Your questions, our answers

Markets continue to be influenced by geopolitics and persistently high inflation on both sides of the Atlantic. In our second quarterly update of the year, portfolio managers responded to the following questions, among others, to explain their views.

Ethna-DEFENSIV

Ethna-AKTIV

Ethna-DYNAMISCH

Ethna-DEFENSIV

When do you think it is time to invest in or switch to longer-dated bonds? What would be your criteria for selecting longer-dated bonds?

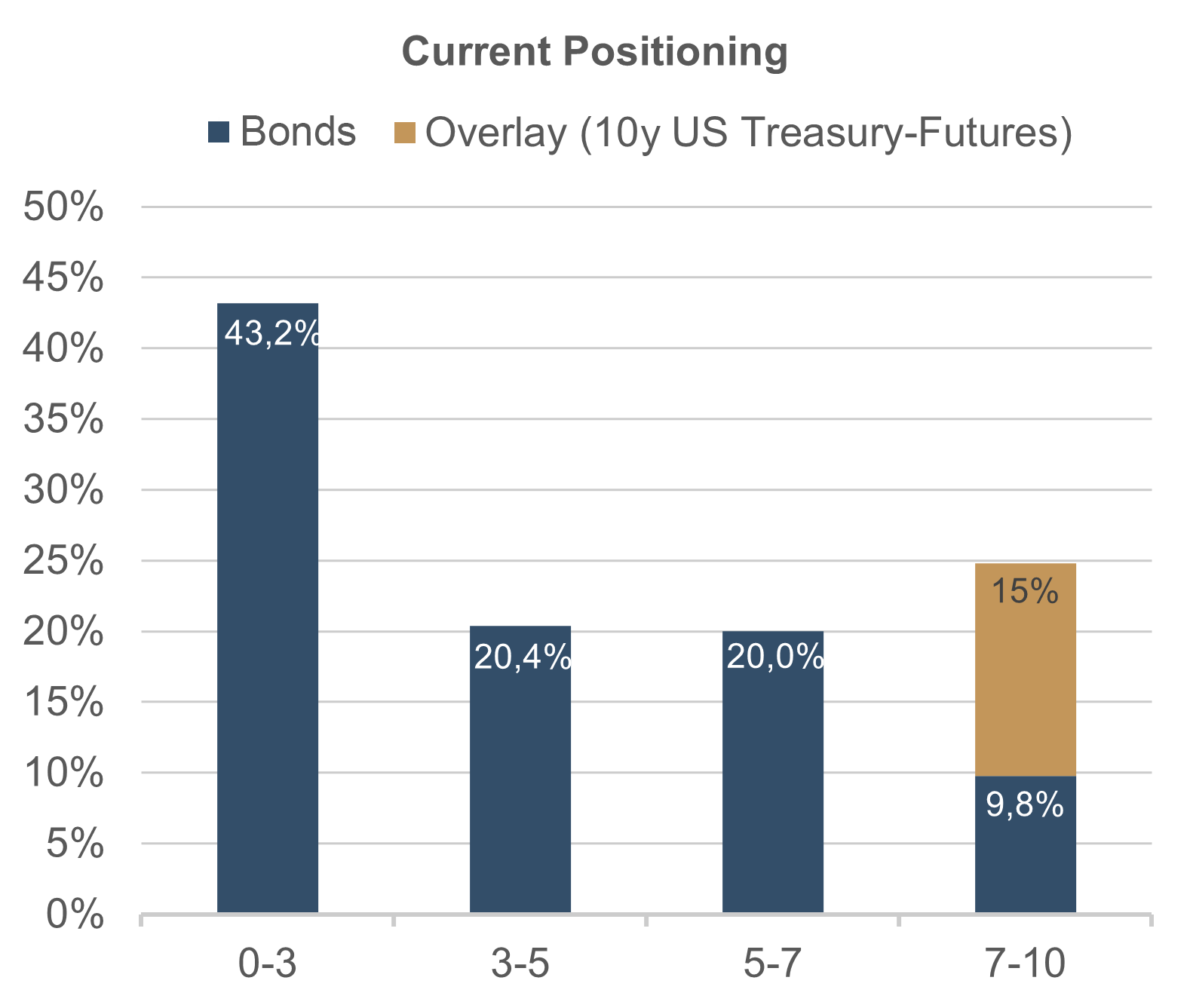

From our point of view, this time has already come. In recent weeks, we have invested opportunistically in the corporate bonds with maturities between 2028 and 2032. The slowdown of the global economy, especially in the industrialised countries such as the US and the EU, as well as falling inflation rates give us reason to expect lower yields at the longer end of the yield curve. An increase in duration therefore seems attractive to us. So far, we have increased the interest rate sensitivity of our portfolio to 4.4 by investing in new issues and building a 15% position in 10-year US Treasuries.

