Inflation and long-term interest rates – looking ahead

Key points at a glance

- The longer-term inflation trend in 2023 and 2024, and the resulting progression of central bank interest rates, is key to how long-term interest rates will develop.

- Inflation rates in Europe and the U.S. are likely to rise in the current quarter but come back down towards the end of the year and especially at the beginning of 2023.

- Both the Fed and the ECB will raise their interest rates.

- An at least temporary increase in 10-year Bund yields to 1.25% and in 10-year Treasury yields to 3.25% is likely in the second quarter of 2022.

- A further rise in central-bank as well as long-term interest rates is possible.

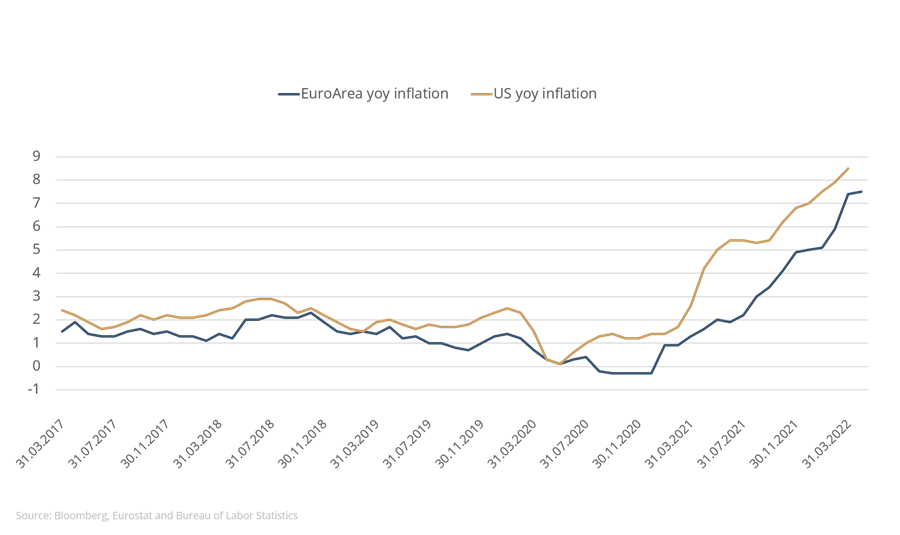

Inflation in the U.S. rose to 8.3%, while in the eurozone it rose to 7.5% in April of this year. It’s clear that inflation will remain very high for the time being; the question is how much further it will climb in the coming months. The ECB and the Fed are alarmed by developments. What will the central banks do to combat inflation and how high could long-term interest rates go?

Figure 1: Inflation eurozone vs U.S.

What we know

The Fed has already terminated its bond-buying programme and in March and May 2022 raised the Fed Funds rates in order to break the inflation dynamic. What’s certain is that further rate hikes will follow. In addition, the Fed will reduce its balance sheet by selling holdings of sovereign and mortgage-backed bonds or by not reinvesting the proceeds of maturing securities. However, the actions and announcements of the central bank alone have so far hardly done anything to curb the inflation rate. While inflation in January 2022 was 7.5%, it rose to 7.9% in February and in April hit 8.3% - a level last seen at the beginning of the 1980s. It’s a similar story in the eurozone. Inflation rose from 5.1% in January to 7.5% in April. The ECB has reduced the pace of its net bond-buying without ending it entirely, but has left its interest rates unchanged.

