Central banks concerned about persistent inflation and modest growth

Ethna-DEFENSIV

Key points at a glance

- Yields are near the peak of the current hiking cycle

- Fund delivers positive performance despite rising yields

- Short positions in futures on German and U.S. sovereign bonds reduced to 10%

- Distribution: back to paying out more than the minimum

- Cautious increase in portfolio duration a possibility in the foreseeable future

30 April 2024 – In April, the rising trend in yields along the entire length of the yield curve continued from previous months. Ever since yields on 10-year sovereign bonds fell to 1.9% in Germany and to 3.8% in the U.S. at the end of 2023, they have been climbing continually. Inflation figures in the U.S. did not come down as investors had expected. April saw the PCE price gauge come in at 2.7% for March, an increase over February’s figure of 2.5%. Of course, this is the wrong direction for the Fed, leading U.S. central bankers to adopt a much more hawkish tone. They even cast doubt on the possibility of interest rate cuts in the U.S. before the end of the year. This was a contributing factor in yields rising to year-to-date highs both in the U.S. and Germany. In our view, these highs are very close to the peak of this cycle.

The next decisions taken by both the Fed and the ECB will concern interest rate cuts. In Europe, the ECB signalled relatively clearly that the first interest rate cut will take place in June. Something extraordinary would have to happen for the members of the ECB to change their minds. In the U.S., the situation is a bit trickier due to persistent inflation. But we are of the opinion that the Fed will effect at least one rate cut before the end of 2024. Against this backdrop, and to take profits (the fund has delivered a positive performance despite rising yields), we gradually reduced our short positions in futures on German and U.S. sovereign bonds from 20% to 10% over the course of the month. Furthermore, fund distribution took place in April, with the fund back to paying out more than the minimum again (1.5%): approx. 2.32% in the A class. Other Ethna-DEFENSIV parameters remained relatively unchanged over the course of the month: we remain conservatively invested in high-quality short-dated corporate bonds denominated in euro.

We can envisage cautiously increasing the portfolio duration in the near future. As already mentioned, yields are nearing a plateau, and the next logical step would be a shift into the longer end of the yield curve so as to benefit from falling yields along with the central banks’ rate cuts. Where (on what markets), when and to what extent we increase duration will depend entirely on the current assessment of the market. At the moment, bonds with maturities after 2030 make up only a small portion of the portfolio, but it is getting nearer the time to increase portfolio duration.