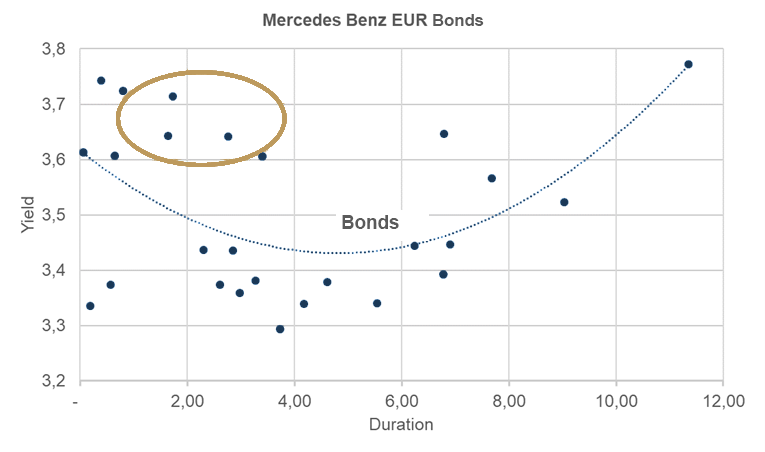

There are two factors to consider when selecting individual positions. The first is yield. In the current economic environment, we can achieve higher returns without taking on more risk. Yields above 4.5% are attractive to us at the moment, and we are closely monitoring new issues in this area. At the same time, the second factor is the inversion of the government yield curve. For some safer companies, the risk premium is not sufficient to form an inverted curve (government yield + risk premium). For example, the government yield at the short end and the risk premium at the long end of the Mercedes Benz yield curve have a greater impact, leading to a U-shaped curve (blue line in Figure 1).

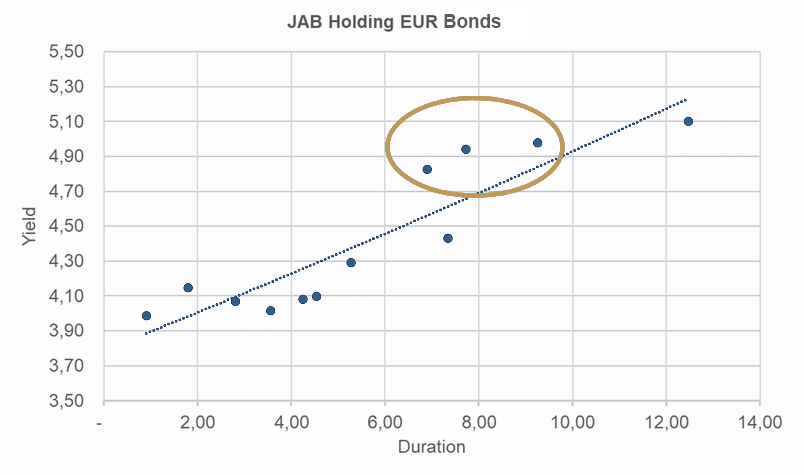

Other companies offer higher risk premiums. Companies such as JAB Holdings, Autostrade per L'Italia Autostrade, Fiserv or VW have linearly rising yield curves:

We are therefore currently positioned to benefit from the inversion with 43.2% exposure in the 0-3 year maturities and 24.8% (incl. futures overlay) at the long end.

