On the home straight

It’s a ritual that marathon runners will be familiar with – after the intensive training comes a gradual reduction in the level of training in the lead-up to the race; competitors load up on vast quantities of carbohydrates and prepare body and mind for the physical exertion. The body needs this time to recover and any hard training right before a race can actually be damaging and reduce the chances of success. Tapering originally comes from the world of marathon running, but investors will be familiar with it since 2013, if not before. Back in 2013, Fed Chair Ben Bernanke announced his intension to taper bond purchases. This came as a surprise for many market participants. Yields on US Treasuries subsequently shot up, and equity markets plummeted.

This is something the US central bank desperately wants to avoid this time round. Now, however, the calls for monetary support to be tapered in light of the fact that the economy is recovering and valuations are high across all markets are starting to become louder. Robert Kaplan, president and CEO of the Dallas Fed was the first to break cover, speaking publicly of “excesses and imbalances in financial markets” and calling for a conversation to be started sooner rather than later about adjusting monetary policy. Even the current Fed Chair Jerome Powell, whether intentionally or not, used the word “frothy” to describe the current situation in markets in the press conference following the last central bank meeting. The minutes of the FOMC meeting in May also show that a number of participants suggested that it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases.

Note that they are talking about possibly starting to talk about asset purchases, so we are a long way away from seeing an actual adjustment. We assume that the Fed will discuss tapering in the June meeting at the earliest and will not adjust their asset purchase programme before Autumn, but possibly not until the end of the year. At that, it is likely that the adjustment will only be moderate before the subject of rate hikes is raised in the next step. The ECB will presumably roll back its monetary policy later and begin tightening at the beginning of next year at the earliest.

The first central banks are demonstrating how withdrawal could work

Smaller central banks are currently demonstrating how an exit from accommodative monetary policy could work without necessarily causing a financial market crash. The Bank of Canada set the standard in April by announcing that it would reduce its bond-buying programme by around one billion Canadian dollars a week, from CAD 4 billion to CAD 3 billion (25%). Further reductions of one billion at a time are expected in the next meetings in July and September. As expected, this strengthened the Canadian dollar and led to a widening of spreads on Canadian sovereign bonds over US Treasuries. The feared taper tantrum similar to the one in 2013 and an ensuing wholesale sell-off of Canadian sovereign bonds failed to materialise.

The Bank of England is the second central bank, after the Bank of Canada, to announce a slowing of the pace of its bond-buying, from GBP 4.4 billion to GBP 3.4 billion per week. At the same time, it stressed that this should not be interpreted as a tightening of monetary policy and that the completion point of the purchase programme and the total size of GBP 895 billion will remain unchanged.

The Reserve Bank of New Zealand (RBNZ) surprised markets at the end of May with the projection that it might raise key rates as soon as the second half of 2022. However, this is conditional on the economy panning out as expected, said the Monetary Policy Committee of the RBNZ. The official cash rate will therefore be kept at a low 0.25% and the asset purchase programme of NZD 100 billion will be maintained in full for the time being. The New Zealand dollar and bond yields rose after the announcement.

Pressure also is mounting in Australia after the economic outlook in the Statement on Monetary Policy (SOMP) in May was raised and the central bank indicated that it could decide in the July meeting on the direction monetary policy would take. Bond purchases are currently capped at AUD 100 billion and the yield target for three-year sovereign bonds is 0.1%. An extension of the purchase programme and of yield curve control from April 2024 to November 2024 is under debate. The Reserve Bank of Australia is likely to want to wait for the coming economic data before making a decision. A continuation of the recovery, however, will make an extension less likely.

Furthermore, a number of smaller European central banks in central, eastern and northern Europe have recently announced a tightening of their monetary policy. In Hungary, deputy governor of the central bank Barnabás Virág announced a surprise rate hike as soon as June of this year in order to pre-empt possible runaway inflation. Inflation in April was 5.1%, the highest it has been in years. It’s a similar story in Poland and the Czech Republic, at 4.3% and 3.1%, respectively; inflation is higher than the respective central banks’ inflation targets, and the hawks are increasingly calling for a tightening of monetary policy.

Our Scandinavian neighbours are adopting a similar stance: the Riksbank in Sweden announced at the end of April that it is sticking to its guns and will exit its QE programme completely around the end of 2021. Though it never launched a bond-buying programme, Norway’s central bank, Norges Bank, announced that it is going to raise key rates in the second half of 2021. Lastly, the Icelandic central bank unexpectedly toughened its monetary stance by raising interest rates for fixed-term deposits with a maturity of seven days from 0.75% to 1%. The reasons given for the rate hike were mounting inflationary pressure and the rise in wages and property prices.

The Fed, ECB and Bank of Japan continue to exercise caution

Only the major central banks – the US central bank, the European Central Bank and the Bank of Japan – continue to tread water. There will be no change there for the time being and this is pleasing markets, especially bond investors, who generally do not like surprises.

However, the strategy does entail risks. Nobody knows for certain how the economy will be in the future, and perhaps the Fed will be proved right in thinking that the recovery will go on for much longer than we would all care for. Portfolio management, however, first and foremost also involves risk management; that is, avoiding or minimising risks that are unlikely to occur. And should the Fed be proved wrong, there could be disastrous consequences: the economy could overheat and inflation could far overshoot the 4% to 5% mark. The Fed would then have to slam on the brakes, which would not be a painless process.

This brings us back to marathon running. Perhaps just now is the right time for the US central bank to successively run off – or rather gradually wind down – its bond purchases, instead of burning out in the final straight and possibly not making it over the finish line. Other central banks are demonstrating at the moment how it can be done.

Positioning of our funds

Ethna-DEFENSIV

US economic data was mixed in May: factory production and retail sales boomed and wages rose. On the other hand, unemployment figures were disappointing: 266,000 new jobs compared with 1,000,000 projected, and the unemployment figures for March were adjusted downward by almost 150,000. That’s the situation at first glance; on reflection, the figures are perhaps not quite as bad as they seem. Many companies want to recruit but can’t get workers because many Americans are still living off their government paychecks. The struggle to find workers has taken on bizarre dimensions. McDonald’s, for instance, is paying applicants USD 50 just to show up for a job interview. So, it’s very possible that labour market figures will be well above expectations in the coming months due to catch-up effects, once the government payments are spent.

In Europe, after a rather sluggish start, vaccination campaigns are still proceeding very slowly. In Germany, 50% of the population will soon have received at least one dose of a vaccine and about 15% are already fully vaccinated. This is giving companies optimism for the future. The ifo Business Climate Index rose from 96.6 points in April to 99.2 points. At the same time, the euro regained its former strength and is back trading at the level we saw at the beginning of the year of around USD 1.22, while gold benefited from lingering concerns about inflation and gained almost 7% last month. The precious metal is currently trading at just over USD 1,900.

10-year US Treasury yields touched 1.70% and 10-year Bund yields tested the 0% mark, but a short time later, yields fell again slightly and are now around 1.60%, or -0.15%. The verbal interventions of both central banks and the reassurance that tapering is off the table for now seems to have calmed markets, at least for the time being. How sustainable current interest rate levels are in the longer run is, of course, debatable, especially if upcoming labour market figures surprise on the upside. Therefore our positioning remains cautious with a duration of around five years, and we are not taking any major interest risks in light of the fact that interest rates remain very low. Instead, we are at most looking for short-term opportunities in order to benefit from fluctuating interest rates.