Fund positioning

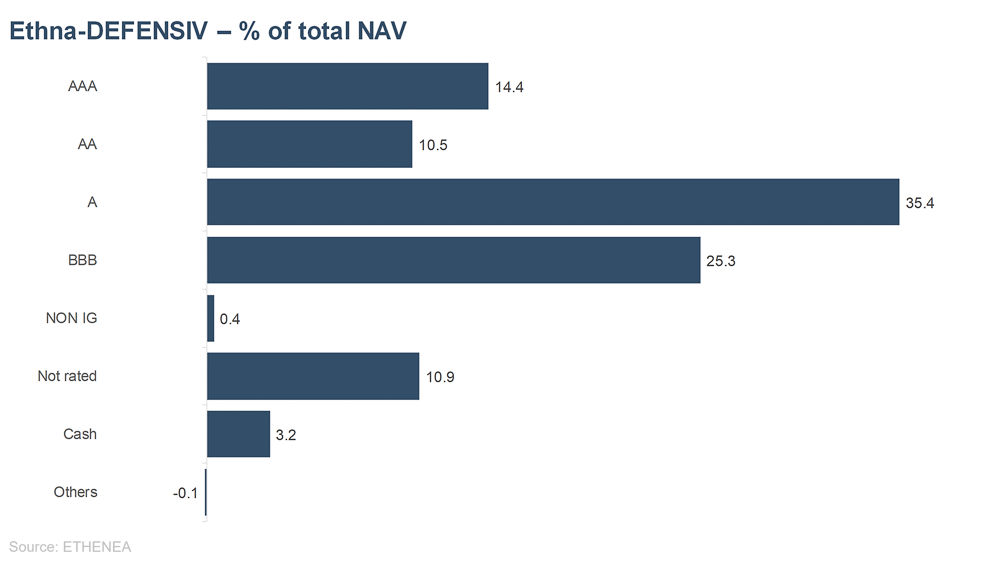

Figure 1: Portfolio structure* of the Ethna-DEFENSIV

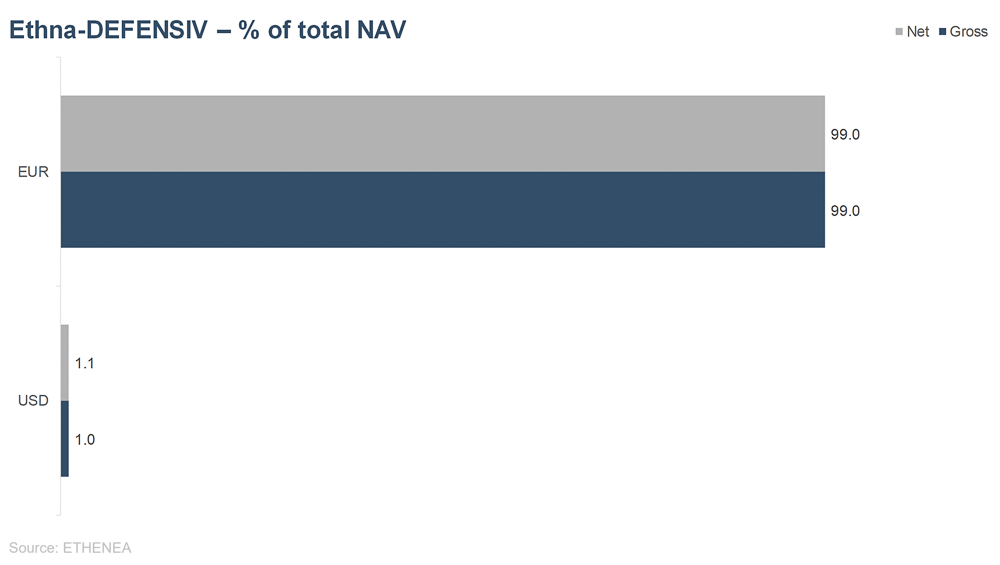

Figure 2: Portfolio composition of the Ethna-DEFENSIV by currency

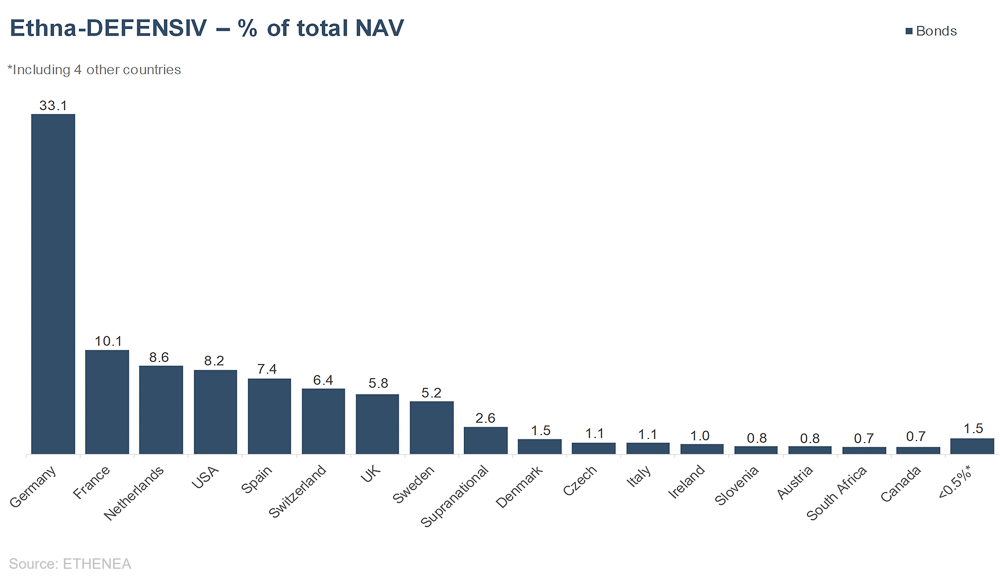

Figure 3: Portfolio composition of the Ethna-DEFENSIV by country

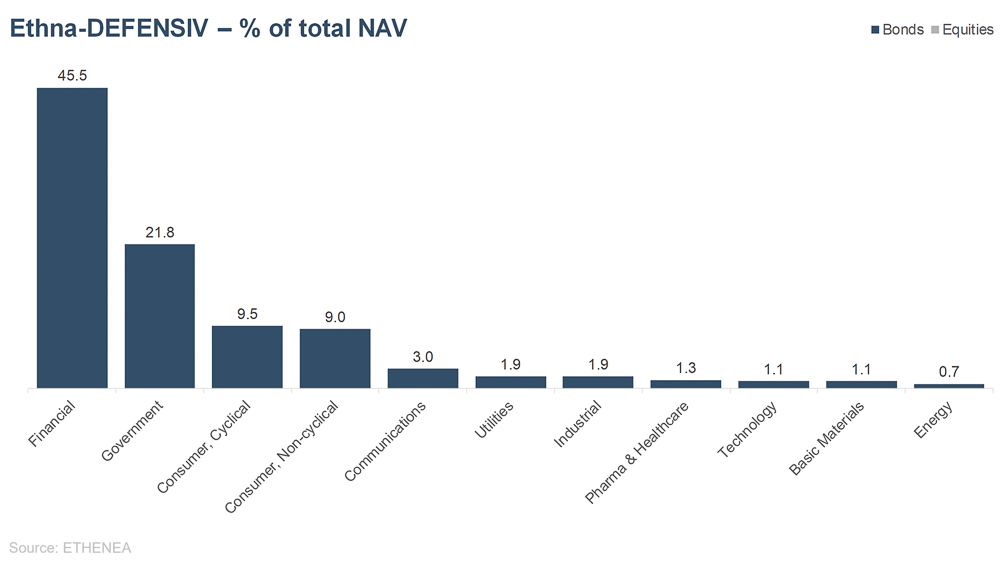

Figure 4: Portfolio composition of the Ethna-DEFENSIV by issuer sector

Ethna-AKTIV

Key points at a glance

- Portfolio remains geared towards an environment of moderate growth, falling but stubborn inflation and a rising stock market trend.

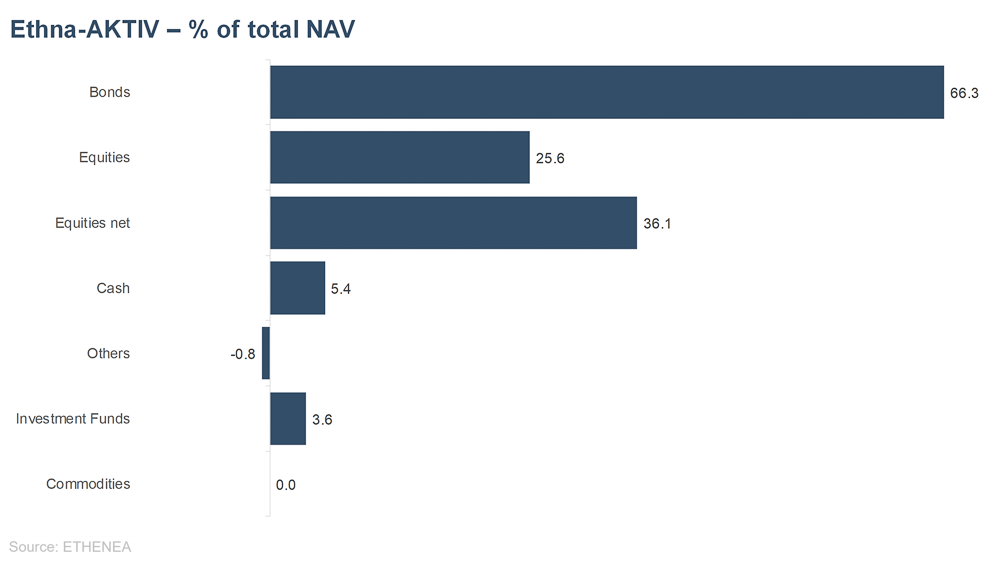

- At 35%, the equity component is in neutral territory, and is exclusively invested in US large caps

- High quality and short maturities continue to characterise the bond portfolio. Modified duration is 1.2.

