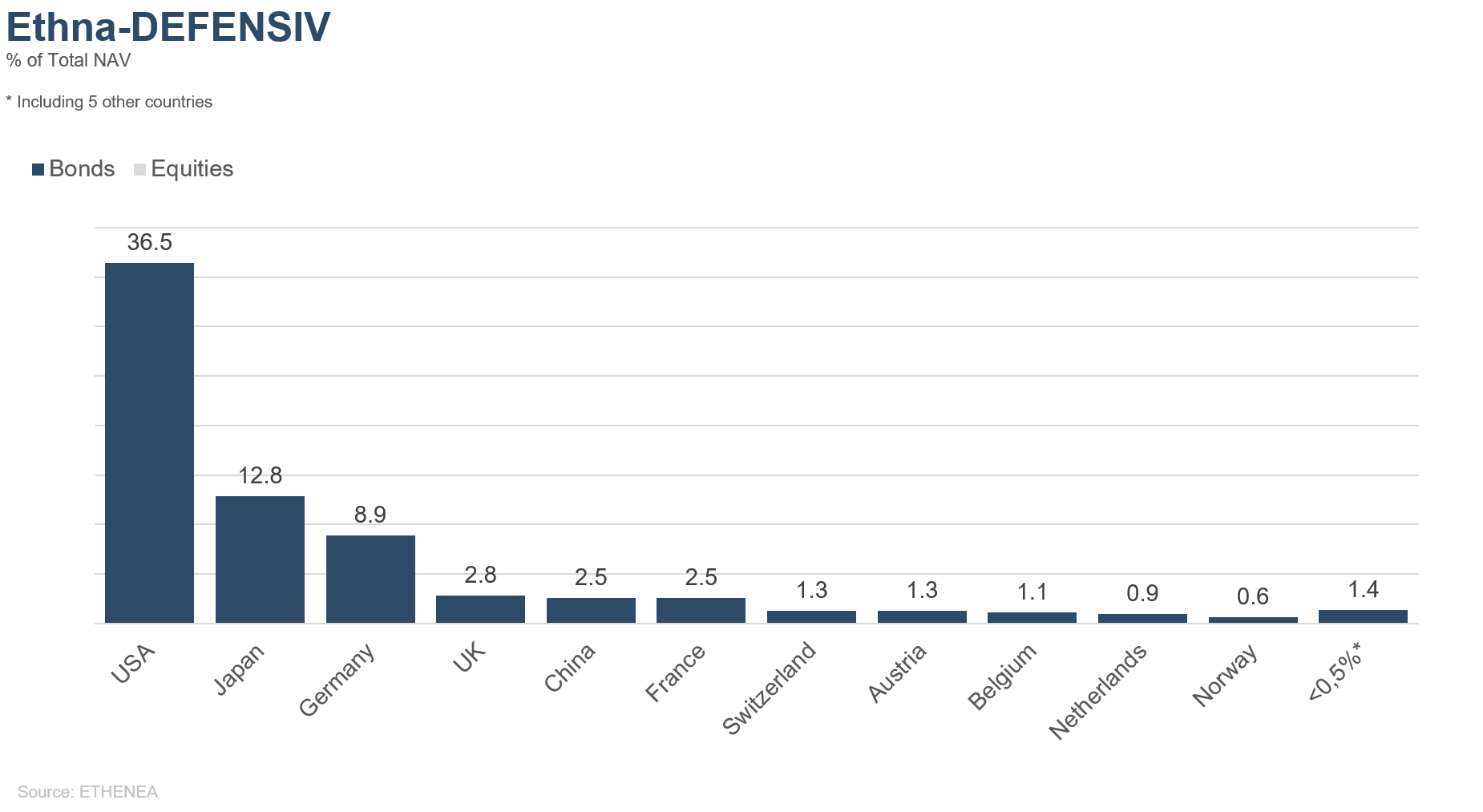

Figure 7: Portfolio composition of the Ethna-DEFENSIV by country

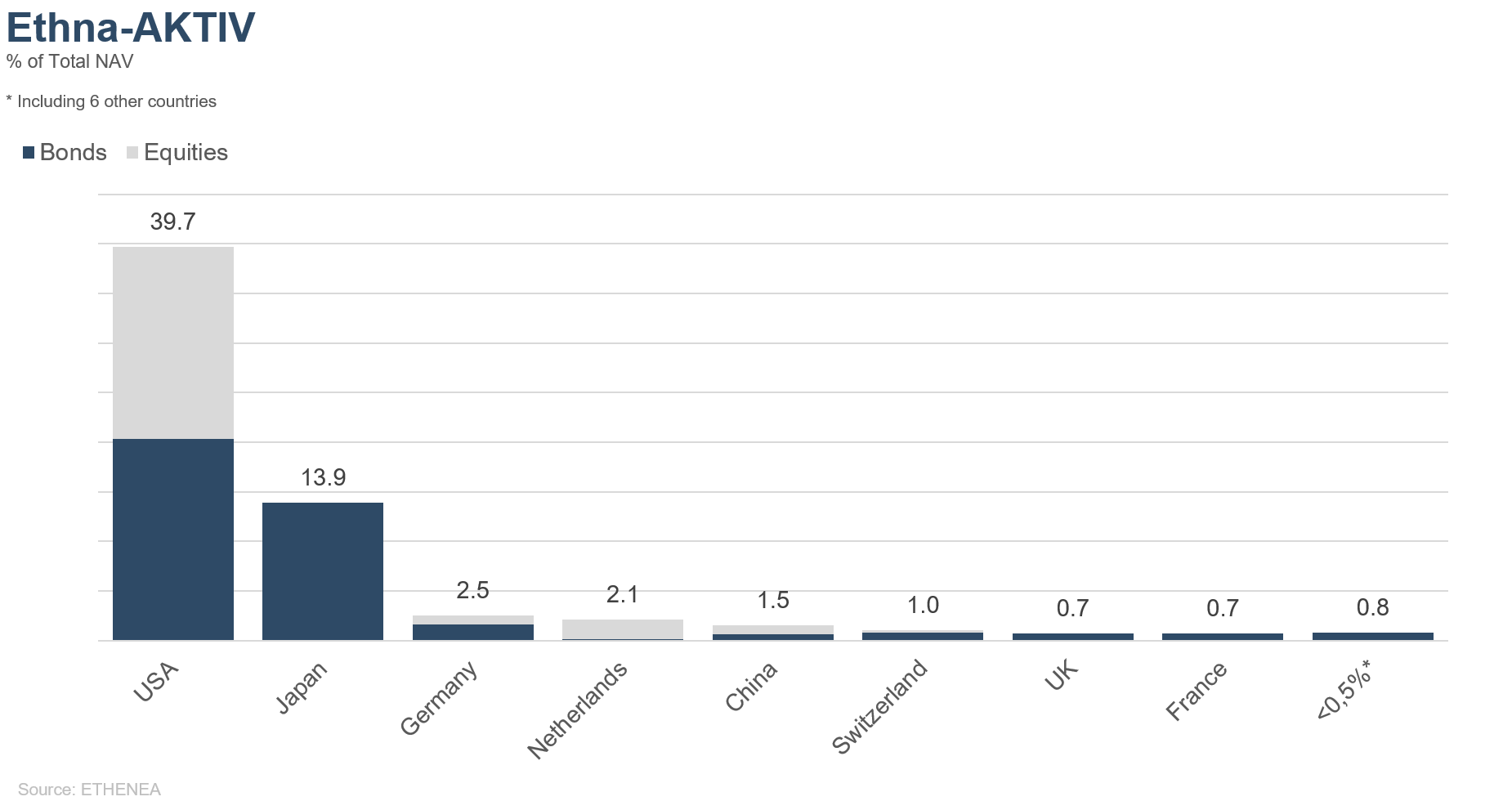

Figure 8: Portfolio composition of the Ethna-AKTIV by country

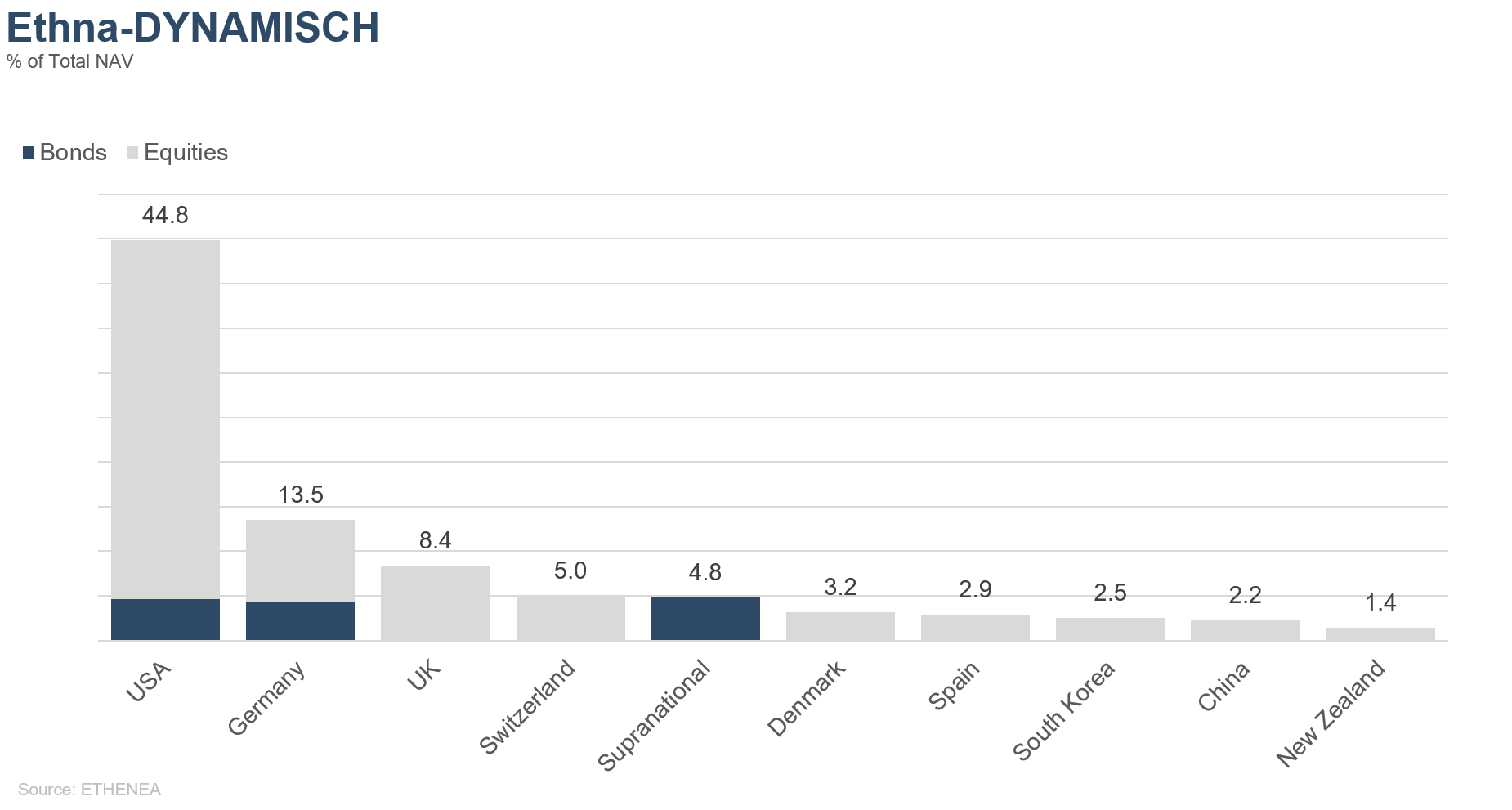

Figure 9: Portfolio composition of the Ethna-DYNAMISCH by country

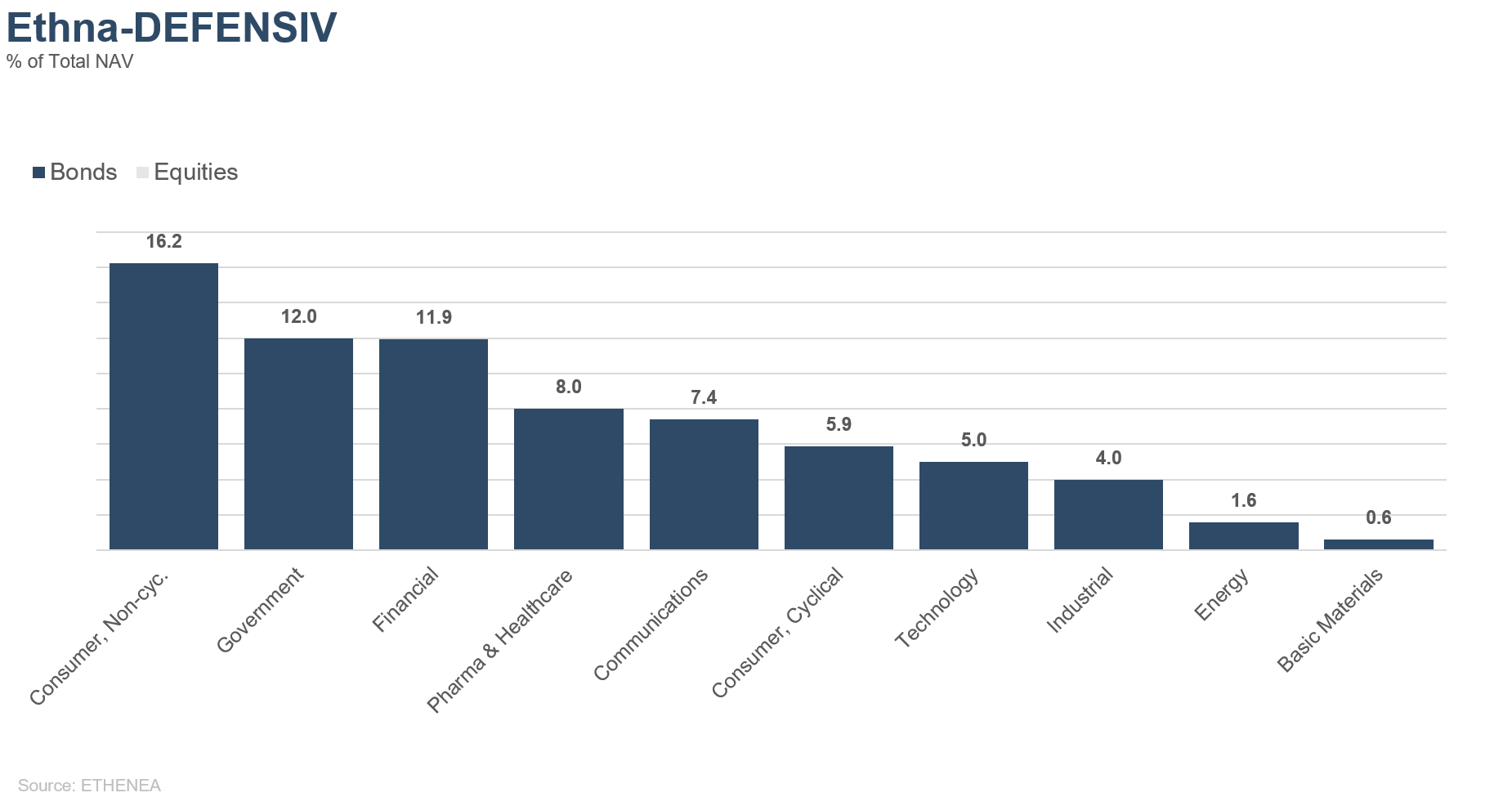

Figure 10: Portfolio composition of the Ethna-DEFENSIV by issuer sector

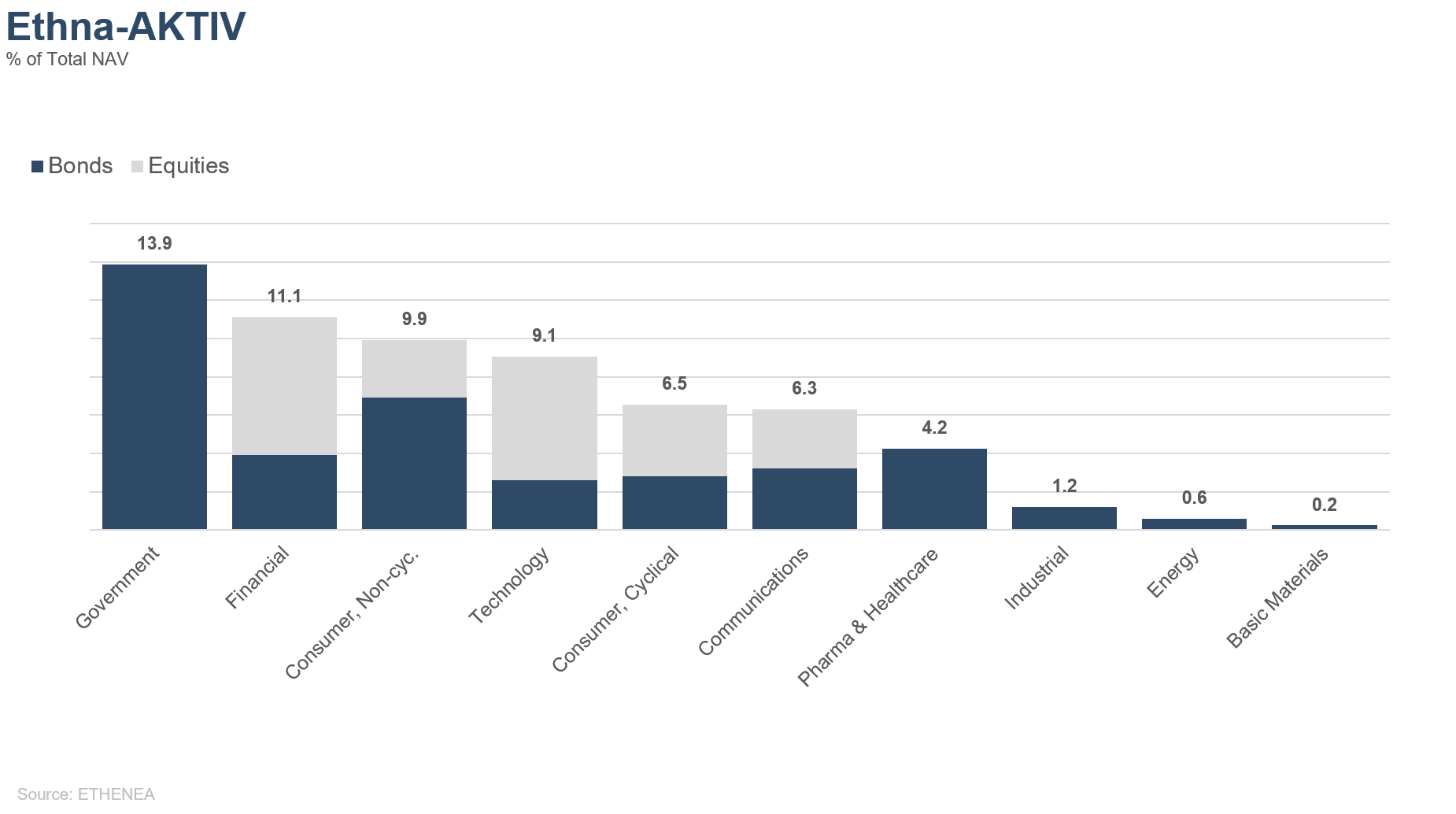

Figure 11: Portfolio composition of the Ethna-AKTIV by issuer sector

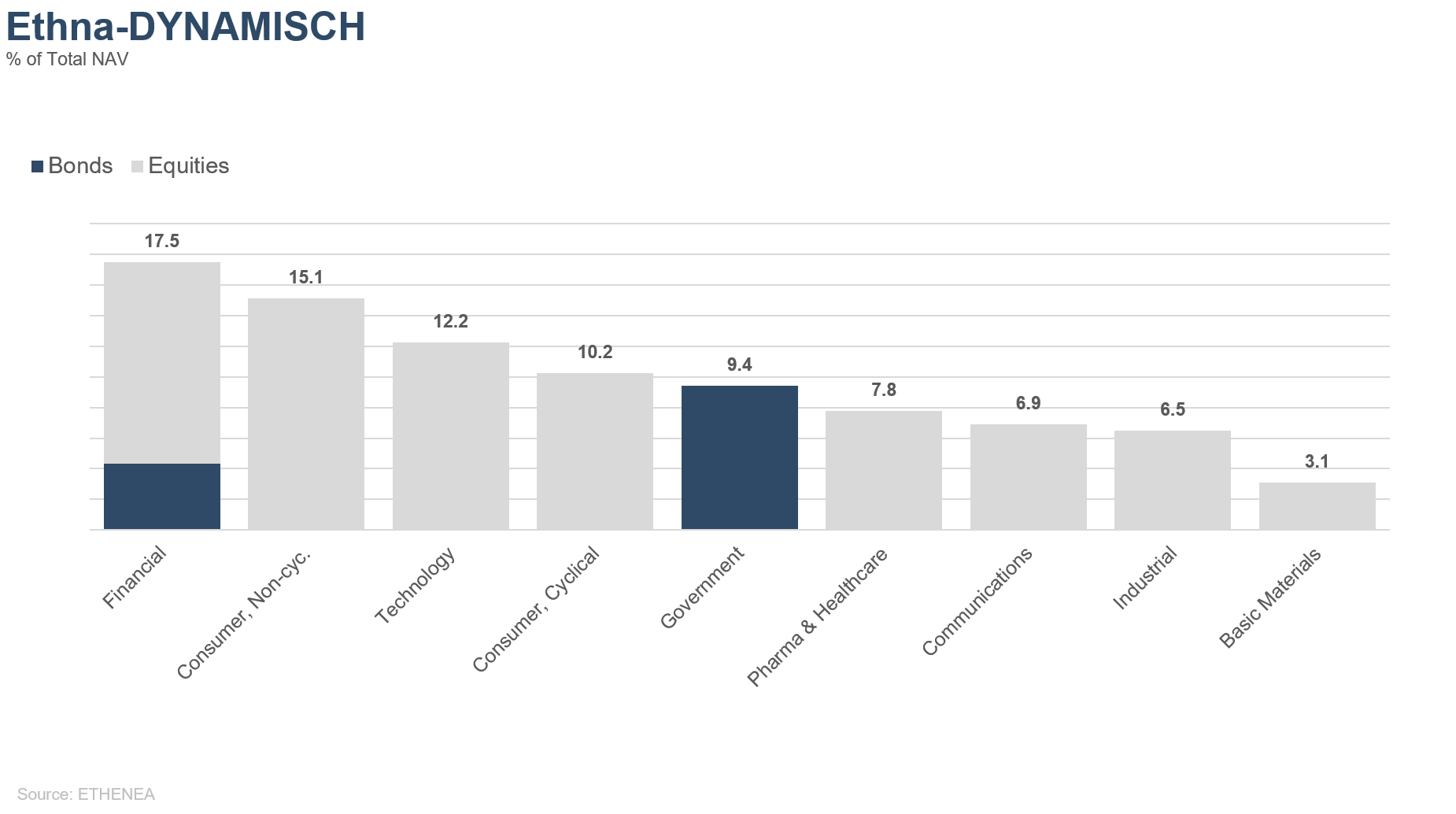

Figure 12: Portfolio composition of the Ethna-DYNAMISCH by issuer sector