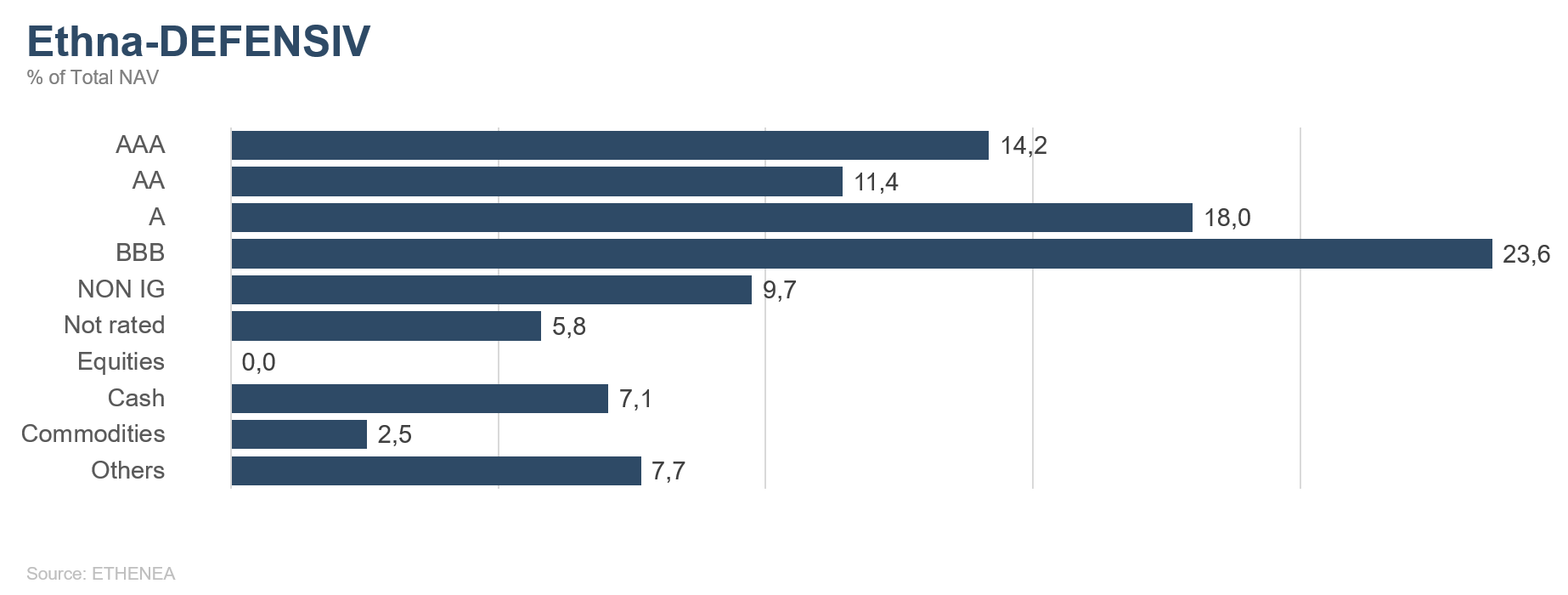

The Ethna-DEFENSIV (T) gained around 0.54% in May. While the bond portfolio benefited from falling sovereign bond yields both in the US and in Europe and from stable spreads, and was the biggest contributor to performance at around 0.42%, equities, to which we are exposed via sustainable ETFs, were only slightly positive for the month. Our gold position, which we opened at 5% at the beginning of the month and have now reduced to around 2.5% for the purpose of profit-taking, made a gratifying 0.33% contribution to performance. Our view that around USD 1,800 would be an attractive re-entry point proved correct. We closed out the yen position. Though it was primarily intended as hedging, the ongoing strength of the euro hit the yen hard. We ultimately further increased the US dollar position to 15%, since, in our opinion, the US dollar is one of the few effective hedges against market turbulence. The performance of the Ethna-DEFENSIV (T) is 0.18% year-to-date, and should move further into positive territory in the coming weeks if sovereign bond yields stabilise further.

Ethna-AKTIV

There was no sign that investors were following the well-known financial-world adage “Sell in May and go away” last month. In fact, equity indices continued to consolidate close to their highs. Amid strong volatility, cryptocurrencies underwent a correction but even that did not seem enough to infect technology securities or the broader market in general. Nor could geopolitical tensions, such as conflict between Israel and the Palestinians, China and Taiwan or due to the forced landing of a plane in Belarus, darken the mood on stock markets, which fundamentally remains buoyant. The high number of “neutrals” in the AAII sentiment survey captures the current mood very nicely, which is also reflected in our positioning. In the current environment, neither the bulls nor the bears are setting the agenda. The fact that the Chinese currency is also trading at a three-year high versus the dollar bolsters our impression that the “risk-on” environment is sustained. Since we assume, looking at equity prices, that the multiple expansion phase has come to an end, further price gains will only be possible if company results improve. At least the prerequisites both on the fiscal and the monetary front are more than well provided. On the subject of monetary policy, with the US labour market well on the way to recouping the losses sustained during the pandemic before the year is out, the debate surrounding inflation and central banks’ response will remain the key issue this summer. At the moment, all central banks except the Canadian central bank are reluctant even to mention the dreaded tapering, even though consumers are experiencing levels of inflation that have not been seen for years in some cases. For example, prices (CPI) in the US rose 4.2% in May, the highest since 2008.

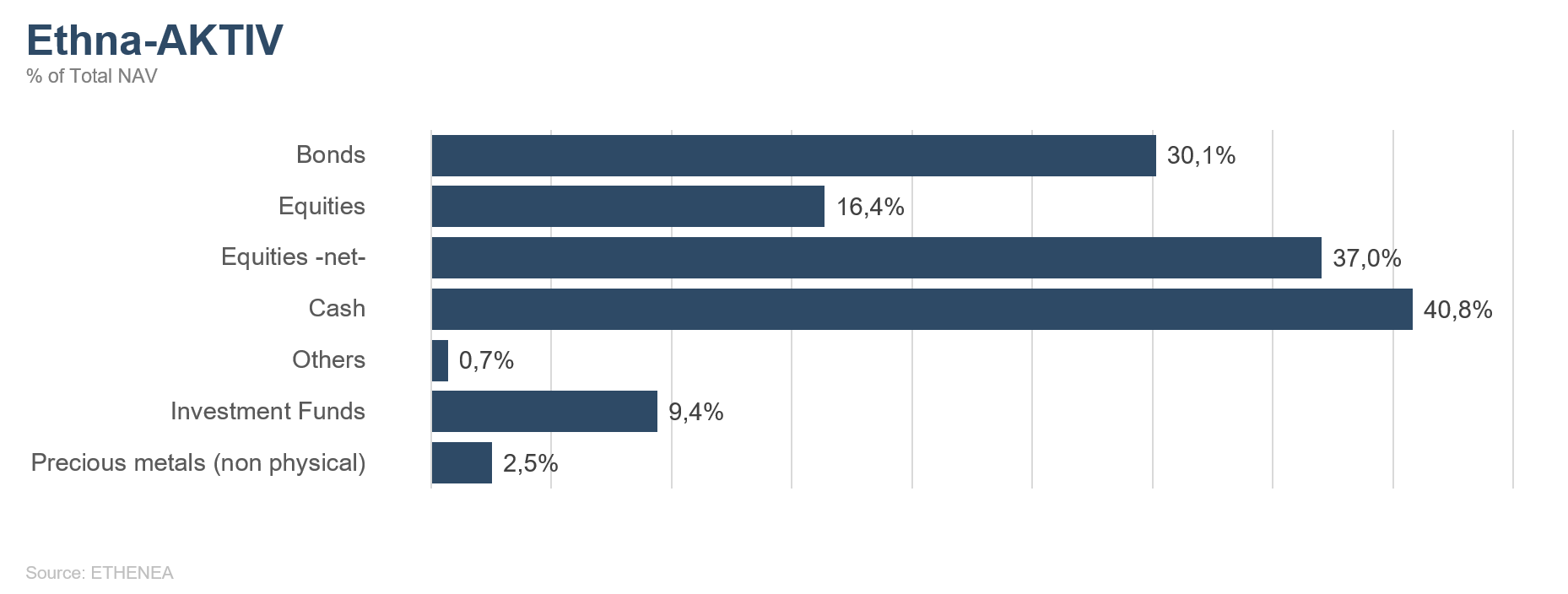

We still think that this second bull market year, coming at the same time as the transition to the mid-cycle stage of what is likely to be a shorter economic cycle, will be volatile but will bring about higher prices towards the end of the year. For this reason, the Ethna-AKTIV’s equity allocation is still above 40%. The much-discussed FX cross hedges are now only in the US dollar. The position in the Japanese yen was closed out as the currency weakened and at the same time as a reduction in the allocation from the maximum of 49%. While we tend to expect further rises in interest rates, especially at the long end of the curve, we are still hesitant to shorten the already relatively low fund duration any more. The reason for this is the high equity exposure, for which we still need the duration as a counterbalance in the event of a crisis. The duration was shortened slightly only via a relatively moderate 4% short position in Italian sovereign bonds. In addition to a potential interest rate rise in all countries, we could see additional widening of spreads in Italy due to its high debt level. It remains to be seen to what extent the ECB will allow this, or rather can curb it at all.

