Stagflation – back to the 1970s?

Last year, the outbreak of the Covid-19 pandemic rocked the global economy. A simultaneous negative supply and demand shock triggered a collapse in worldwide aggregate demand, reduced economic activity to a minimum, and disrupted major supply chains. Then the rapid and unprecedented monetary and fiscal policy response, together with the roll-out of effective vaccines, propelled a powerful economic recovery driven by the rebound of aggregate demand.

The strong pick-up in economic activity, accompanied by rising energy prices and supply shortages, has fuelled the acceleration of inflationary pressures on a global scale. The price of oil has surged to a seven-year high and natural gas costs have risen more than 500% in Europe. After the strong rebound of the first half of 2021, the global economy is now losing momentum. The appearance of new Covid-19 variants, fading policy support, inflationary pressures, and the deceleration of the Chinese economy are among the main uncertainties threatening the economic outlook.

The combination of slow growth and inflationary pressures is both concerning and particularly challenging for policymakers. Recently, there have been suggestions that the global economy may soon enter a period of stagflation, similar to the one experienced in the 1970s.

What is stagflation?

Stagflation is defined as a period of high inflation rates accompanied by sluggish economic growth and steadily high unemployment. In the worst cases, stagflation can also mean a period of inflation combined with a decline in gross domestic product (GDP).

The main theories on the origin of stagflation suggest that it arises from supply shocks, from poor economic policies, or from a combination of both. Sudden disruptions in the supply of a commodity can result in a rapid increase not only of its price but also the general price level. The price surge makes production more expensive and less profitable, thereby slowing economic growth. Stagflation can also occur as a result of poor economic policies implemented in response to a surge in inflation. These then exacerbate the economic contraction or the inflationary pressures.

Stagflation is particularly challenging for policymakers, as most measures to lower inflation may have a detrimental impact on output and increase unemployment levels, whiles policies designed to decrease unemployment may make inflation worse. However, stagflation is a rare phenomenon, as weak demand tends to drive prices down, which means that a self-correcting mechanism should mitigate the duration of the recessionary period.

When discussing stagflation, it is useful to understand that there are two types of inflation. Demand-pull inflation is the increase in prices as a result of macroeconomic policies. This is usually the result of central banks cutting interest rates or governments increasing spending or cutting taxes. These policies produce an increase in aggregate demand that goes beyond the economy’s productive capacity. On the other hand, cost-push inflation is the result of supply shortages and disruptions that mainly originate in the food and energy markets. Cost-push inflation impacts retail prices through the production chain. Monetary policy tends to have little impact on curbing it, as tighter policies would not help to restore supply. Instead they risk exacerbating the negative effects of inflation by reducing aggregate demand.

The stagflation of the 1970s

The ‘Great Inflation’ and the stagflation of the 1970s were the result of a unique series of historical events and policy missteps:

1) The painful memories of the economic depression of the 1930s, created a policy environment in the 1960s and the 1970s dominated by the pursuit of full employment. The Keynesian stabilisation policies emphasised a stable and long-term trade-off between damaging unemployment and inflation, where the latter was considered a mere inconvenience. It was believed that lower rates of unemployment could be permanently achieved with modestly higher rates of inflation. Motivated by the mandate of full employment, the Federal Reserve accommodated large and rising fiscal imbalances. The Fed policies accelerated the expansion of money supply and increased overall prices without reducing unemployment.

2) During the late 1960s and the early 1970s, the US economy was characterised by growing budget and current account deficits. President Johnson’s ‘Great Society’ legislation introduced major spending programmes for a number of social initiatives, including Medicare and Medicaid. The US fiscal situation was also severely strained by the country’s involvement in the Vietnam war. In 1968, Lyndon Johnson’s fiscal policies boosted economic growth to 4.9% but, coupled with a complacent Federal Reserve, this led to a disturbing annual inflation rate of 4.7%.

3) President Nixon’s policies (1969 - 1974) contributed to weakening growth and increasing price pressures. To counteract the mild inflation generated by President Johnson’s policies, he imposed damaging wage-price controls, which had negative effects on aggregate demand and squeezed businesses margins. The US economy, which was already suffering from a loss of competitiveness, went into a severe recession between 1973 and 1975. By ending the convertibility of the US dollar (USD) into gold, President Nixon also contributed to the collapse of Bretton-Woods - a system of fixed exchange rate parities that provided a solid anchor to the post-war Federal Reserve policies. The decision to unpeg the USD from gold removed the Fed’s policy anchor and, combined with expansionary policies aimed at reducing unemployment, contributed to inflation swelling to above 12% in 1974.

4) The energy crises, which are typically blamed for causing the US recession, were actually an aggravating factor that contributed to the deterioration of an economy already severely damaged by recession. First came the OPEC oil embargo in 1973, during which oil prices quadrupled. Then in 1979, we saw the second energy crisis in the aftermath of the Iranian revolution, during which the oil price tripled. The oil shocks of the 1970s contributed to cost-push inflation that reached a peak of 14.8% in 1980.

Back to the 1970s?

There is no doubt that the current environment of slowing growth and stubbornly high inflation poses both significant risks to global growth and a challenge for policymakers. Persistent high inflation may lead to tighter financial conditions and weaker growth momentum by constraining production and denting consumer confidence. However, an unwarranted pre-emptive policy tightening could derail economic recovery, while having little effect on containing cost-push inflationary pressures.

Although the challenges of the current environment cannot be dismissed, persistent high inflation should be seen as a tail risk. The current situation appears to be quite different from the situation in the 1970s in several respects.

Timing perspective

The timing and sequencing of the events of the Covid-19 crisis differ markedly from the recessions of the 1970s and 1980s. In 2020, the Covid-19 shock hit inflation and growth, both of which collapsed simultaneously and abruptly. The unprecedented policy response prevented a global depression and produced a very unusual and rapid global recovery. Yet the strong rebound in aggregate demand could not be matched by an impaired supply and the global economy is now going through a delicate adjustment period. However, economic growth is solid and unemployment rates are approaching their pre-pandemic levels. Despite the recent downgrade revisions, analysts point out that growth rates in 2021 and 2022 will be solid and will outpace the trend growth of the recent past.

Monetary policy

The Fed’s dovish policies and a lack of a clear anchor for its policy framework contributed to the loss of credibility that caused the Great Inflation of the 1970s. Credibility loss can be very costly, and the deep recession of the early 1980s was associated with policies adopted to control inflation and restore the Fed’s credibility.

Since the early 1990s, central bank independence and the progressive adoption of the inflation targeting framework have greatly enhanced the credentials of central banks in terms of fighting inflation. Together, anchoring monetary policy to an inflation targeting objective and the central bank policies of the last 30 years have been key to both ensuring central banks’ credibility and taming inflationary pressures.