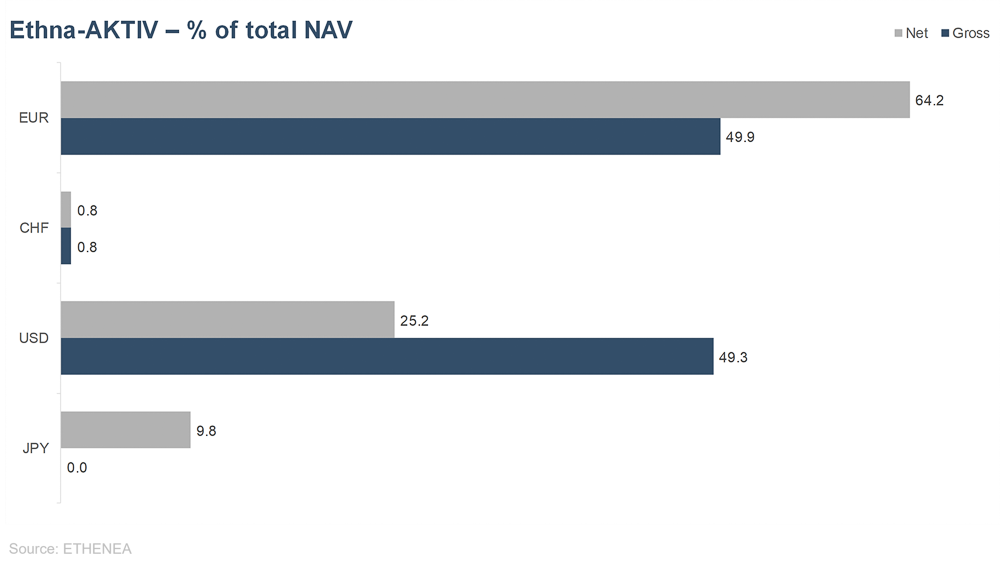

- 15% position in the Japanese yen reduced to 10%; portfolio still has USD exposure of 25%.

30 April 2024 – The month of April held an array of fundamental, macro-economic and, last but not least, geopolitical factors for capital markets. Altogether they caused volatility to pick up. As soon as the month started, the first correction to speak of since the beginning of the rally in November set in on the equity market. This was spurred on by another flare up in the conflict in the Middle East, which took the form of attacks and counterattacks between Iran and Israel. Fortunately, this conflict has not yet escalated further. What was notable about the reactions from the market was not the sell-off in equities and the initial flight to safe havens such as U.S. Treasuries but the relatively quick resumption of the original rising trend in interest rates. For example, 10-year U.S. Treasuries have now returned to a level that caused stress for equities last summer. Even though earnings season has so far gone better than expected, this presents a headwind for equities’ continued performance that must not be underestimated. Especially since, in all likelihood, there won’t be any added tailwind either from all that many interest rate cuts on the part of Western central banks. Against the backdrop of ongoing inflation, expectations for interest rate cuts this year have fallen to less than 1.5 in the U.S. and just under three in Europe.

In these circumstances, a solidly constructed and well balanced portfolio was called for. This is precisely why the Ethna-AKTIV did well. Both the USD position and the interest rate overlay made a positive contribution to performance in a challenging month, containing the need for additional risk management measures. Quite the contrary: after Israel’s most recent missile attack, we increased to 35% the equity allocation that had been reduced to 25% at the beginning of the month, as we see the current consolidation in the equity market as just that – a consolidation – and not the beginning of a bear market. Only slight changes were made to the basic composition of the equity portfolio. The only urgent need for action we saw was with regard to the interest rate overlay. When the aforementioned geopolitical escalation began, we quickly reversed the reduction in interest rate sensitivity, as a potential flight to safety would have flown in the face of our positioning towards rising interest rates. However, as this movement did not materialise, we reduced modified duration to 1.2. Looking ahead, communications from and the actions of central banks will be interesting. Western central banks have little scope to cut interest rates at the moment due to persistent inflation, and the resulting “higher for longer” mantra is supporting the U.S. dollar above all. The yen was particularly hard hit last month. With the yen at a 34-year low against the U.S. dollar, the Japanese central bank felt compelled at month-end to intervene in the currency market. As they began this intervention much later than we expected, the yen position had already been reduced over the course of the month by 5% down from 15%. We are currently waiting to see what happens, but expect a turnaround in the trend in the short term in favour of the yen.