To sum up, the Ethna-AKIV’s flexible management style makes it ideally suited to adapt to changing markets. It’s possible that the ending of the saying “Go away in May...” – “and remember to come back in September” – won’t apply either this year and, contrary to the established seasonal trends, we will see a positive summer we won’t want to miss.

Ethna-DYNAMISCH

After the price gains in previous months, there was a lack of trend in equity markets to some extent in May. While the most recent corporate results season was very positive, the majority of the good news had already been priced into the (in some cases) ambitious valuations. At the same time, a great deal of nervousness is weighing on markets, since we can expect very sharp rises in inflation figures in the coming weeks. This is mainly down to one stand-out basis effect. Both the economy and countless market prices hit rock bottom around a year ago at the height of the pandemic. These are the low comparative figures for the rises we are now seeing. In addition, we are seeing some, in some cases, spectacular shortages at the moment – for instance, in electronic chips and building materials. There is much to suggest that these are temporary price rises, which is also the central banks’ interpretation. But there is ultimately a certain degree of uncertainty about how inflation will develop, particularly since economic activity is forging ahead as we go through the phases of reopening. This, in turn, is feeding into fears about rising interest rates and holds negative implications for equity valuations.

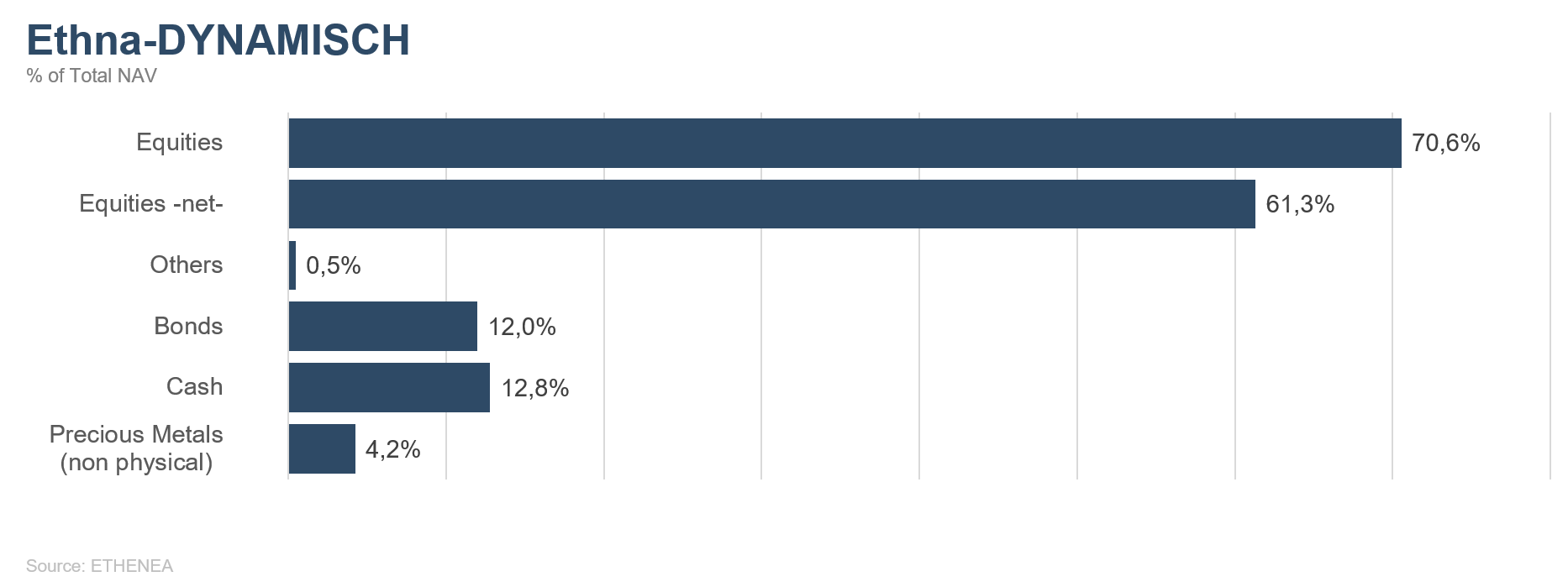

A differential analysis is also required at the moment in areas other than the inflation trend. Upon first glance, the entire capital market environment appears extremely supportive towards equities: (i) the economy is growing, while (ii) enormous fiscal measures are taking effect and (iii) the central banks are continuing with their expansionary monetary policy. This is how things stand at present. The problem is that capital markets look to the future. To put it another way, (i) future economic growth will not be able to match the pace of increases in 2021, (ii) the fiscal packages are enormous but their size is a known fact and (iii) the incremental normalisation of monetary policy is only a matter of time. In short, while many major factors will essentially remain supportive towards equity markets, their magnitude will diminish. This means that we in the Ethna-DYNAMISCH will ease our foot off the accelerator into the summer months. Having successively reduced the equity allocation back in April, we added another hedging component to the portfolio in May (liquid equity index futures) and reduced the net equity allocation from 67% to around 61%. We regard this percentage as appropriate given the risk/reward profile of the markets.

One of the most attractive features of equities is the asymmetry they bring. Set against limited prices losses (“limited” to -100%) is a disproportionately higher return potential, which can far exceed a +100% price gain. As a rule, greater price gains go hand in hand with commensurate fundamental growth in the company. This is easier for smaller companies to achieve than for large industrial conglomerates that operate in saturated markets. With this in mind, in recent months we have been keeping a sharper eye out for fast-growing small- and mid-caps, which complement and round out the Ethna-DYNAMISCH equity portfolio as smaller additions rather than as main components. Here, we target companies that, with their strong products solutions and operations in structural growth markets, have an attractive growth potential. While in the US, many such stocks are (too) expensive, we have been more successful in our search in Europe of late.

In previous Market Commentaries, we mentioned the UK online shop The Hut Group (09/2020) and the UK advertising and marketing service provider S4 Capital (03/2021), which meet these criteria. In recent weeks, three further names with similar characteristics have been added to the portfolio. Back at the end of March we added GK Software, from Germany, to the portfolio, when it completed a capital increase. GK Software offers software solutions for digitalising large retail companies and is increasingly expanding – thanks to established products and partnerships with SAP, Microsoft and IBM – abroad as well. Furthermore, we have built up a 0.5% position each in Apontis Pharma and hGears, both of which completed their IPO in Germany. Apontis Pharma combines the active ingredients of multiple generic products in its “single pill strategy”, thus increasing treatment adherence, which is proven to result in reduced overall costs for health insurers. The industrial company hGears, meanwhile, builds critical drive components for electric motors. Testifying to the strong product quality, one in every two e-bikes sold in Europe in 2020 had gear components from hGears. The company is therefore ideally positioned to benefit from further growth in electric mobility. All of these last three companies mentioned have a market capitalisation of less than EUR 1 billion, making them the smallest companies in the portfolio, numbering 37 equities as of now.

The Ethna-DYNAMISCH product presentation states “Reasonably reducing risks. Seizing opportunities.” The above comments on the latest developments in the portfolio – top-down and bottom-up – flesh out this statement and place it in the context of the current market environment.

HESPER FUND - Global Solutions (*)

On 7 May, the broader US indices, such as the Dow Jones Industrial Average (DJIA) and the S&P 500, reached new highs amid a good earnings season and an increase in commodity prices. Equities then took a breather, as inflation fears and talk that the Fed might start tapering earlier than anticipated started to dominate the market narrative, which, in turn, sparked volatility. By the end of the month, equity markets had recovered, as strong economic data fuelled the rotation to cylicals.

Technology stocks suffered in May while small-caps lagged the broader market. Cryptocurrencies experienced a sharp selloff and incredible fluctuations on the back of criticism for excessive energy consumption, Chinese warnings, and a call from the US Treasury for cryptocurrency transfers of more than USD 10,000 to be reported to the IRS.