Origin of inflationary pressures

The stagflation of the 1970s was the result of a unique combination of policy missteps, dovish Federal Reserve policies, and a historic change of the international monetary system, accompanied by two severe oil shocks. While inflationary pressures are not homogeneous across countries, recent inflation drivers reflect the strong pick-up in economic activity, rising energy prices, and unusual pandemic-related mismatches between demand and supply that are likely to be temporary.

Input shortages and supply chain disruptions should progressively level out as progress is made in combatting the pandemic and higher prices spur investments in production capacity. High energy prices should also be short-lived. The world can produce sufficient energy and, when prices become high enough, new supply from US shale producers and other non-OPEC members flood the market. Over time, energy transition and the rise of renewable energies will also help to dampen the increase in energy prices.

For the time being, there is also little evidence that the current inflationary pressures are generating second-round effects and feeding into generalised salary increases. Salary increases are primarily concentrated in the pandemic-affected sectors and mainly impact low-wage earners. Automation is replacing labour at a rapid pace and the current labour shortage could even force companies to speed up the automation process.

In the short term, there are many uncertainties about inflationary development, but overall there are few signs of a repeat of the Great Inflation of the 1970s. Overall, the current situation does not point to a change in the long-term inflation dynamics. Structural forces, such as demographics, technology, rising inequality, and globalisation are likely to maintain disinflationary pressures over the longer term.

There are still risks to consider

While a repeat of the stagflation of the 1970s seems unlikely, the current environment still presents a number of risks that should not be underestimated.

Inflation risks are skewed to the upside and could materialise if supply-demand mismatches continue for longer than expected. Persistently higher inflation may derail the recovery by constraining production or denting consumer confidence. Moreover, the longer the supply disruption persists, the greater the risk that it will translate into second round effects and generalised inflation. Rising inflation expectations could lead to a faster-than-anticipated monetary normalisation in advanced economies, which could also derail the economic recovery.

Policymakers will have to walk a fine line between patient support for the economic recovery and a willingness to act quickly to curb any potential entrenched inflationary pressures. It will be particularly important to avoid de-anchoring medium-term inflationary expectations and prevent an inflationary spiral that would require abrupt policy tightening. Should current inflationary pressures generate persistent second-round effects that trigger wage increases, central banks will need to act decisively and tighten their policies.

Portfolio Manager Update & Fondspositionierung

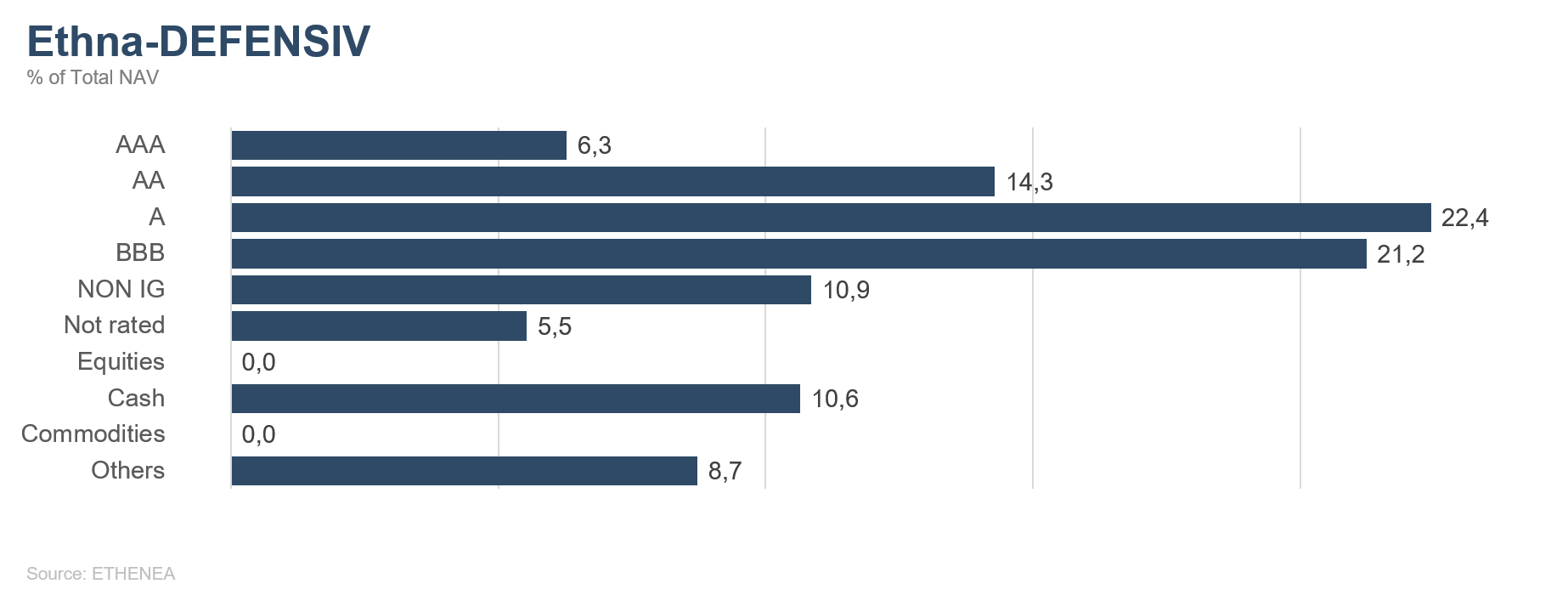

Ethna-DEFENSIV

“I do think it's time to taper; I don't think it's time to raise rates.” This statement from Jerome Powell in October again made it clear what monetary course the Fed will take. In all likelihood, the U.S. central bank will officially announce the tapering of its monthly sovereign bond purchases on 3 November, which currently stand at USD 120 billion. At the same time, Mr Powell has stressed repeatedly that it is too soon to raise interest rates. The market takes a somewhat different view. Eurodollar futures have already priced in three rate hikes for September 2022 and two more for 2023, to 1.5% at that point.

In the euro zone too, investors are sticking to their guns that the ECB will raise interest rates at least once next year due to sustained inflationary pressure. This would mean a radical change away from ultra-accommodative monetary policy, but we believe this is extremely unlikely. The pandemic emergency purchase programme (PEPP) officially ends in March 2022, and the ECB will probably let it peter out beyond March, perhaps in the form of PEPP bridge financing or a top-up of the regular asset purchase programme (APP) before raising interest rates for the first time in 2023 at the earliest. However, there remains the negative scenario where inflation is much higher than expected, which would force the ECB to raise interest rates early.

It remains to be seen whether the market or the central banks will be proven right. One thing for certain is that the high rates of inflation, and in particular the higher costs of intermediate products and energy, will continue to pose a challenge for some companies. Not since 1981 have the prices of imported goods into Germany been so high as in October; timber and steel in particular have soared. This puts pressure on margins and creates headaches especially for companies that operate in highly competitive markets and cannot easily pass on higher prices to customers. Within the Ethna-DEFENSIV, therefore, we continue to invest in well-capitalised companies that, given their position in the market, are well able to translate higher raw material prices into higher prices for their products and get through dry spells caused by supply shortages without any problems.