Fund positioning

Figure 5: Portfolio structure* of the Ethna-AKTIV

Figure 6: Portfolio composition of the Ethna-AKTIV by currency

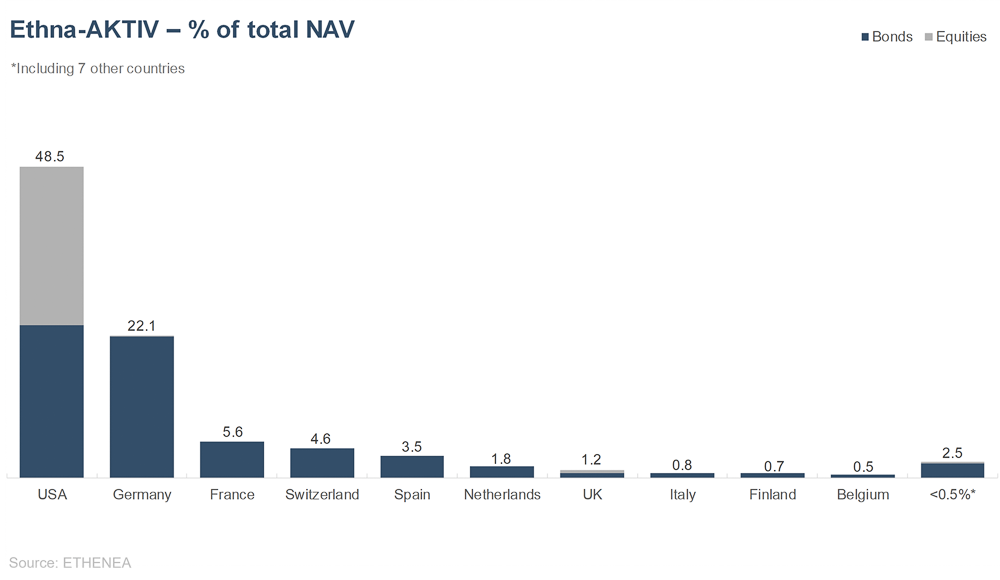

Figure 7: Portfolio composition of the Ethna-AKTIV by country

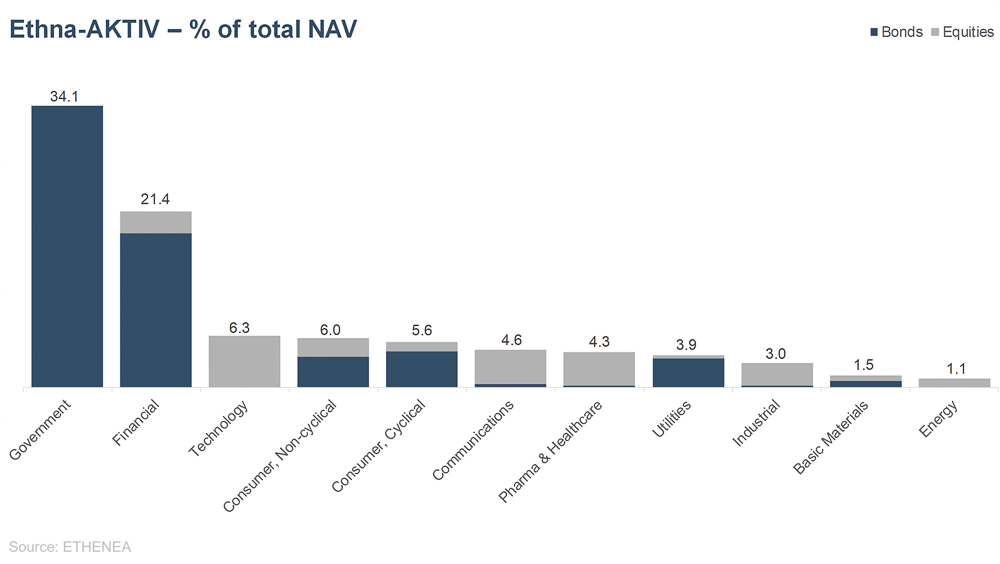

Figure 8: Portfolio composition of the Ethna-AKTIV by issuer sector

Ethna-DYNAMISCH

Key points at a glance

- In April, equity markets underwent the first significant correction this year.

- With its phased hedging of the equity component and good quarterly results from its portfolio stocks, the Ethna-DYNAMISCH bucked the rather unsettled trend.

- Lots of minor portfolio adjustments were made.

- Looking ahead, our assessment of the market remains constructive, even if volatility, which has recently increased, continues to be a factor for some time.

30 April 2024 – After a few comparatively quiet months, capital markets exhibited a little more jitteriness in April. It’s hard to pin down a single trigger. It was more a case of a confluence of higher bond yields, evaporated hopes for interest rate cuts in the U.S., small clouds on the economic horizon, equity prices that have, in some cases, run a little too far ahead, and very high levels of investment in the case of trend-following investors. Compounding this was the justified fear of a further immediate geopolitical escalation in the Middle East. No one factor by itself posed an appreciable danger to the basically constructive outlook, which we have gone into on more than one occasion in the past in our commentary. But altogether these factors were enough to bring the upward trend to a halt.

If we take a closer look at the correction, we see that it was most pronounced in small caps, even though this group was already one of the laggards. Thus, the hotly anticipated comeback of second-tier stocks has once again failed to materialise and many small-cap indices, such as the Russell 2000 in the U.S. and the MDAX in Germany, are back in negative territory since the start of the year. The discounts in valuations we are seeing in this segment do not as yet confirm the slowly improving economic prospects. Equity markets tend to remain divided; into more expensive, high-growth stocks, and cheaper, fundamentally stagnant ones.

Our task as portfolio manager of an asset-managed, equity-focused multi-asset fund is to continually weigh up the respective risks and opportunities – both macro-economic, in selecting an appropriate level of investment and asset allocation (top-down) and micro-economic, in selecting suitable individual stocks (bottom-up). The strengths of both approaches came to light in April.

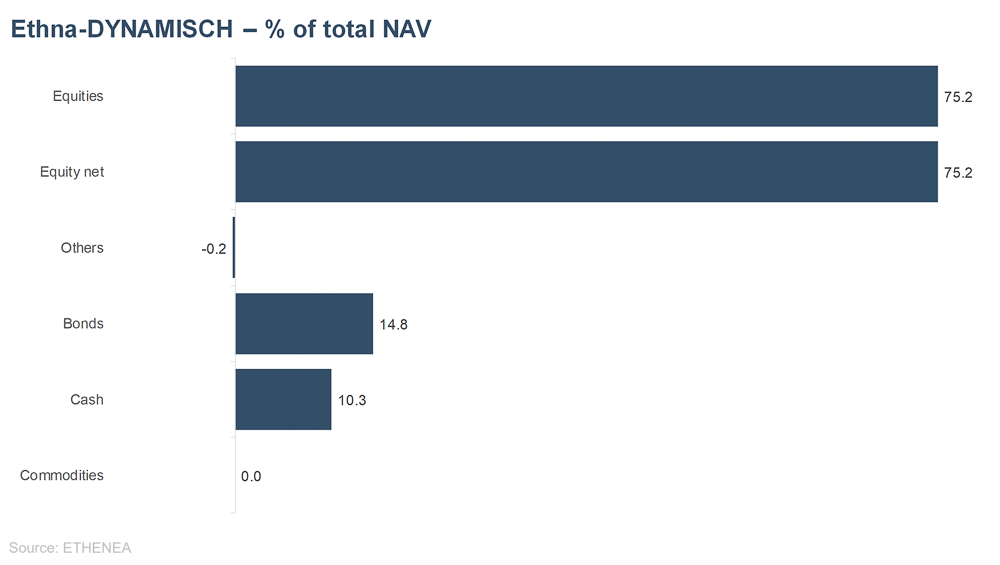

Against the backdrop described above, at the start of the month we decided based on our top-down analyses to hedge one third of the equity component using derivatives, thereby reducing the Ethna-DYNAMISCH’s level of investment from around 75% to approximately 50%. With this reduced level of risk, we waited out much of the market correction before completely reversing the hedges over the rest of the month.