For the month, the S&P 500 rose by 0.5% and the DJIA gained 1.9%, while the Nasdaq Composite decreased by 1.5%. The Russell 2000 increased marginally by 0.1%. The Euro Stoxx 50 index climbed 1.6% to an annual high (an increase of 3.3% when calculated in USD), and the Shanghai Shenzhen CSI 300 index jumped 4.1% (5.8% in USD terms).

On the currency front, the USD experienced weakness for second month in a row and the yuan rallied in recent weeks against all major currencies.

As the vaccine rollouts accelerate in most countries, and restrictions are lifted in the US and Europe, the global economy continues to rebound strongly. However, we are seeing supply bottlenecks, such as with chip microprocessors, and prices of industrial commodities have risen sharply, jeopardising the recovery and raising questions for central bankers. The Fed recently reiterated its view that it considers any spike in inflation to be temporary and would need to see more tangible progress towards its policy goals before normalising policy. In addition, the Biden administration has just proposed that Congress increase federal spending to USD 6 trillion in the coming fiscal year. We expect extensive fiscal and monetary stimulus to continue to drive the US recovery.

The HESPER FUND – Global Solutions is sticking with its recovery and reflation trade scenario. In summary, the fund is long equities and short duration.

However, due to market volatility the fund exercised its discipline and reduced almost all of its equity exposure (55% at that time), as stop losses were triggered mid-month. Once market sentiment improved, the fund progressively rebuilt its equity exposure (45%). In the interim, we profited from higher volatility to sell some index put options.

With regard to interest rates, the HESPER FUND – Global Solutions underpinned its view on higher yields, increasing the short on BTPs up to 25% and retaining a 12% short exposure to US Treasuries. Overall, the bond portfolio has a modified duration of -9.3 years (derivatives -13.8 years and corporate bonds 4.5 years).

We have fine-tuned our commodity holdings (10%), reducing industrial metals and buying an ETF that tracks the gold price.

On the currency front, the fund kept its long USD exposure at 18%. We also maintained our 4% exposure to the Norwegian krone as a pure reflation trade.

In May, the performance of the HESPER FUND - Global Solutions EUR T-6 was -0.36%, interrupting six straight months of gains. Year-to-date performance was at 3.69%. Over the last 12 months, the fund has gained 7.13%. Volatility remains stable and low at 7%.

*The HESPER FUND – Global Solutions is currently only authorised for distribution in Germany, Luxembourg, France, and Switzerland.