* “Cash” comprises term deposits, call money and current accounts/other accounts. “Equities net” comprises direct investments and exposure resulting from equity derivatives.

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

This marketing communication is for information purposes only. It may not be passed on to persons in countries where the fund is not authorized for distribution, in particular in the USA or to US persons. The information does not constitute an offer or solicitation to buy or sell securities or financial instruments and does not replace investor- and product-related advice. It does not take into account the individual investment objectives, financial situation, or particular needs of the recipient. Before making an investment decision, the valid sales documents (prospectus, key information documents/PRIIPs-KIDs, semi-annual and annual reports) must be read carefully. These documents are available in German and as non-official translations from ETHENEA Independent Investors S.A., the custodian, the national paying or information agents, and at www.ethenea.com. The most important technical terms can be found in the glossary at www.ethenea.com/glossary/. Detailed information on opportunities and risks relating to our products can be found in the currently valid prospectus. Past performance is not a reliable indicator of future performance. Prices, values, and returns may rise or fall and can lead to a total loss of the capital invested. Investments in foreign currencies are subject to additional currency risks. No binding commitments or guarantees for future results can be derived from the information provided. Assumptions and content may change without prior notice. The composition of the portfolio may change at any time. This document does not constitute a complete risk disclosure. The distribution of the product may result in remuneration to the management company, affiliated companies, or distribution partners. The information on remuneration and costs in the current prospectus is