On the bottom-up side, the focus was on earnings season, which was successful for most companies in the Ethna-DYNAMISCH portfolio. This was the case in particular for some of our highest-weighted names that we regard as suitably attractive, and which we also regularly feature on ETHENEA’s LinkedIn profile under the hashtag #derAktienexpress. Also, thanks to the tailwind from stocks such as Alphabet, ResMed and Unilever, the fund finished up April close to its March value, despite the equity market correction in the intervening month. In parallel, over the course of the month, we made a number of adjustments to the weight of individual positions in order to reflect the risk-reward ratios within the fund that are changing with market volatility.

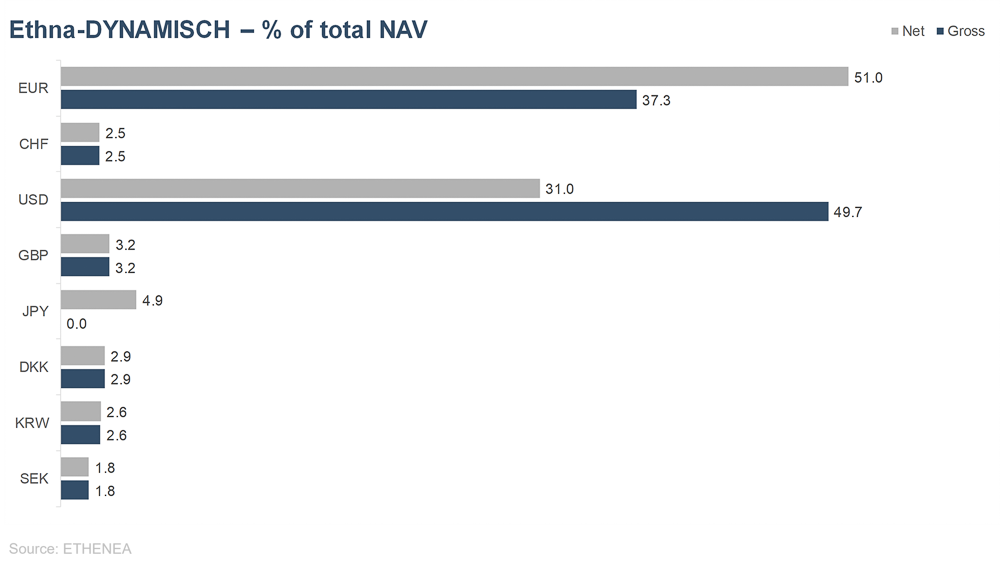

Only the currency position in the Japanese yen (JPY) opened in March did not perform as positively as hoped. The interest rate and yield differentials relevant for currency pairs drifted further apart and, also, Japan’s rhetoric concerning the increasingly weak JPY was much more restrained than we expected. Having timed the opening of the position well, losses were well contained, despite the JPY hitting a new year-to-date low against the EUR. Nevertheless, we halved the position from its original 10% to 5%. If there are no major foreign exchange interventions by the Japanese authorities in May, we will close the remaining position soon.

On the whole, the capital market climate is likely to remain quite bleak in the months to come. Without doubt, with its high degree of flexibility, its replete toolkit and its solid foundation of attractive individual securities, we consider the Ethna-DYNAMISCH to be well equipped to weather any storms not just adequately but also to actively seize any opportunities that develop from them.