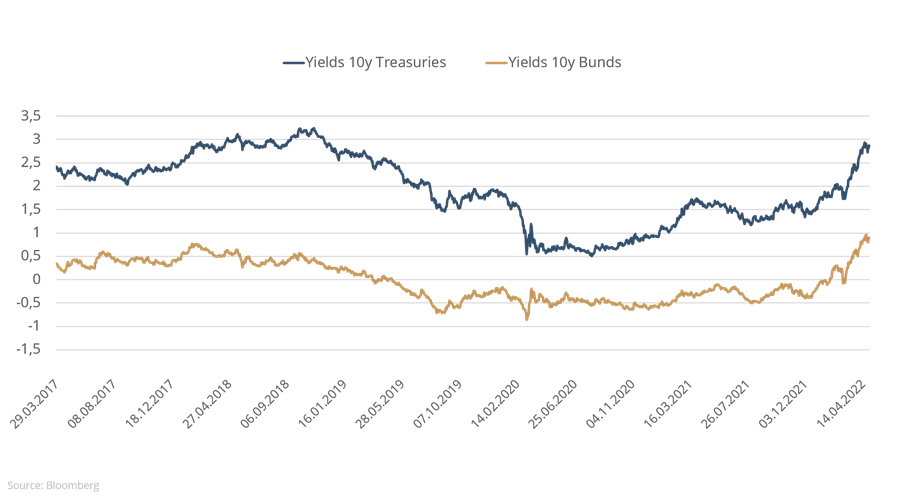

“10-year yields are out of the negative zone.”

Yields on long-dated bonds have risen sharply, as have rates for new credits. For property loans with first-class collateral and a 10-year fixed term, investors are already paying well over 2% in Germany. Interest rates for the 30-year mortgages common in the U.S. stand at 5.25% – the highest rate since 2010.

What we can expect

Given what we know, it is comparatively easy to predict what the central banks will do: both the Fed and the ECB will raise their interest rates. The Fed will raise the Fed Funds Rate significantly by the end of the year. A new target range of 2.5% to 2.75%, or even slightly higher, is likely. In a similar vein, the ECB is likely to end negative interest rates for its deposit facility by the end of the year. It’s even possible that the repo rate will be raised before the year is out. The outlook for the future inflation trend is more complicated. While in the U.S. individual inflation components have already fallen or are only rising slowly, rents and the cost of building an owner-occupied home are only just taking off. Second-round effects due to higher wages, energy prices and transport costs will continue to push up prices of goods and services. However, the pace is hard to predict. In Europe, the explosion in energy prices is hugely important for inflation. Given the possibility of boycotts and the fact that electricity generation relies on wind and water levels, it’s very hard to say how things will develop on this front. On the other side of the ledger is – as yet unquantifiable – state intervention, which, while reducing inflation, will lead to higher national debt. In our view, however, it is quite likely that annualised inflation both in the U.S. and in Europe will increase slightly further in the second quarter but not exceed the 10% mark. We expect inflation to fall again slightly at the end of the year. Inflation rates of over 5% - perhaps even 6% - should still be expected for December 2022.

What we don’t know (yet)

However, the longer-term inflation trend in 2023 and 2024 and the resulting progression of central bank interest rates is even more key to how long-term interest rates will develop. We can speculate on this no end, but not much is certain. Even the reduction of the Fed’s balance sheet in the U.S. and the discontinuation of purchases by the ECB could cause upheaval. Nobody knows who will replace the central banks as purchasers. An at least temporary increase in 10-year Bund yields to 1.25% and in 10-year Treasury yields to 3.25% is likely in the second quarter. After that, however, the market is likely to take a breather for the time being. Yields have already soared and there is huge uncertainty about what 2023 will bring. At any rate, given exorbitant rates of inflation, we are ruling out the possibility of further economic upturn both in the eurozone and in the U.S. Either the economy will weaken first, bringing about lower inflation and less need for the central banks to act, or persistently high inflation will affect consumer sentiment, thus leading to a sharp economic downturn. In any case, growth in the first quarter of 2022 has already declined sharply; GDP in the U.S. has even fallen slightly compared with the previous quarter.

Figure 2: Yields on 10-year sovereign bonds

Even if inflation rates in Europe and the U.S. rise slightly further in the current quarter they will come back down towards the end of the year and especially at the beginning of 2023. But it seems uncertain to us whether inflation will fall to the desired 2% region as a result of the restrictive measures expected from the central banks. If the expectation arises that inflation in 2023 and 2024 will tend to level off between 3% and 4%, then the central banks would be compelled to adjust their policy once again. A further increase in central bank interest rates and long-term interest rates would then ensue.