Figure 1: Portfolio structure* of the Ethna-DEFENSIV

Figure 2: Portfolio structure* of the Ethna-AKTIV

Figure 3: Portfolio structure* of the Ethna-DYNAMISCH

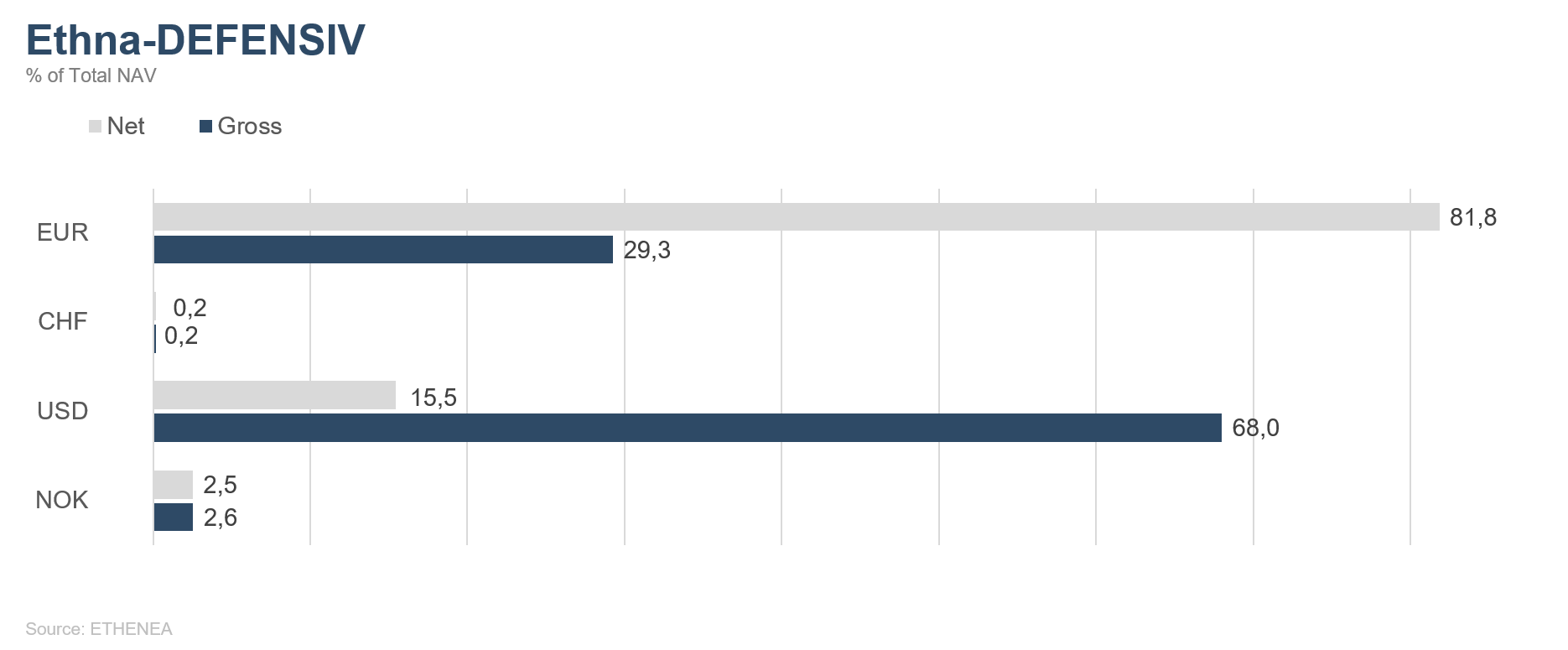

Figure 4: Portfolio composition of the Ethna-DEFENSIV by currency

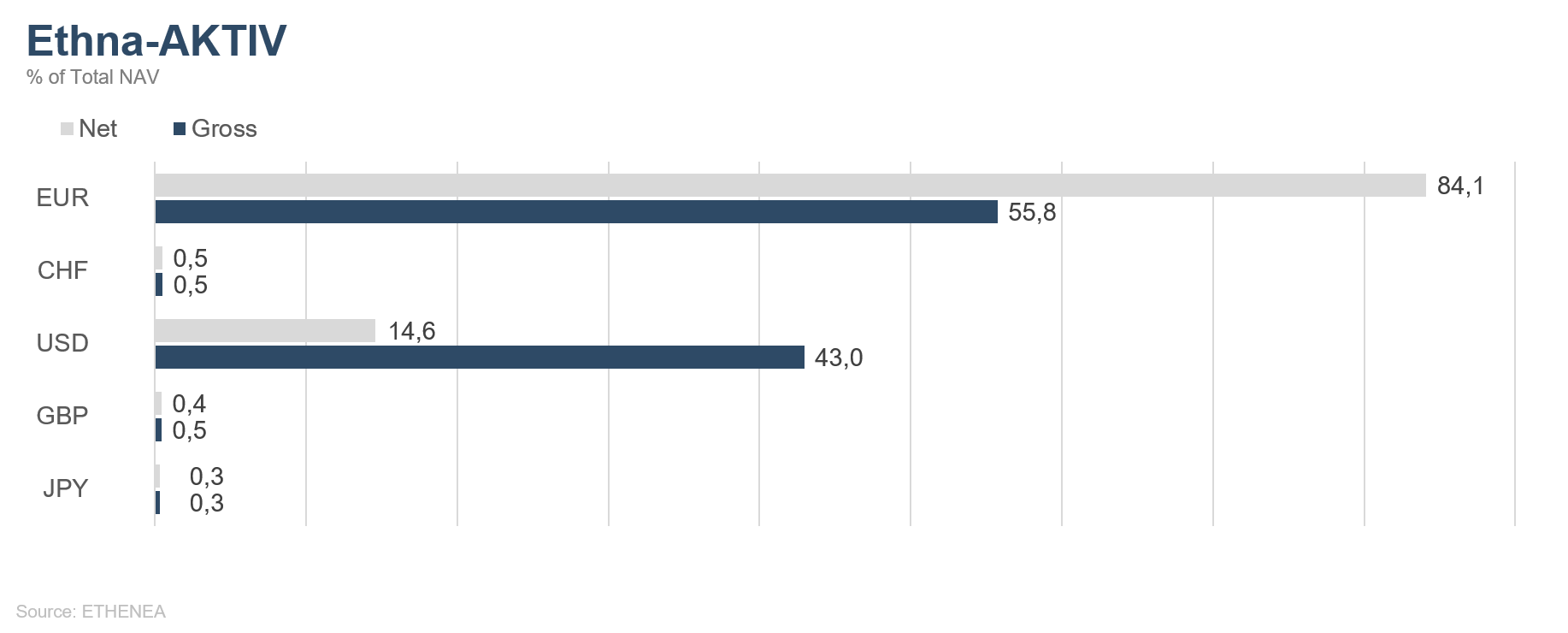

Figure 5: Portfolio composition of the Ethna-AKTIV by currency

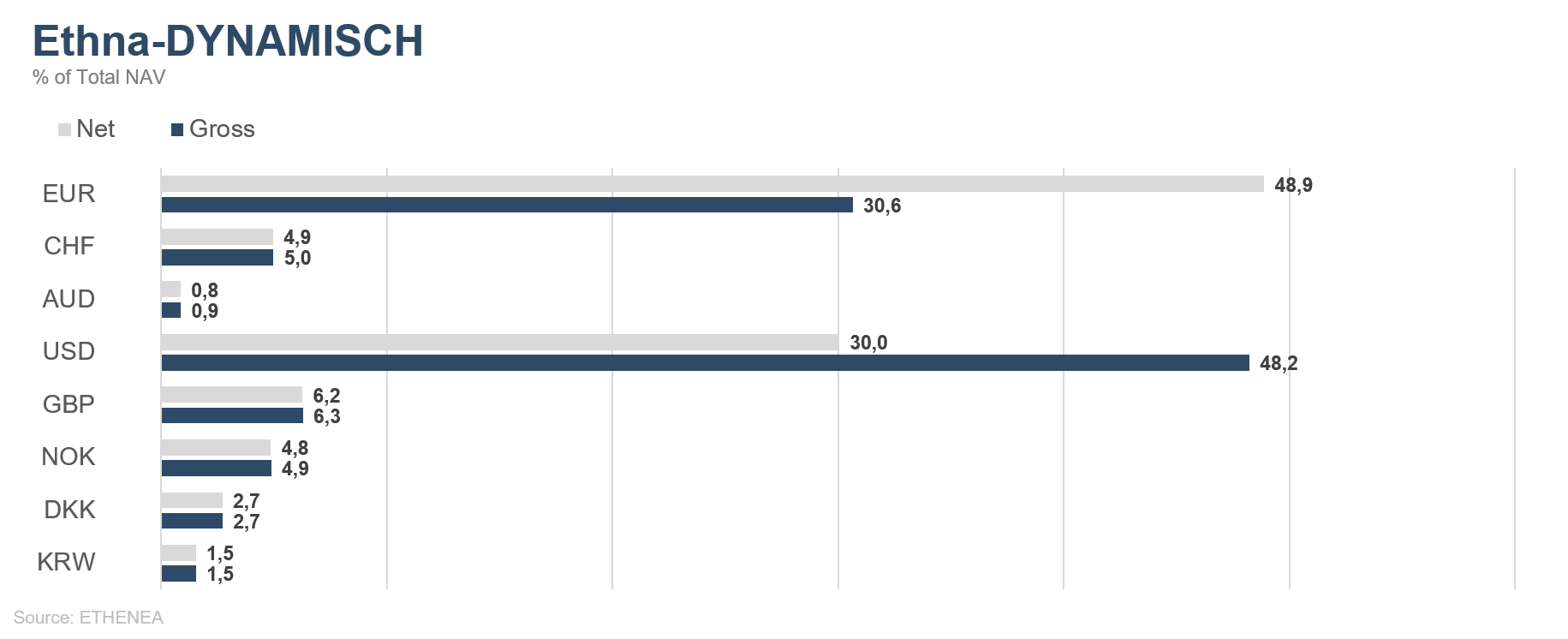

Figure 6: Portfolio composition of the Ethna-DYNAMISCH by currency

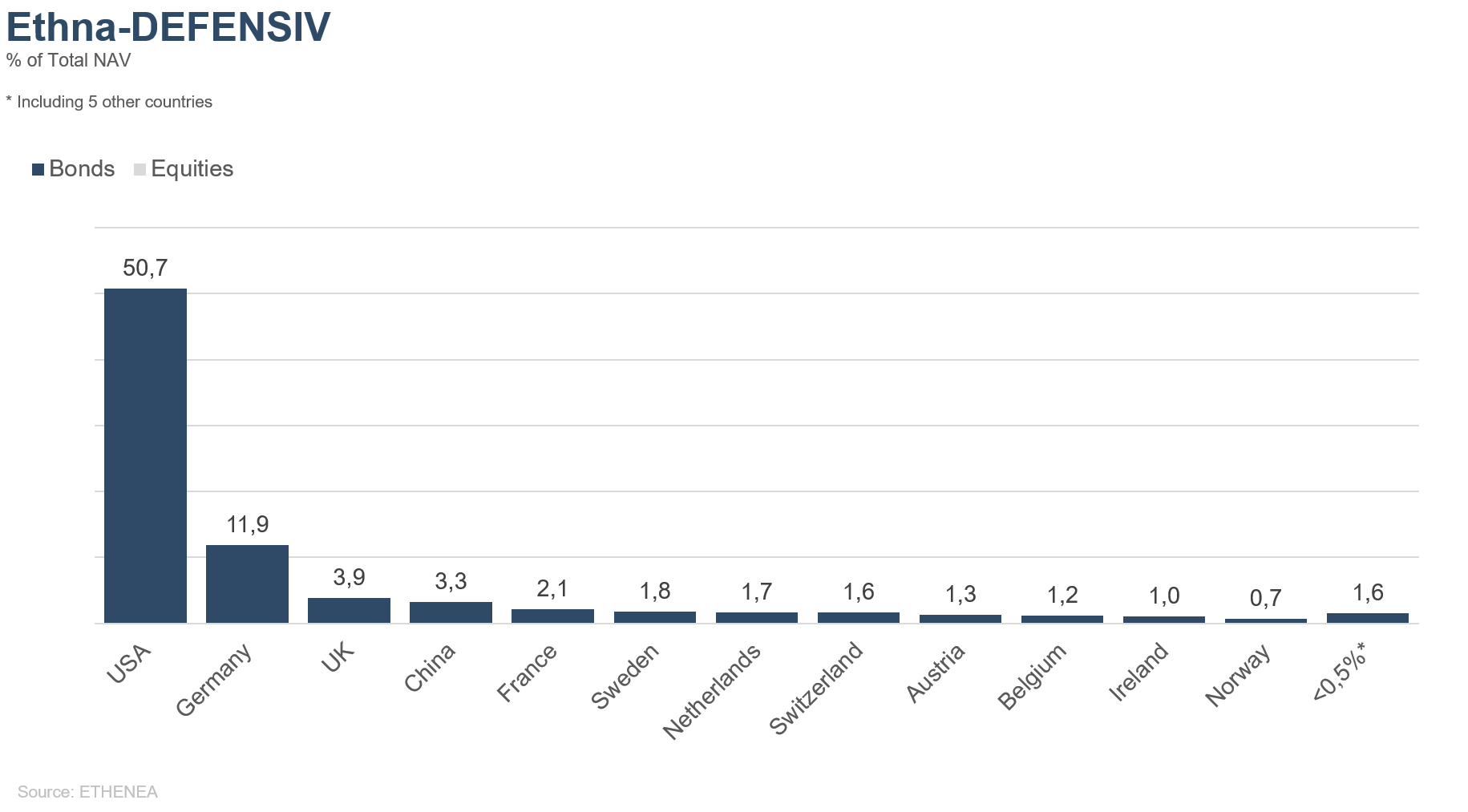

Figure 7: Portfolio composition of the Ethna-DEFENSIV by country

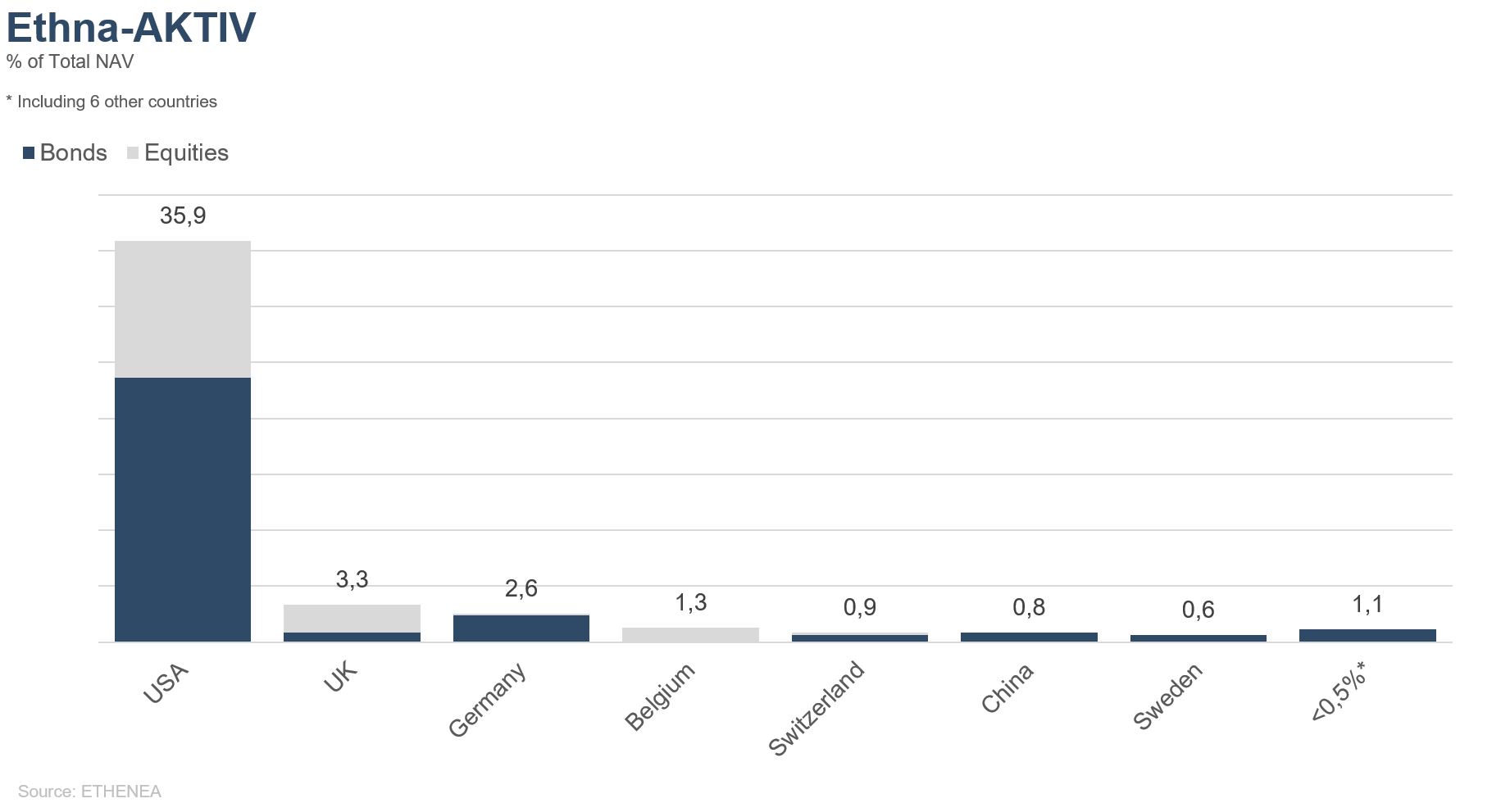

Figure 8: Portfolio composition of the Ethna-AKTIV by country

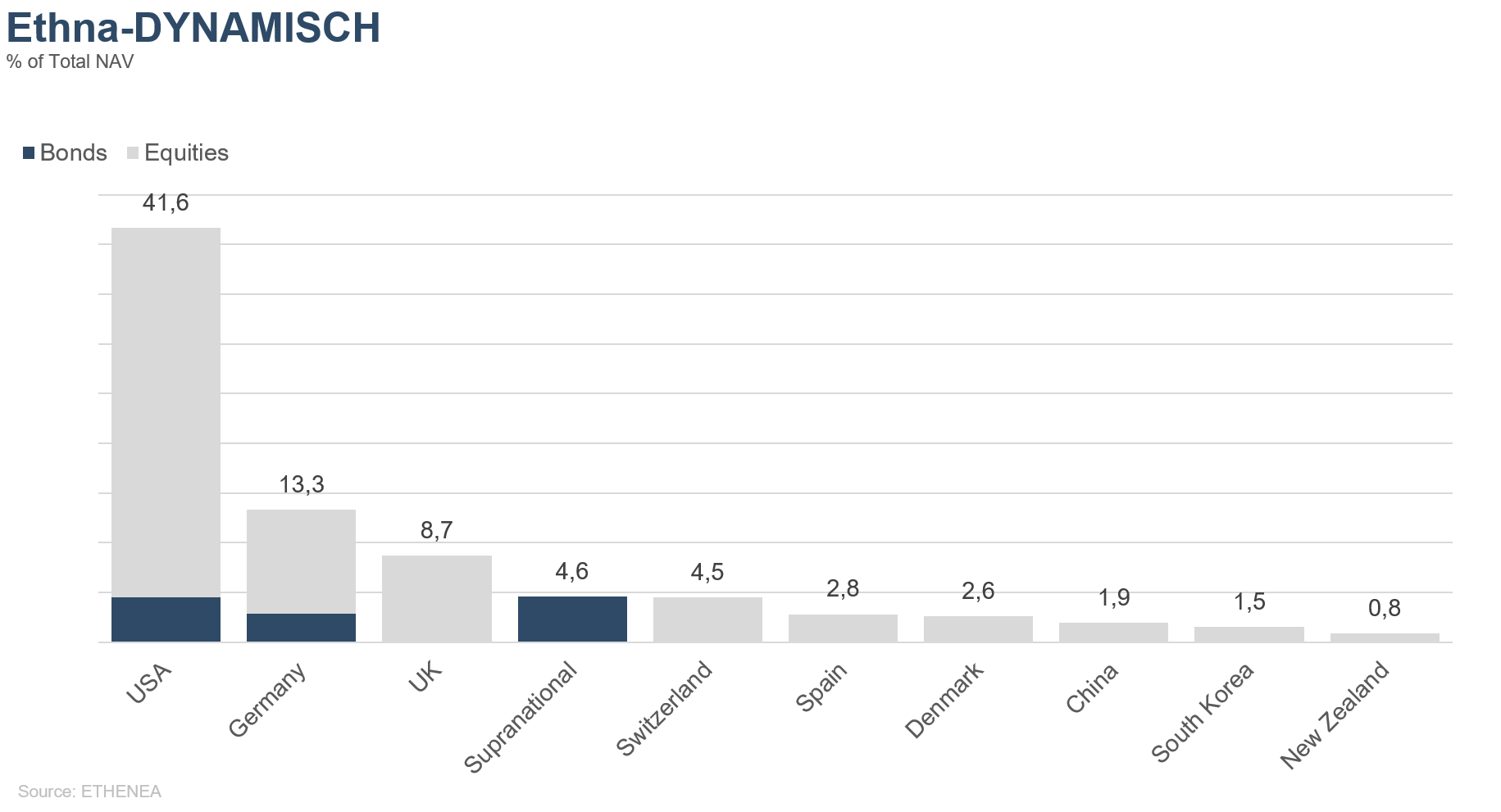

Figure 9: Portfolio composition of the Ethna-DYNAMISCH by country

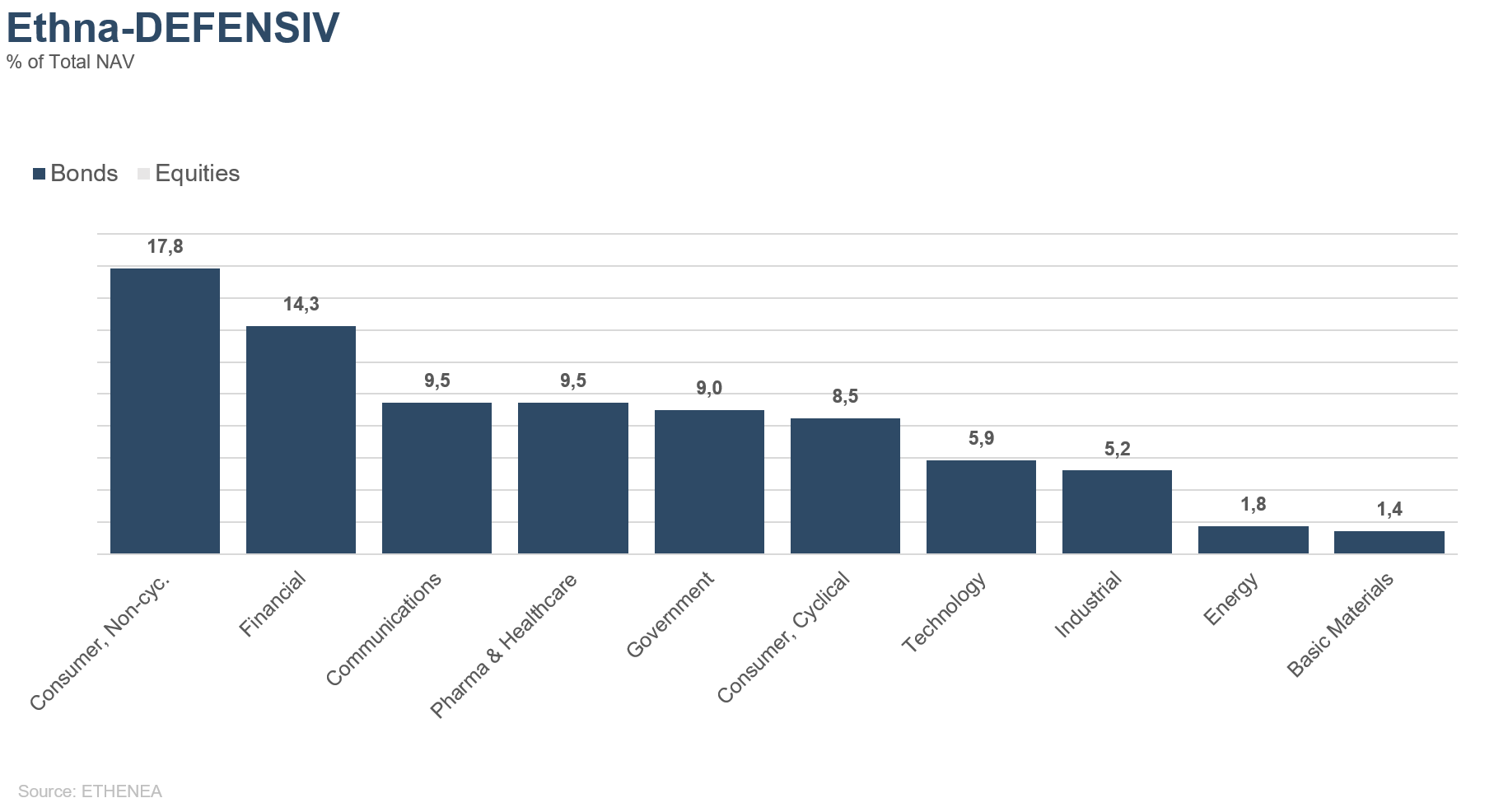

Figure 10: Portfolio composition of the Ethna-DEFENSIV by issuer sector

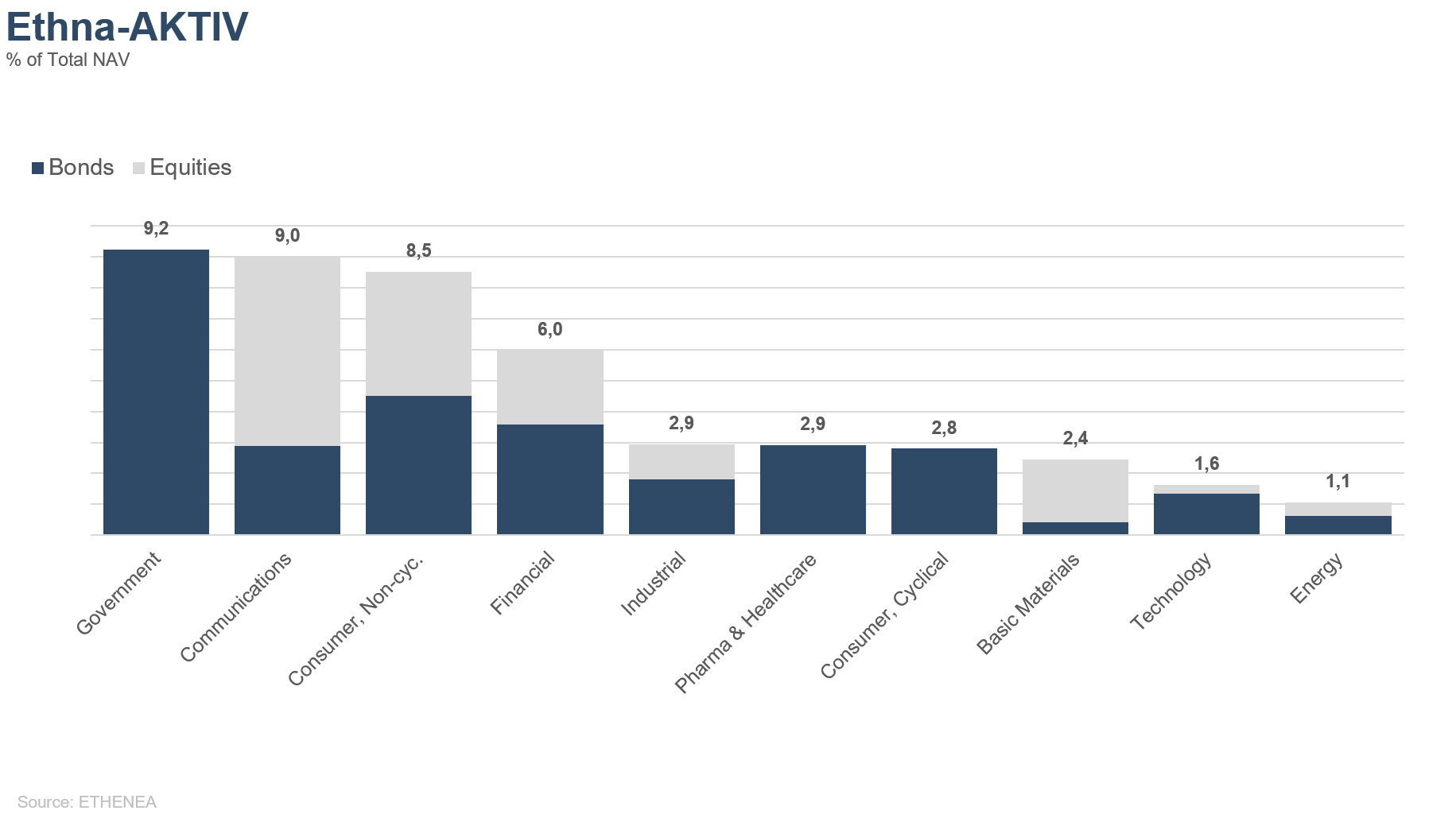

Figure 11: Portfolio composition of the Ethna-AKTIV by issuer sector

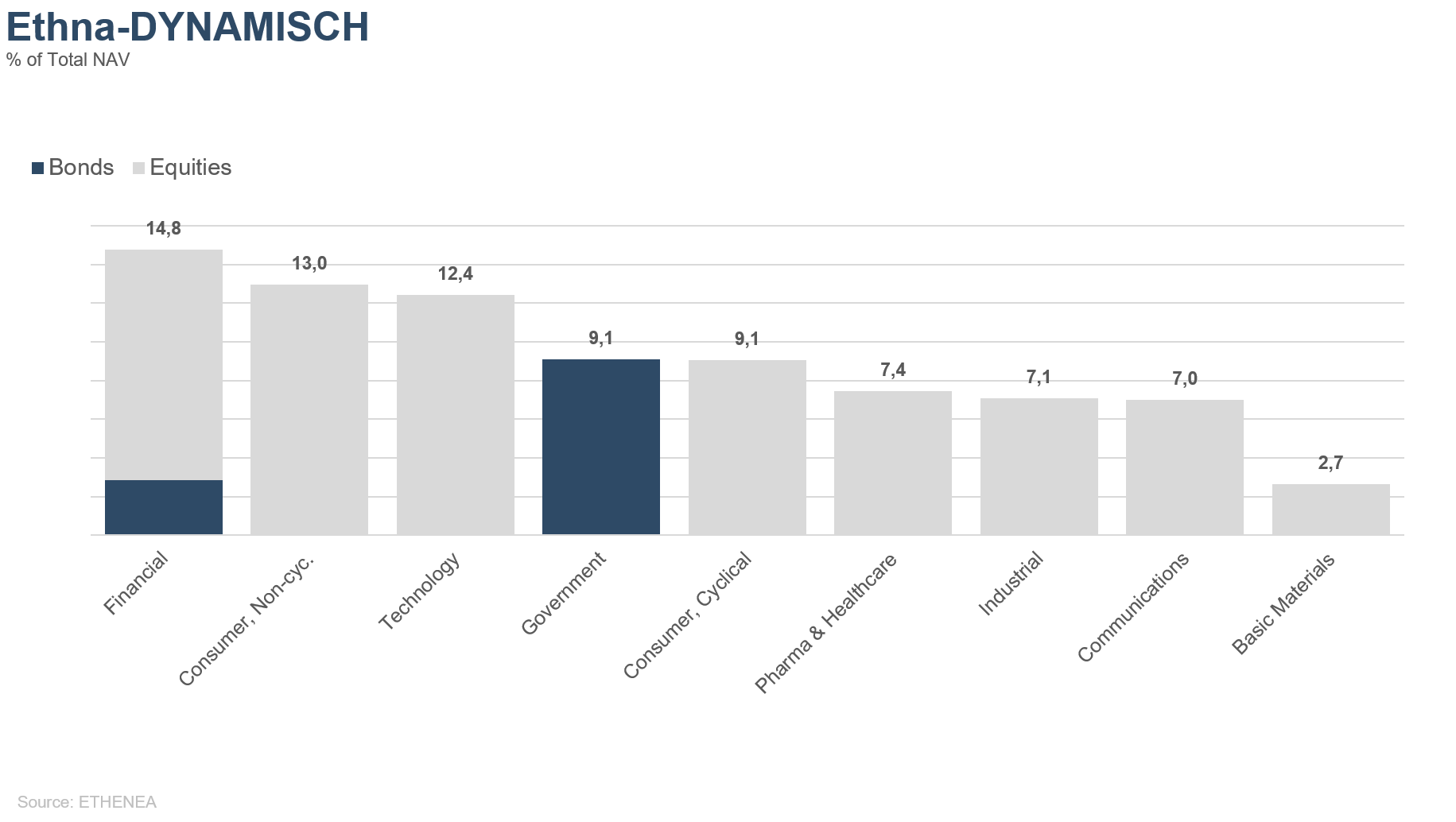

Figure 12: Portfolio composition of the Ethna-DYNAMISCH by issuer sector

* “Cash” comprises term deposits, call money and current accounts/other accounts. “Equities net” comprises direct investments and exposure resulting from equity derivatives.