Fund positioning

Figure 9: Portfolio structure* of the Ethna-DYNAMISCH

Figure 10: Portfolio composition of the Ethna-DYNAMISCH by currency

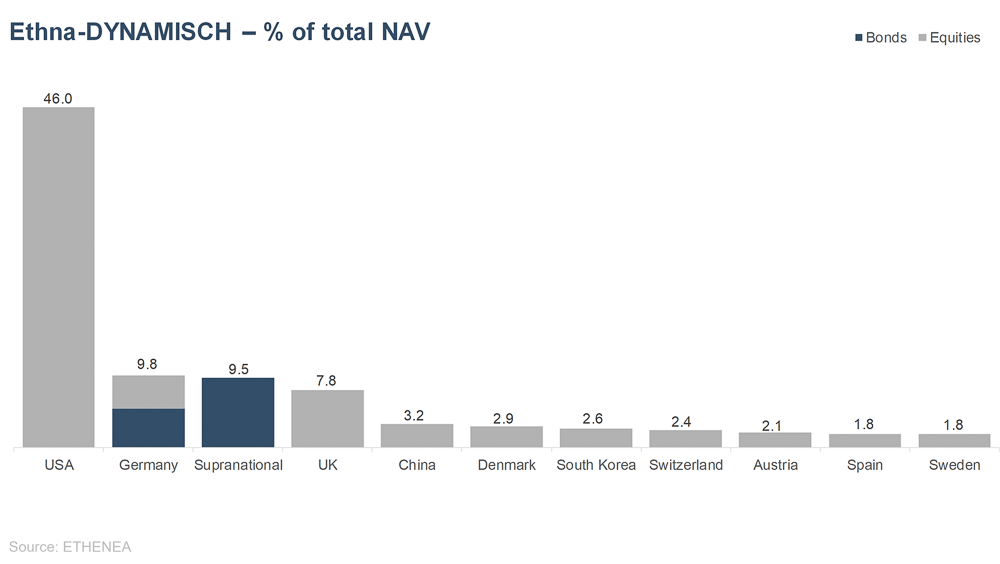

Figure 11: Portfolio composition of the Ethna-DYNAMISCH by country

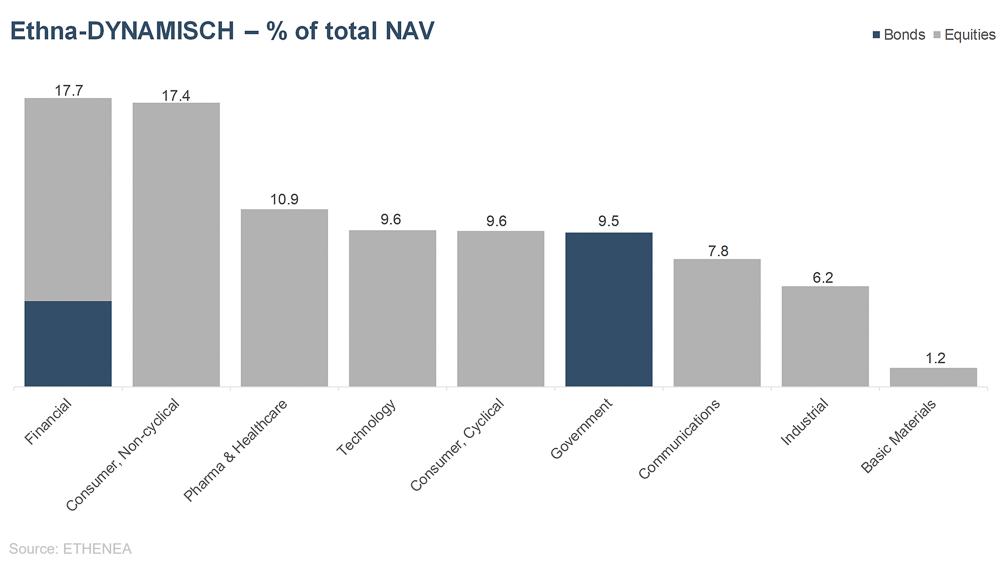

Figure 12: Portfolio composition of the Ethna-DYNAMISCH by issuer sector

* “Cash” comprises term deposits, call money and current accounts/other accounts. “Equities net” comprises direct investments and exposure resulting from equity derivatives.

HESPER FUND – Global Solutions (*)

Key points at a glance

Higher for longer….

- Sticky inflation derailed the rate-cut path expected by the market

- Global yields soared as inflation continues to surprise on the upside

- Stocks broke 5-months winning streak as rate-cut hopes waned

- Chinese equities rebounded as economic activity picks up pace

- Yen swung wildly after first slide past 160 since 1990 catching traders in short squeeze at the end of the month.

- The HESPER FUND – Global Solutions interrupted four months of positive returns.

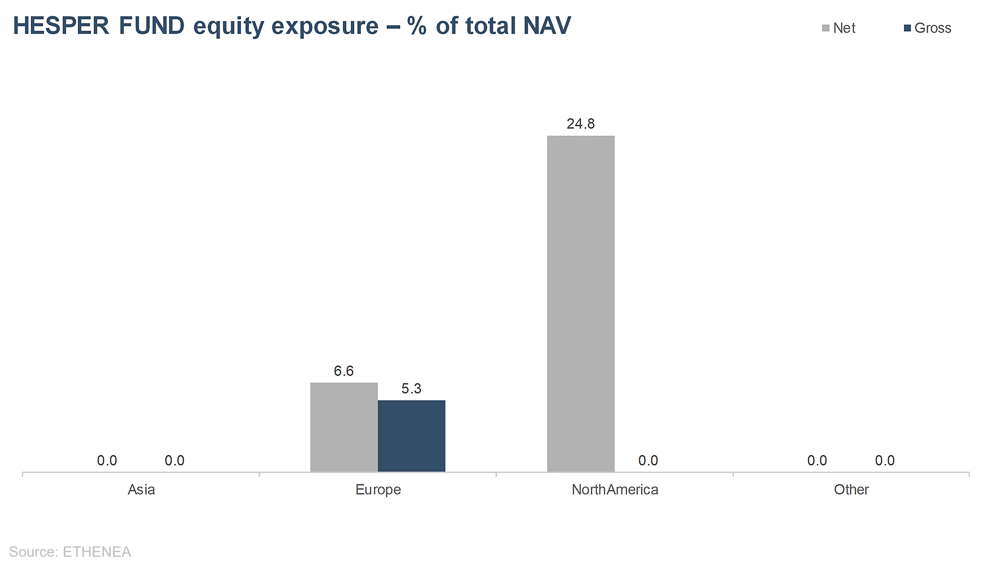

- The HESPER FUND – Global Solutions fine-tuned its portfolio allocation. Net equity exposure was reduced to 30% and duration cut into negative territory (-0.85). In FX, the fund rebuilt the long exposure to the Norwegian krone up to 20%, kept the US dollar at around 50%, and raised GBP short exposure to -40%.

30.04.24 - Rates will stay higher for longer than expected

Rate cuts are still on the Fed’s agenda, but they will likely come much later and less deep than markets discounted at the beginning of the year. For the time being, the direction of travel is still clear but it will take longer and rates will likely not come back to their pre-pandemic level. Sticky inflation, a buoyant economy and fiscal stimulus during an election year make the Fed’s job much harder. The sticky inflation of the first quarter may be more than a simple bump in the road, and even in the Eurozone disinflation is showing signs of stalling while the economy has bottomed out and may start to pick up.

Soaring yields hit equitie

US equities interrupted a five-month rally. Soaring yields, some big techs earnings misses and confusing signs about consumer confidence weighed on stocks during April.

Yields soared up as traders saw the Fed further delaying the first rate cut. Four months of higher-than-expected inflation readings reinforced the idea that the Fed is not yet confident enough that inflation will return sustainably to its target rate of 2%. “Higher for longer” seems to be the new Fed’s mantra.

In the US, the major indices corrected. The S&P 500 plunged 4.2% and the DJIA fell 5%. The tech-heavy NASDAQ lost 4.4% despite Microsoft’s and Alphabet’s strong first quarter earnings. The small cap index Russel 2000 tanked 7.1%.