Given the ongoing uncertainty in bond markets and the slightly increased yields in October (10-year Bunds went from -0.20% to -0.10% and U.S. Treasuries went from 1.49% to 1.60%), the Ethna-DEFENSIV retained its strategy of keeping duration below 2. Hedging in the form of futures absorbed the higher yields in euro and U.S. dollar to some extent. We also retained the equity allocation of 10%, which contributed 0.43% to performance. Having reduced the gold position in September, we completely closed it last month, since the trend of rising yields is putting pressure on the precious metal. Overall, the Ethna-DEFENSIV (T class) produced a slightly negative performance of -0.12% in October, which, given the higher yields, is quite a respectable result for a defensive balanced fund like the Ethna-DEFENSIV. Therefore, the fund is up 1.08% year-to-date.

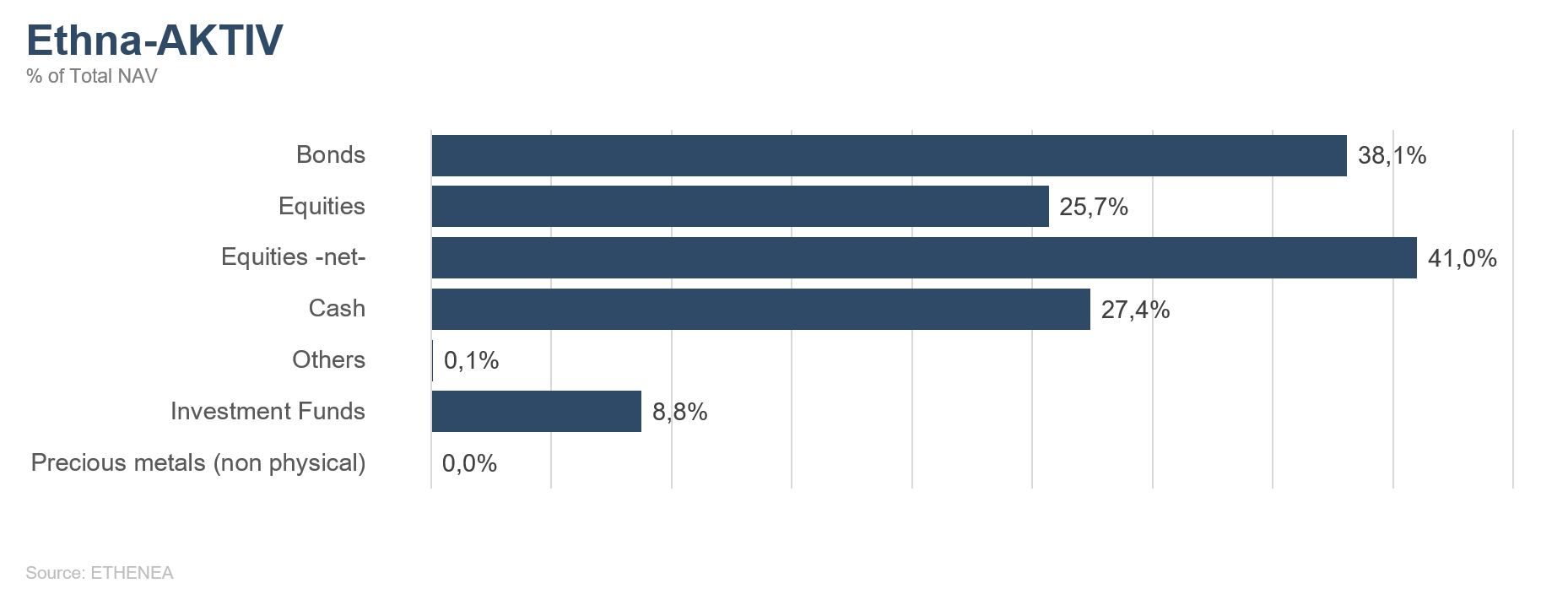

Ethna-AKTIV

Given the ongoing supply shortages, which now affect much more than just electronic chips, the current reporting season was eagerly anticipated. The most pressing question was whether the ambitious growth expectations, both for revenue and earnings, could be met. Approximately half of companies on both sides of the Atlantic had published their figures by month-end. While surprising, this figure was not as big compared to the previous quarter, and analysts’ expectations for revenue and earnings were beaten by more than 10%, which is still outstanding historically. So it’s no wonder that the MSCI World, the broadest global equity index, climbed to new all-time highs in October, driven particularly by the U.S. leading indices, after a weak September. Our belief, as stated in last month’s Market Commentary, that the correction in prices we were seeing was temporary and wouldn’t lead to a lasting trend reversal, has borne out so far. Despite the known challenges, the fundamentals are simply still too good. Nor could the further slow rise in global interest rates dampen the positive mood on the equity market. We expect this trend to continue. Even though we are confident that expectations of high inflation will push interest rates upwards, we do not expect a massive overshooting in interest rates. This view is supported by the rhetoric from the European Central Bank, among others, which indicated no change in its monetary policy during its latest meeting. Central bankers at the U.S. Federal Reserve, who will meet at the beginning of November, also made it very clear in the lead-up that the start of tapering will not involve imminent interest rate hikes. We expect growth figures to stabilise at a low level, and thus an ongoing reflationary environment. Given the comprehensive economic packages, both already in place and in the pipeline, we believe the present concern about stagflation to be overblown. On the whole, this points to a continuation of the risk-on phase, which will increasingly come down to the selection of the sectors that benefit and also individual securities, especially in equities.

What this consequently means for the positioning of the Ethna-AKTIV is adhering to the historically high equity allocation, which was increased to the maximum level of 49% in the period of weakness. Because we remain confident of the market position and potential for growth of U.S. companies, the U.S. accounts for most of our equity exposure. By gradually switching from investment in futures to individual securities, not only are we following our own selection rationale, but we have also managed to reduce the cash allocation to less than 30%. We are striving to reduce this percentage to less than 20% in the coming weeks. As announced a month ago, we expanded the U.S. dollar allocation to above 40%. Despite the bull markets, the strength of the U.S. dollar was very noteworthy. We see this is a sign of the relative strength of the currency. On the bond front, we barely had to make any changes as we consider the fixed-income portfolio to be well positioned in relation to both quantity and quality in this environment. We have rightly continued to reduce the duration. Only a few sovereign bonds were added, which also helped to reduce the cash allocation.