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

Deze marketingmededeling dient uitsluitend ter informatie. Het mag niet worden doorgegeven aan personen in landen waar het fonds niet voor distributie is toegestaan, met name in de VS of aan Amerikaanse personen. De informatie vormt noch een aanbod noch een uitnodiging tot koop of verkoop van effecten of financiële instrumenten en vervangt geen op de belegger of het product toegesneden advies. Er wordt geen rekening gehouden met de individuele beleggingsdoelstellingen, financiële situatie of bijzondere behoeften van de ontvanger. Lees vóór een beleggingsbeslissing zorgvuldig de geldende verkoopdocumenten (prospectus, essentiële informatiedocumenten/PRIIPs-KIDs, halfjaar- en jaarverslagen). Deze documenten zijn beschikbaar in het Duits en als niet-officiële vertaling bij ETHENEA Independent Investors S.A., de bewaarbank, de nationale betaal- of informatiekantoren en op www.ethenea.com. De belangrijkste vaktermen vindt u in de lexicon op www.ethenea.com/lexicon/. Uitgebreide informatie over kansen en risico's van onze producten vindt u in het actuele prospectus. In het verleden behaalde resultaten bieden geen betrouwbare indicatie voor toekomstige prestaties. Prijzen, waarden en opbrengsten kunnen stijgen of dalen en kunnen leiden tot volledig verlies van het geïnvesteerde kapitaal. Beleggingen in