In Europe, the Euro Stoxx Index fell 3.2% (-2% in USD), while the FTSE 100 rose 2.4% (+1.5% in USD) underpinned by miners and banks. The Swiss Market Index plunged 4% (-5.7% in USD, as the Swiss franc weakened further).

In Asia, stocks were mixed. China’s efforts to stabilise its financial markets showed promising results, as the economy grew better than expected 5.3% during the first quarter. China’s factory activity held up well in April. The Hang Seng jumped by 7.4% and the CSI 300 gained 1.9% (+1.6% in USD). The Korean stock market fell 2% (-4.6% in USD) and the Indian Sensex gained 1.1% (+1% in USD). The Japanese Nikkei plunged 4.9% (-8.1% in USD as the yen slid past 160 against the dollar, presumably forcing BoE intervention last Monday).

Yen weakness is something to handle with care

After 17 years, in March the Bank of Japan ended the era of negative interest rates but gave little indication of further policy tightening. Its dovish tone sent the weak yen drifting even lower and global yields were not dragged up as feared.

For Chinese and Korean exporters, the yen weakness has become a headache, troubling exports and delaying the economic recovery. On the other hand, unwinding the very crowded carry trade against the yen is a delicate task that could unleash extreme volatility through many markets, especially with yields soaring in Western countries.

As the yen slid to its weakest level since 1990, the BoJ stepped up its intervention warnings

The yen sharp and brief jump prompted chatter of BoJ intervention, although the BoJ decided to keep traders in the dark on its actions. Given the very crowded nature of the yen carry trade and the leverage chains financing the trade, yen intervention is a major source of markets’ concerns.

HESPER FUND – Macro Scenario: sticky inflation constrains Fed to delay rate cuts

Central banks are navigating a challenging scenario of uncertain disinflation, tepid economic activity amid political elections, and rising geopolitical tensions. Central banks need to carefully assess the risks of remaining hawkish for too long, with the risk of cutting rates too soon and missing their target. In the US, inflation readings have continued to disappoint, while economic activity remained solid, forcing the Fed to further delay any rate cuts and even raising questions on whether policy is tight enough. In the Eurozone, disinflation has been progressing at a better pace than in the US, but, with economic activity giving initial signs of picking up, it may also start to stall. With the supply side of the inflation equation having already delivered its benefits, we may still need to see some softening in demand to achieve the central banks’ inflation targets. The combination of a strong fiscal support, a healthy labour market, and geopolitical tensions, however, could further delay or even spoil the disinflationary path.

As long as the economy holds up and the carrot of upcoming rate cuts remains in sight, equity markets could shrug off higher yields. However, the Goldilocks scenario of the first quarter of this year seems (at least for the time being) gone and we expect higher volatility ahead.

Positioning and monthly performance

The HESPER FUND – Global Solutions decreased in April (unit class T-6 EUR -1.13%), dragged down by equities and mixed FX bets. YTD, the fund is up 2.38%

To hedge against this more challenging environment, the HESPER FUND reduced its overall equity exposure to 30%. Neutral duration exposure was cut further to become negative (almost -0.9 years). The fund continued to trade actively in the FX space, maintaining the dollar exposure at 50%. GBP short exposure was increased to -40% as we rebuilt long NOK bets (20%).

The breakdown of MTD (-1.13%) was +0.38% fixed income (-0.04% long positions, +0.42% short future positions), -1.60% equities, +0.03% commodities, +0.17% currencies and -0.13% fees and expenses. Decorrelation with traditional assets such as equities and bonds remained high.

Total assets fell to EUR 57 million at the end of the month. The unit class T-6 EUR unit class was 8.23% below its all-time high on 29 September 2022.

Volatility over the last 250 days ticked up to 6.1%, maintaining an attractive risk/return profile. The annualised return since inception has decreased to 3.26%.

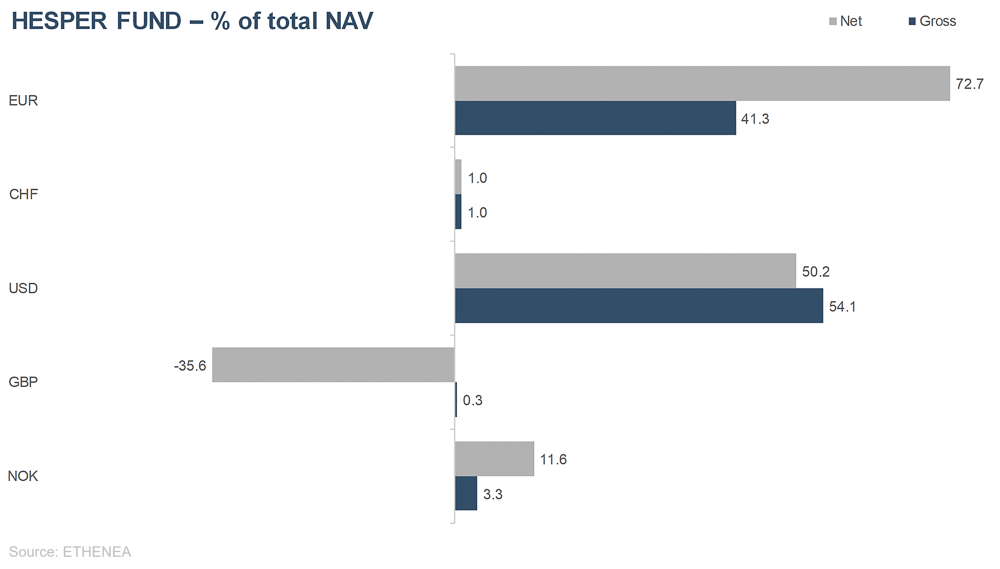

Looking ahead to next month, the fund has continued to stay far away from its reference currency and to trade actively in the FX space. Currently, the currency exposure of the HESPER FUND – Global Solutions is as follows: USD 50%, NOK 20%, CHF 1% and GBP -40%.

As in the past, we will continue to monitor and calibrate the fund’s exposure to the various asset classes in line with market sentiment and changes in the macroeconomic baseline scenario.