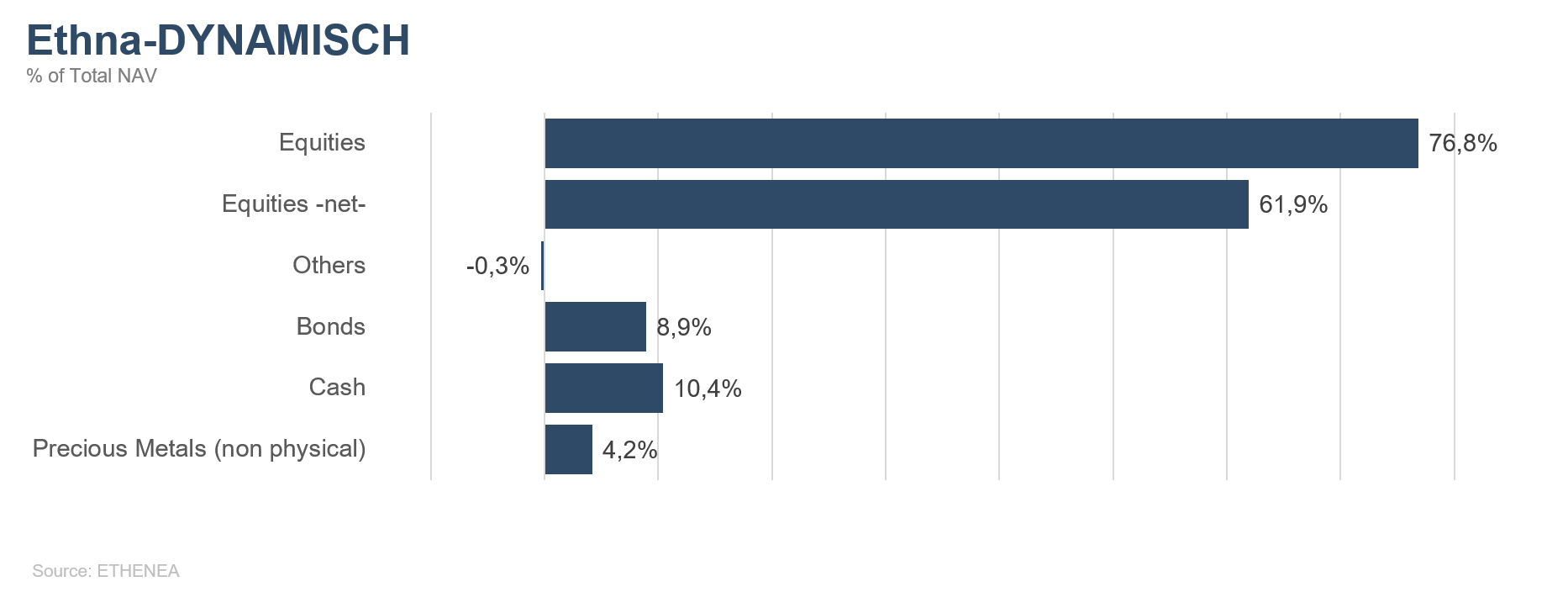

Ethna-DYNAMISCH

Towards the end of the month, a good 50% of S&P 500 companies had reported their third quarter results. This halfway point in the reporting season gives us a good opportunity to take stock: what we are seeing is a mixed picture. On the one hand, the majority of companies have exceeded analysts’ consensus estimates, in terms of both revenue and earnings, in some cases by a clear margin. However, the immediate market reaction – as measured by price movements within a day of results being published – is extremely low, at an average of 0.01%. The European STOXX Europe 600 index paints a similar picture.

One reason for this apparent discrepancy is the high degree of forecast uncertainty inherent in the current quarter. After the very high growth in the second quarter, company growth rates are normalising. This process of normalisation is relatively hard to predict. Global supply chain problems and inflationary pressure are additional uncertainty factors. Analysts’ wide range of expectations for fundamental revenue and earnings performance shows that they are finding it difficult to deal with this complex set of factors. There is even little consensus in relation to companies that are not directly affected by the consequences of the supply chain issues. Take Google’s parent company Alphabet Inc. for example: there was a difference of almost 15% between the most optimistic and the most pessimistic estimate for revenue – the biggest difference of opinion in more than a decade. The range is so wide that the consensus estimate – a proxy for the average expectation of the market as a whole – loses some of its relevance. Moreover, market expectations as a whole can also diverge from the analysts’ consensus estimate and anticipate a surprise positive quarterly report. In determining how the price reacts after publication of quarterly results, the outlook also plays an important, generally more decisive role. The supply chain problems in particular are a factor in many companies issuing a conservative outlook for business performance in coming quarters and prevent excessive euphoria. For this and other reasons, bearing in mind a hard-to-predict reporting season, we reduced the net equity allocation to almost 60% at the beginning of October.

So what’s next? It’s clear that the supply chain problems and the resulting price rises will subside. What is less clear is when this will happen. Against this backdrop, the Ethna-DYNAMISCH’s focus on quality companies helps. The stocks in our portfolio occupy a position in the market that enables them to pass on or absorb price rises. They also have the flexibility to react to dynamic procurement markets. The current reporting season confirms this. For that reason, the composition of the Ethna-DYNAMISCH did not change significantly in October. As such, even in the current market environment, we offer risk-controlled access to equity markets.

HESPER FUND - Global Solutions (*)

In October, the combination of slowing economic momentum and stubbornly high inflation not only became the primary concern for markets but also put central banks in the spotlight. Rapidly rising inflation triggered a sell-off in local debt markets, pushing up yields. Many of the central banks in emerging markets, along with a few of the smaller central banks in advanced economies, started hiking interest rates. Markets are now challenging the view held by the major central banks that the current inflationary spike is only transitory. There is a particularly high degree of uncertainty about the future path of inflation. Unwinding the unprecedented policy stimulus is a delicate process and policy missteps are a risk that should not be underestimated.

Although growth concerns dampened market sentiment in September and at the beginning of October, the surprisingly positive earnings season came to the rescue, with stocks first recovering then rising to new highs. Despite the initial volatility, October turned out to be an excellent month for equities, as most broad indices posted strong gains. This strength was underpinned by the fact that profit margins held up quite well in the third-quarter results, despite soaring commodity prices and supply chain disruptions. Many companies have been able to pass rising costs on to consumers, with more than 80% of them beating Wall Street’s earnings estimates.

In October, the major US stock indices rebounded to close the month at new all-time highs. For the month, the S&P 500 rose by 6.9%, the Dow Jones Industrial Average (DIJA) went up by 5.8% and the Nasdaq Composite increased by 7.3%. Conversely, small-caps, as measured by the Russell 2000 Index, gained 4.2% but remained below their mid-March highs.

In Europe, the Euro Stoxx 50 Index rose by 5% (an increase of 4.7% when calculated in USD) while in the UK, the FTSE 100 gained 2.1% (+3.7% in USD). Despite a strong Swiss franc, the Swiss Market Index performed very well, rising by 4% (+6% in dollar terms) over the month.

Asian markets lagged, with the Shanghai Shenzhen CSI 300 Index gaining 0.9% (+1.8% in USD terms). The Hang Seng Index in Hong Kong rebounded by 3.3%. In Japan, the blue-chip Nikkei 225 lost 1.9% (-3.7% in USD terms).

The HESPER FUND – Global Solutions continues to operate under the scenario of solid global growth supported by accommodative monetary and fiscal policies and vaccination rollouts. However, headwinds, such as skyrocketing energy costs and supply chain bottlenecks, forced us to take a more cautious stance and dynamically adapt our portfolio.