Ethna-AKTIV

Ethna-AKTIV has always been a very conservative fund, so the equity allocation is surprising, especially given the current situation on the capital markets. Can you please explain this?

The Ethna-AKTIV is still the right choice for the conservative and risk-conscious investor. However, the attributes active and flexible are also part of our offering. Our task is to find the optimal asset allocation for attractive long-term capital growth, depending on the market environment. This is usually derived from an assessment of the macroeconomic situation, valuation parameters and positioning data. At the end of the first quarter, we noted a clear disconnect between the available macro data, including our forecasts, and the measurable reaction of market participants (flows and positioning). Despite declining inflation, stable to positive markets for months, and an economic outlook that was relatively constructive to us, the sentiment and positioning of many market participants was very negative. We recognised this opportunity and our flexible approach allowed us to adjust the portfolio accordingly. It is important to note that this does not contradict the conservative nature of the portfolio. On a risk/reward basis, the opportunities outweighed the risks at the time. Firstly, a market that everyone expects to fall is relatively well supported. You have usually hedged accordingly. Second, when prices are stable, it often only takes a catalyst to adjust positioning and follow a new narrative. The shift from the recession to the soft-landing narrative and the hype about the potential efficiency gains from artificial intelligence were just such catalysts. But adjusting the equity exposure was not the only adjustment. We have also significantly increased the duration of the bond portfolio this year and hedged all currency risks. This means that changing a specific allocation is never an isolated decision but must always be seen in the context of the entire portfolio. In the meantime, however, the starting position on the equity side has changed to the extent that we are currently discussing a return to a more neutral position. Always in the spirit of: Taking active and flexible advantage of opportunities.

Ethna-DYNAMISCH

Looking at the hype around AI and NVIDIA's spectacular performance: Do you think it is sustainable? Do you want to allocate part of Ethna-DYNAMISCH to this segment to participate in the potential gains of this industry?

Although Artificial Intelligence (AI) is nothing new, it is the ChatGPT application that seems to have really caught the public's imagination. So much so that hardly a day goes by without another company announcing its AI solutions and capabilities. The stock market is taking notice.

We don't want to underestimate the fact that AI has the potential to change many things. From efficiency gains to new products and services. But we are sceptical that this will happen as suddenly as the recent performance of some stocks suggests. Spectacular really is the appropriate description.

Well, not everything is fantasy, some of it is already reality: NVIDIA's latest quarterly results were huge. The fundamental performance is of course impressive. But to be considered for an investment, the valuation must also be right. Keyword: "growth at a reasonable price" (GARP). In any case, we are not entirely comfortable with an expected P/E ratio of around 50. The potential for setbacks is too great if the high growth expectations are not met. Experience shows that over-hyped themes and stocks that are flooded with inflows into active or passive fund structures have a hard time meeting expectations - and thus their valuation levels - in the future.

It is true that over a longer time horizon, valuation plays an increasingly subordinate role if the fundamentals are right. But the past has also shown that it is very difficult to identify the long-term winners in technological (r)evolutions, even if they seem obvious in retrospect. In any case, Alphabet was considered the leader in the field of AI language models until OpenAI’s ChatGPT, which is essentially funded by Microsoft, took off. Competition is very dynamic.

We are already invested in several AI companies, although this was not the basis of our initial investment decision. We also have a number of relevant stocks on our watch list. We will not hesitate to invest when opportunities arise. Until then, however, we prefer companies that are thriving outside the hype. Those with solid fundamental growth (preferably with good visibility) and attractive valuations, i.e. GARP stocks.