vreemde valuta zijn onderhevig aan extra valutarisico's. Aan de verstrekte informatie kunnen geen bindende toezeggingen of garanties voor toekomstige resultaten worden ontleend. Aannames en inhoud kunnen zonder voorafgaande kennisgeving worden gewijzigd. De samenstelling van de portefeuille kan op elk moment wijzigen. Dit document vormt geen volledige risico-informatie. De distributie van het product kan vergoedingen opleveren voor de beheermaatschappij, verbonden ondernemingen of distributiepartners. De informatie over vergoedingen en kosten in het actuele prospectus is doorslaggevend. Een lijst van nationale betaal- en informatiekantoren, een samenvatting van de beleggersrechten en informatie over de risico's van een foutieve netto-inventariswaarde-berekening vindt u op www.ethenea.com/juridische-opmerkingen/.In geval van een foutieve NIW-berekening wordt compensatie verleend volgens CSSF-circulaire 24/856; bij via financiële intermediairs aangeschafte participaties kan de compensatie beperkt zijn. Informatie voor beleggers in Zwitserland: Het land van herkomst van de collectieve belegging is Luxemburg. De vertegenwoordiger in Zwitserland is IPConcept (Schweiz) AG, Bellerivestrasse 36, CH-8008 Zürich. De betaalagent in Zwitserland is DZ PRIVATBANK (Schweiz) AG, Bellerivestrasse 36, CH-8008 Zürich. Prospectus, essentiële