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

Esta comunicación publicitaria es únicamente para fines informativos. Está prohibida su transmisión a personas en países donde el fondo no está autorizado para su distribución, especialmente en EE.UU. o a personas estadounidenses. La información no constituye una oferta ni una invitación para comprar o vender valores o instrumentos financieros y no sustituye el asesoramiento personalizado al inversor o al producto. No tiene en cuenta los objetivos de inversión individuales, la situación financiera ni las necesidades particulares del destinatario. Antes de tomar una decisión de inversión, deben leerse cuidadosamente los documentos de venta vigentes (folleto, documentos de información clave/PRIIPs-KIDs, informes semestrales y anuales). Estos documentos están disponibles en alemán y en traducción no oficial en la sociedad gestora ETHENEA Independent Investors S.A., en el depositario, en los agentes de pago o de información nacionales, así como en www.ethenea.com. Los términos técnicos más importantes se encuentran en el glosario de www.ethenea.com/glosario/. La información detallada sobre oportunidades y riesgos de nuestros productos se encuentra en el folleto vigente. La rentabilidad pasada no es un indicador fiable de la rentabilidad futura. Los precios, valores y rendimientos pueden subir o bajar y pueden llevar a la pérdida total del capital invertido. Las inversiones en divisas extranjeras están sujetas a riesgos de tipo de cambio adicionales. No se pueden derivar compromisos ni garantías vinculantes para resultados futuros a partir de la información proporcionada. Las suposiciones y el contenido pueden cambiar sin previo aviso. La composición de la cartera puede cambiar en cualquier momento. Este documento no constituye una información completa sobre riesgos. La distribución del producto puede dar lugar a remuneraciones para la sociedad gestora, empresas vinculadas o socios de distribución. Son determinantes los datos sobre remuneraciones y costes que figuran en el folleto vigente. Una lista de los agentes de pago e información nacionales, un resumen de los derechos de los inversores y las advertencias sobre los riesgos de un cálculo erróneo del valor liquidativo están disponibles en www.ethenea.com/avisos-legales/. En caso de error en el cálculo del valor liquidativo, la compensación se realizará conforme a la Circular CSSF 24/856; para participaciones suscritas a través de intermediarios financieros, la compensación puede estar limitada. Información para inversores en Suiza: El país de origen del fondo de inversión colectiva es Luxemburgo. El representante en Suiza es IPConcept (Schweiz) AG, Bellerivestrasse 36, CH-8008 Zúrich. El agente de pagos en Suiza es DZ PRIVATBANK (Schweiz) AG, Bellerivestrasse 36, CH-8008 Zúrich. El folleto, los documentos de información clave (PRIIPs-KIDs), los estatutos y los informes anuales y semestrales pueden obtenerse gratuitamente del representante. Información para inversores en Bélgica: El folleto, los documentos de información clave (PRIIPs-KIDs), los informes anuales y semestrales del subfondo están disponibles gratuitamente en alemán a petición de ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxemburgo y del representante: DZ PRIVATBANK AG, Niederlassung Luxemburg, 4, rue Thomas Edison, L-1445 Strassen, Luxemburgo. A pesar del máximo cuidado, no se garantiza la exactitud, integridad o actualidad de la información. Solo los documentos originales en alemán son vinculantes; las traducciones son solo para fines informativos. El uso de formatos publicitarios digitales es bajo su propia responsabilidad; la sociedad gestora no asume ninguna responsabilidad por fallos técnicos o violaciones de la protección de datos por parte de proveedores externos de información. El uso solo está permitida en países donde esté legalmente autorizado. Todos los contenidos están protegidos por derechos de autor. Cualquier reproducción, distribución o publicación, total o parcial, solo está permitida con el consentimiento previo por escrito de la sociedad gestora. Copyright © ETHENEA Independent Investors S.A. (2026). Todos los derechos reservados. 03-05-2022