As volatility rose, the fund reduced its long equity exposure significantly at the beginning of the month. By the middle of October, the HESPER FUND – Global Solutions started to gradually increase its equity allocation, ending the month with a 48% net exposure. The fund kept its high-yield bond exposure but completely hedged the duration to protect performance from the volatility in bond yields. The fund increased its commodity exposure slightly to more than 11%. Exposure to the various asset classes is monitored and calibrated on an ongoing basis to adapt to market sentiment and changes in the macroeconomic baseline scenario.

On the currency front, the fund has been very active, increasing its long USD exposure to 85%. This is partly due to our significant short exposure to sterling (-40% net exposure) primarily against the USD. Despite the various problems impacting the British economy (shortages, Brexit, high inflation, etc.), sterling has remained strong, sustained by the central bank guidance that rate hikes are needed to rein in the rising inflation. The Bank of England (BOE) will soon face the market and prove how hawkish its stance really is. The fund has been also long Swiss franc and to a lesser extent Norwegian krone, which appreciated nicely during the month.

In October, the HESPER FUND - Global Solutions EUR T-6 rose by 0.89%. Year-to-date performance was 7.05%. Over the last 12 months, the fund has gained 9.75%. Volatility has remained stable and low at 6.5%, retaining an interesting risk/reward profile.

*Der HESPER FUND - Global Solutions ist aktuell nur zum Vertrieb in Deutschland, Italien, Luxemburg, Frankreich und der Schweiz zugelassen.