informatiedocumenten (PRIIPs-KIDs), statuten en de jaar- en halfjaarverslagen zijn gratis verkrijgbaar bij de vertegenwoordiger. Informatie voor beleggers in België: Het prospectus, de essentiële informatiedocumenten (PRIIPs-KIDs), de jaarverslagen en de halfjaarverslagen van het subfonds zijn op verzoek gratis in het Duits verkrijgbaar bij ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxemburg en bij de vertegenwoordiger: DZ PRIVATBANK AG, Niederlassung Luxemburg, 4, rue Thomas Edison, L-1445 Strassen, Luxemburg. Ondanks de grootst mogelijke zorg wordt geen garantie gegeven voor de juistheid, volledigheid of actualiteit van de informatie. Alleen de originele Duitstalige documenten zijn juridisch bindend; vertalingen dienen alleen ter informatie. Het gebruik van digitale advertentieformaten is op eigen risico; de beheermaatschappij aanvaardt geen aansprakelijkheid voor technische storingen of schendingen van gegevensbescherming door externe informatieaanbieders. Het gebruik is alleen toegestaan in landen waar dit wettelijk is toegestaan. Alle inhoud is auteursrechtelijk beschermd. Elke reproductie, verspreiding of publicatie, geheel of gedeeltelijk, is alleen toegestaan met voorafgaande schriftelijke toestemming van de beheermaatschappij. Copyright © ETHENEA Independent Investors S.A. (2026). Alle rechten voorbehouden. 02-06-2021