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

Esta comunicação publicitária tem apenas fins informativos. A distribuição a pessoas localizadas em países nos quais o fundo não está autorizado para comercialização, especialmente nos EUA ou a cidadãos norte-americanos, é proibida. As informações não constituem uma oferta ou recomendação de compra ou venda de valores mobiliários ou instrumentos financeiros, e não substituem uma consultoria específica para o investidor ou para o produto. Não consideram os objetivos de investimento individuais, a situação financeira ou as necessidades particulares do destinatário. Antes de tomar qualquer decisão de investimento, é necessário ler atentamente os documentos de venda aplicáveis (prospeto de venda, documentos informativos básicos/PRIIPs-KIDs, relatórios semestrais e anuais). Esses documentos estão disponíveis em alemão e em traduções não oficiais junto da sociedade gestora ETHENEA Independent Investors S.A., da entidade depositária, das entidades nacionais de pagamento ou de informação, bem como em www.ethenea.com. Os principais termos técnicos podem ser encontrados no glossário disponível em www.ethenea.com/glossary/. Para informações detalhadas sobre as oportunidades e riscos de nossos produtos, consulte o prospeto de venda atual. O desempenho passado não é um indicador fiável de resultados futuros. Os preços, valores e rendimentos podem subir ou descer e resultar na perda total do capital investido. Os investimentos em moedas estrangeiras estão sujeitos a riscos cambiais adicionais. As informações fornecidas não implicam quaisquer garantias ou compromissos vinculativos relativamente a resultados futuros. Os pressupostos e conteúdos podem ser alterados sem aviso prévio. A composição da carteira pode ser alterada a qualquer momento. Este documento não constitui uma explicação completa sobre os riscos. A comercialização do produto pode envolver comissões para a sociedade gestora, empresas associadas ou parceiros de distribuição. As informações sobre comissões e custos são as constantes no prospeto de venda atual. Uma lista das entidades nacionais de pagamento e informação, um resumo dos direitos dos investidores e informações sobre os riscos de erro no cálculo do NAV podem ser encontradas em www.ethenea.com/avisos-legais. Em caso de erro no cálculo do NAV, será oferecida uma compensação de acordo com o comunicado CSSF 24/856; para unidades adquiridas através de intermediários financeiros, a compensação poderá ser limitada. Informações para investidores na Suíça: O país de origem do fundo coletivo de investimento é o Luxemburgo. O representante na Suíça é a IPConcept (Schweiz) AG, Bellerivestrasse 36, CH-8008 Zurique. O agente pagador na Suíça é a DZ PRIVATBANK (Schweiz) AG, Bellerivestrasse 36, CH-8008 Zurique. O prospeto, os documentos informativos básicos (PRIIPs-KIDs), os estatutos, bem como os relatórios anuais e semestrais podem ser obtidos gratuitamente junto ao representante. Informações para investidores na Bélgica: O prospeto de venda, os documentos informativos principais (PRIIPs-KIDs), os relatórios anuais e semestrais do fundo estão disponíveis gratuitamente em português, mediante solicitação, junto da sociedade gestora ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxemburgo, e do representante: DZ PRIVATBANK AG, Niederlassung Luxemburg, 4, rue Thomas Edison, L-1445 Strassen, Luxemburgo. Apesar de toda a diligência, não é assumida qualquer garantia quanto à exatidão, integridade ou atualidade das informações. Somente os documentos originais em alemão são válidos; as traduções são fornecidas apenas para fins informativos. A utilização de formatos digitais de publicidade é feita por própria conta e risco; a sociedade gestora não se responsabiliza por falhas técnicas ou violações de dados causadas por fornecedores externos de informações. A utilização só é permitida em países onde seja legalmente permitida. Todo o conteúdo está sujeito a direitos de autor. Qualquer reprodução, distribuição ou publicação, total ou parcial, só é permitida com a autorização prévia por escrito da sociedade gestora. 20/06/2023