*HESPER FUND - Global Solutions is currently only authorised for distribution in Germany, Luxembourg, Belgium, Italy, France, Austria and Switzerland.

Fund positioning

Grafik 13: Aktien-Exposure nach Regionen des HESPER FUND − Global Solutions

Grafik 14: Währungs-Allokation des HESPER FUND − Global Solutions

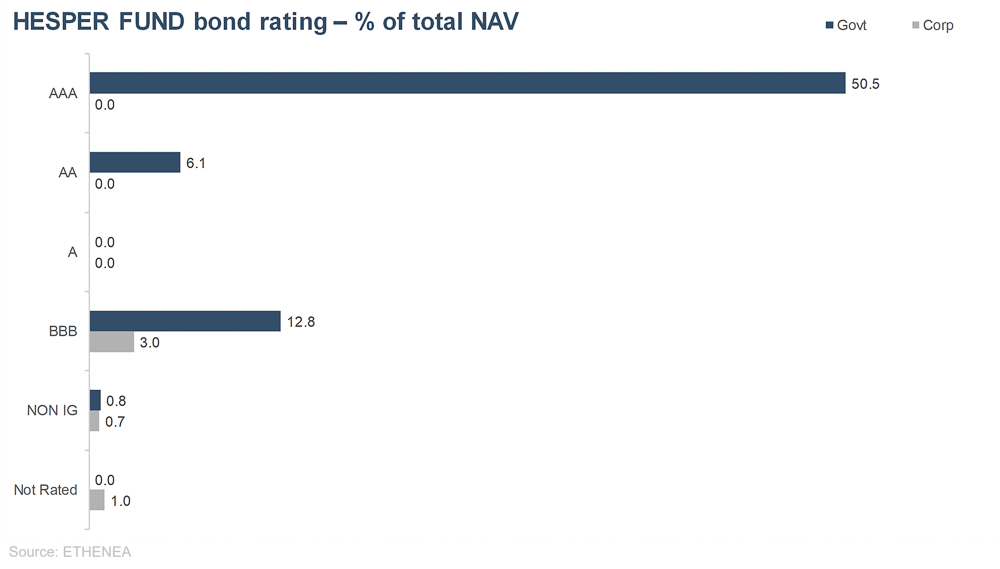

Grafik 15: Ratingstruktur der Anleihen des HESPER FUND − Global Solutions

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

Esta comunicación publicitaria es únicamente para fines informativos. Está prohibida su transmisión a personas en países donde el fondo no está autorizado para su distribución, especialmente en EE.UU. o a personas estadounidenses. La información no constituye una oferta ni una invitación para comprar o vender valores o instrumentos financieros y no sustituye el asesoramiento personalizado al inversor o al producto. No tiene en cuenta los objetivos de inversión individuales, la situación financiera ni las necesidades particulares del destinatario. Antes de tomar una decisión de inversión, deben leerse cuidadosamente los documentos de venta vigentes (folleto, documentos de información clave/PRIIPs-KIDs, informes semestrales y anuales). Estos documentos están disponibles en alemán y en traducción no oficial en la sociedad gestora ETHENEA Independent Investors S.A., en el depositario, en los agentes de pago o de información nacionales, así como en www.ethenea.com. Los términos técnicos más importantes se encuentran en el glosario de www.ethenea.com/glosario/. La información detallada sobre oportunidades y riesgos de nuestros productos se encuentra en el folleto vigente. La rentabilidad pasada no es un indicador fiable de la rentabilidad futura. Los precios, valores y rendimientos pueden subir o bajar y pueden llevar a la pérdida total del capital invertido. Las inversiones en divisas extranjeras están sujetas a riesgos de tipo de cambio adicionales. No se pueden derivar compromisos ni garantías vinculantes para resultados futuros a partir de la información proporcionada. Las suposiciones y el contenido pueden cambiar sin previo aviso. La composición de la cartera puede cambiar en cualquier momento. Este documento no constituye una información completa sobre riesgos. La distribución del producto puede dar lugar a remuneraciones para la sociedad gestora, empresas vinculadas o socios de distribución. Son determinantes los datos sobre remuneraciones y costes que figuran en el folleto vigente. Una lista de los agentes de pago e información nacionales, un resumen de los derechos de los inversores y las advertencias sobre los riesgos de un cálculo erróneo del valor liquidativo están disponibles en www.ethenea.com/avisos-legales/. En caso de error en el cálculo del valor liquidativo, la compensación se realizará conforme a la Circular CSSF 24/856; para participaciones suscritas a través de intermediarios financieros, la compensación puede estar limitada. Información para inversores en Suiza: El país de origen del fondo de inversión colectiva es Luxemburgo. El representante en Suiza es IPConcept (Schweiz) AG, Bellerivestrasse 36, CH-8008 Zúrich. El agente de pagos en Suiza es DZ PRIVATBANK (Schweiz) AG, Bellerivestrasse 36, CH-8008 Zúrich. El folleto, los documentos de información clave (PRIIPs-KIDs), los estatutos y los informes anuales y semestrales pueden obtenerse gratuitamente del representante. Información para inversores en Bélgica: El folleto, los documentos de información clave (PRIIPs-KIDs), los informes anuales y semestrales del subfondo están disponibles gratuitamente en alemán a petición de ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxemburgo y del representante: DZ PRIVATBANK AG, Niederlassung Luxemburg, 4, rue Thomas Edison, L-1445 Strassen, Luxemburgo. A pesar del máximo cuidado, no se garantiza la exactitud, integridad o actualidad de la información. Solo los documentos originales en alemán son vinculantes; las traducciones son solo para fines informativos. El uso de formatos publicitarios digitales es bajo su propia responsabilidad; la sociedad gestora no asume ninguna responsabilidad por fallos técnicos o violaciones de la protección de datos por parte de proveedores externos de información. El uso solo está permitida en países donde esté legalmente autorizado. Todos los contenidos están protegidos por derechos de autor. Cualquier reproducción, distribución o publicación, total o parcial, solo está permitida con el consentimiento previo por escrito de la sociedad gestora. Copyright © ETHENEA Independent Investors S.A. (2025). Todos los derechos reservados. 06-05-2024