Figure 1: Portfolio structure* of the Ethna-DEFENSIV

Figure 2: Portfolio structure* of the Ethna-AKTIV

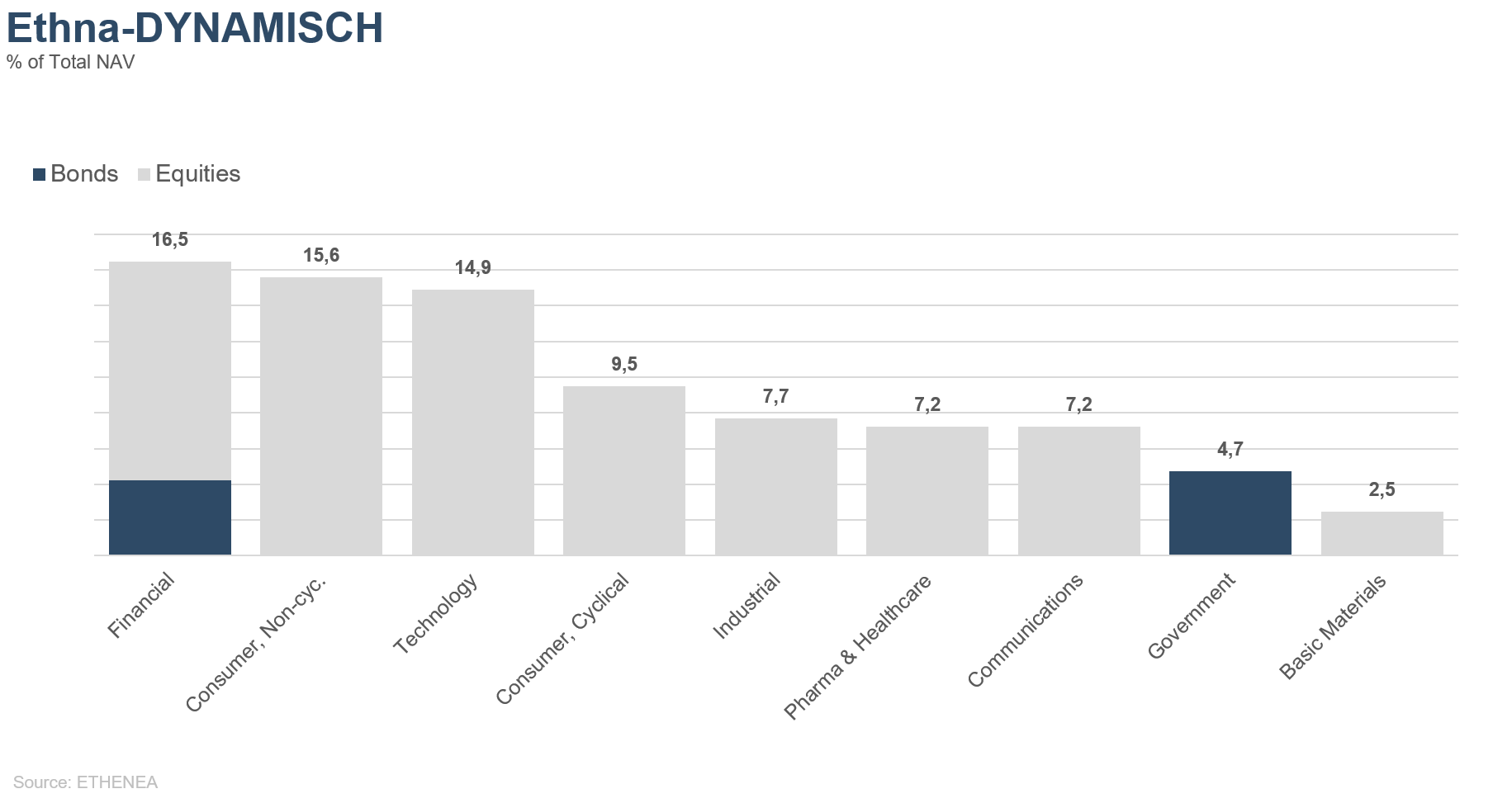

Figure 3: Portfolio structure* of the Ethna-DYNAMISCH

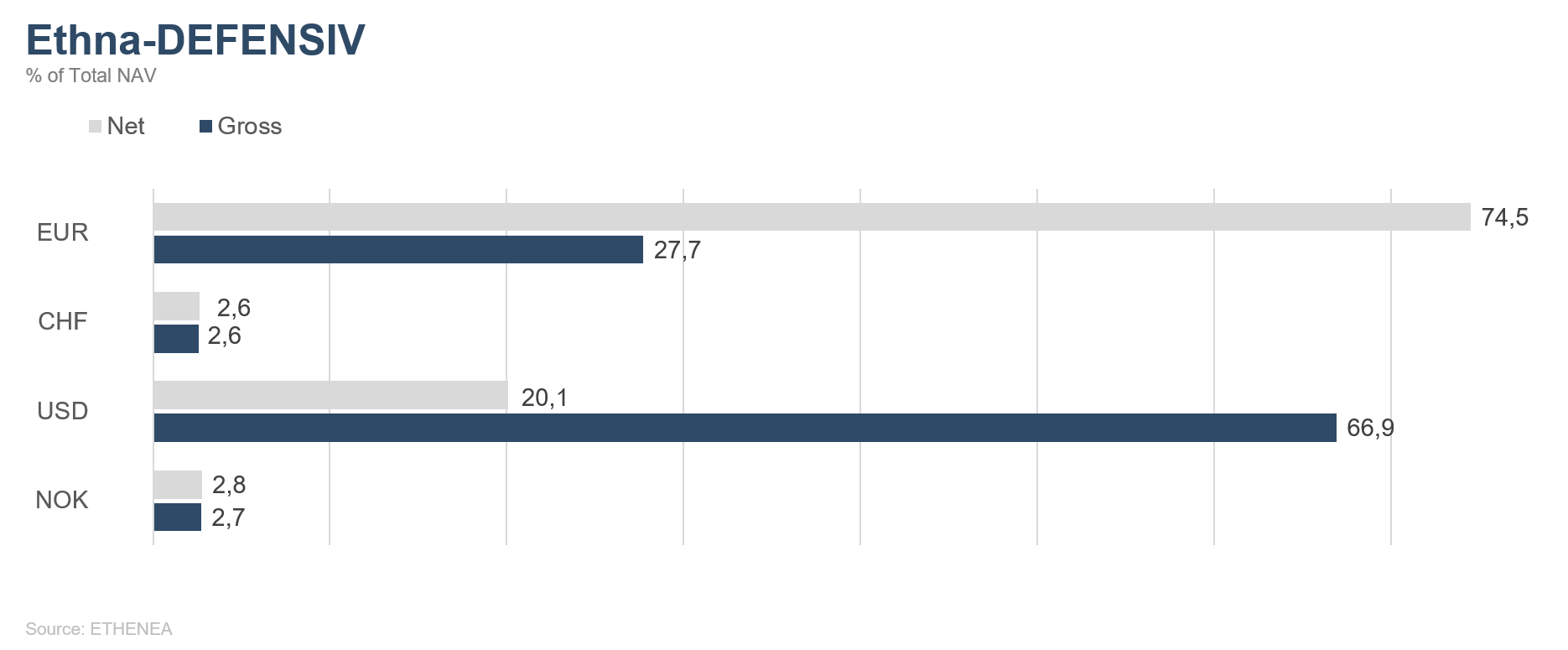

Figure 4: Portfolio composition of the Ethna-DEFENSIV by currency