decisive. A list of national paying and information agents, a summary of investor rights, and information on the risks of incorrect net asset value calculation can be found at www.ethenea.com/legal-notices/. In the event of an incorrect NAV calculation, compensation will be provided in accordance with CSSF Circular 24/856; for shares subscribed through financial intermediaries, compensation may be limited. Information for investors in Switzerland: The home country of the collective investment scheme is Luxembourg. The representative in Switzerland is IPConcept (Suisse) AG, Bellerivestrasse 36, CH-8008 Zurich. The paying agent in Switzerland is DZ PRIVATBANK (Suisse) AG, Bellerivestrasse 36, CH-8008 Zurich. Prospectus, key information documents (PRIIPs-KIDs), articles of association, and the annual and semi-annual reports can be obtained free of charge from the representative. Information for investors in Belgium: The prospectus, key information documents (PRIIPs-KIDs), annual reports, and semi-annual reports of the sub-fund are available free of charge in German upon request from ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxembourg, and from the representative: DZ PRIVATBANK AG, Niederlassung Luxemburg, 4, rue Thomas Edison, L-1445 Strassen, Luxembourg. Despite the greatest care, no guarantee is given for the accuracy, completeness, or timeliness of the information. Only the original German documents are legally binding; translations are for information purposes only. The use of digital advertising formats is at your own risk; the management company assumes no liability for technical malfunctions or data protection breaches by external information providers. The use is only permitted in countries where this is legally allowed. All content is protected by copyright. Any reproduction, distribution, or publication, in whole or in part, is only permitted with the prior written consent of the management company. Copyright © ETHENEA Independent Investors S.A. (2026). All rights reserved. 02/03/2021