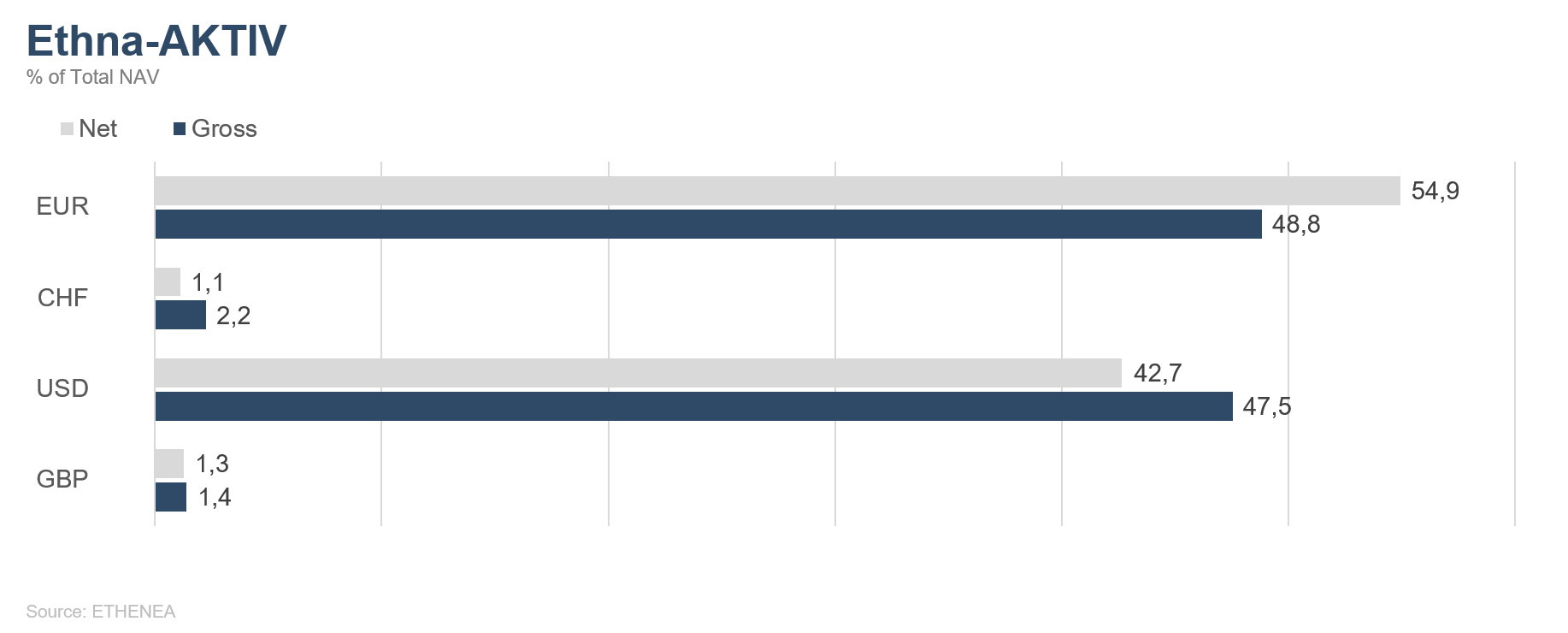

Figure 5: Portfolio composition of the Ethna-AKTIV by currency

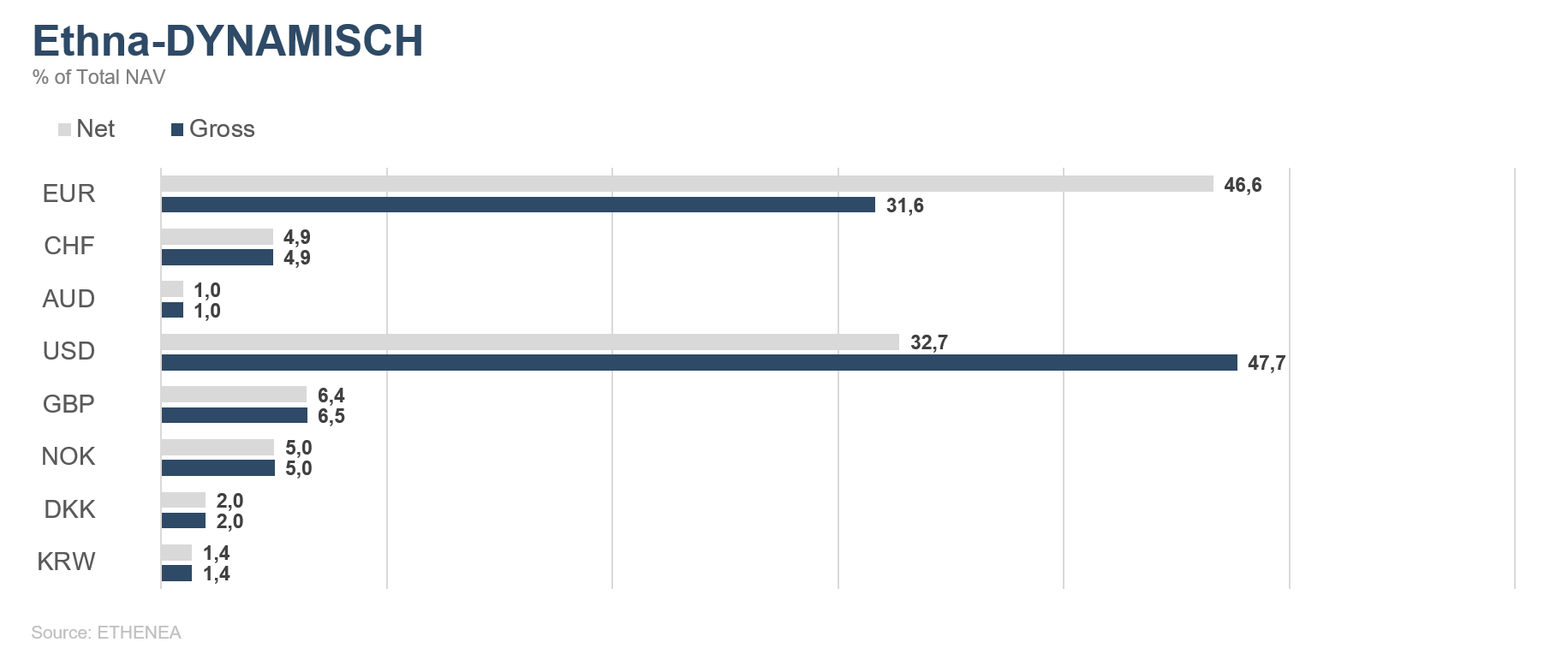

Figure 6: Portfolio composition of the Ethna-DYNAMISCH by currency

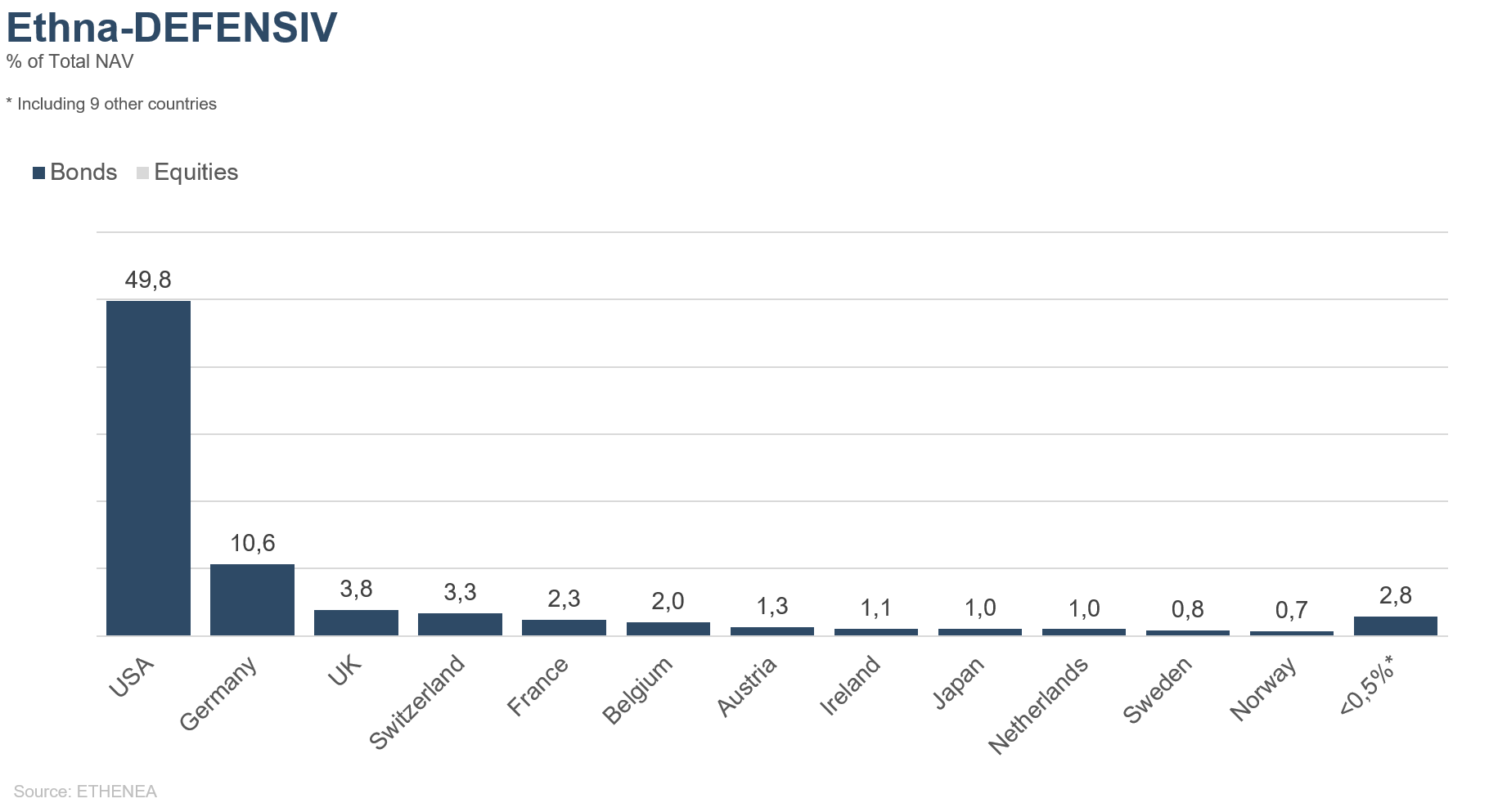

Figure 7: Portfolio composition of the Ethna-DEFENSIV by country

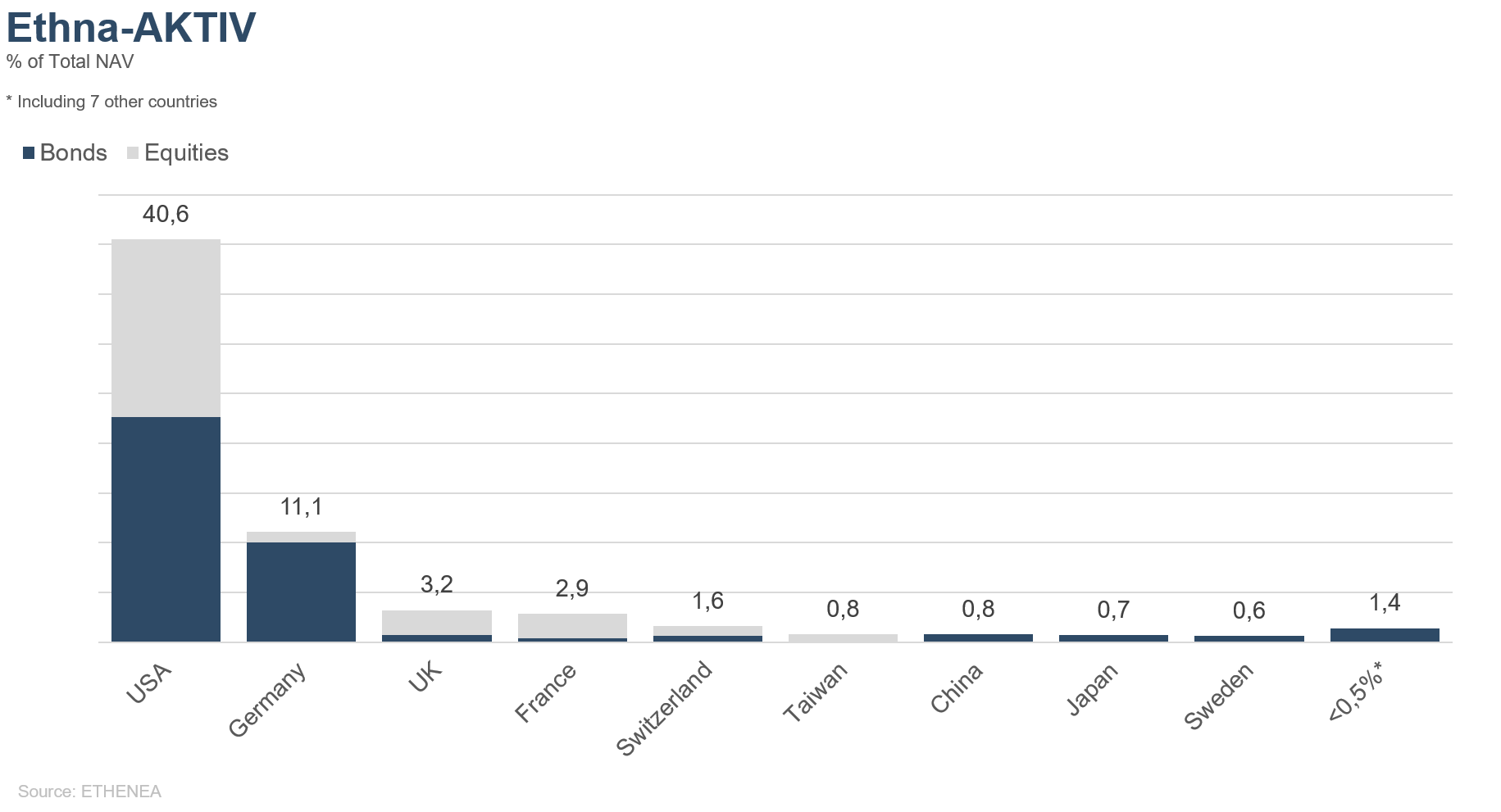

Figure 8: Portfolio composition of the Ethna-AKTIV by country

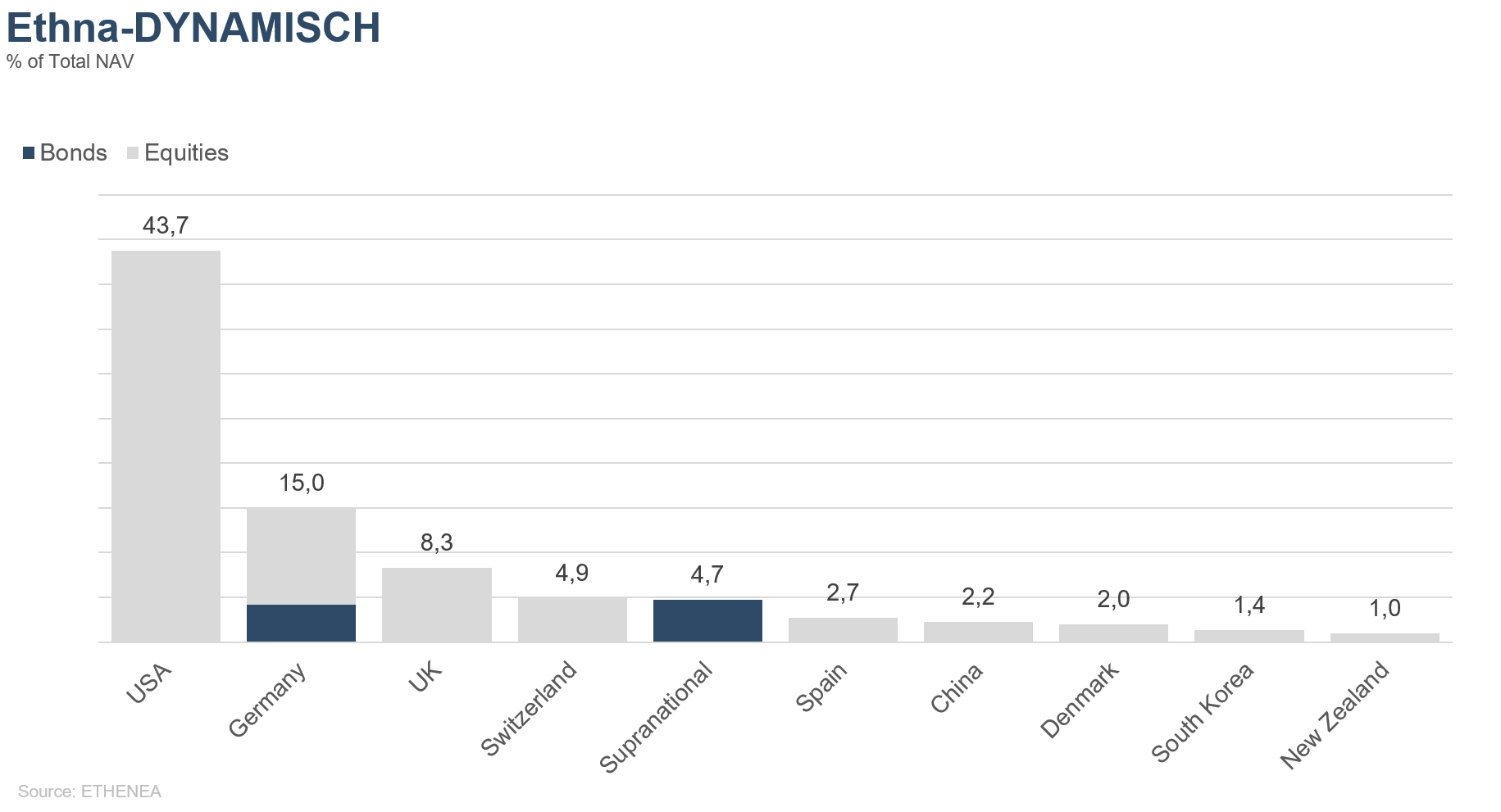

Figure 9: Portfolio composition of the Ethna-DYNAMISCH by country

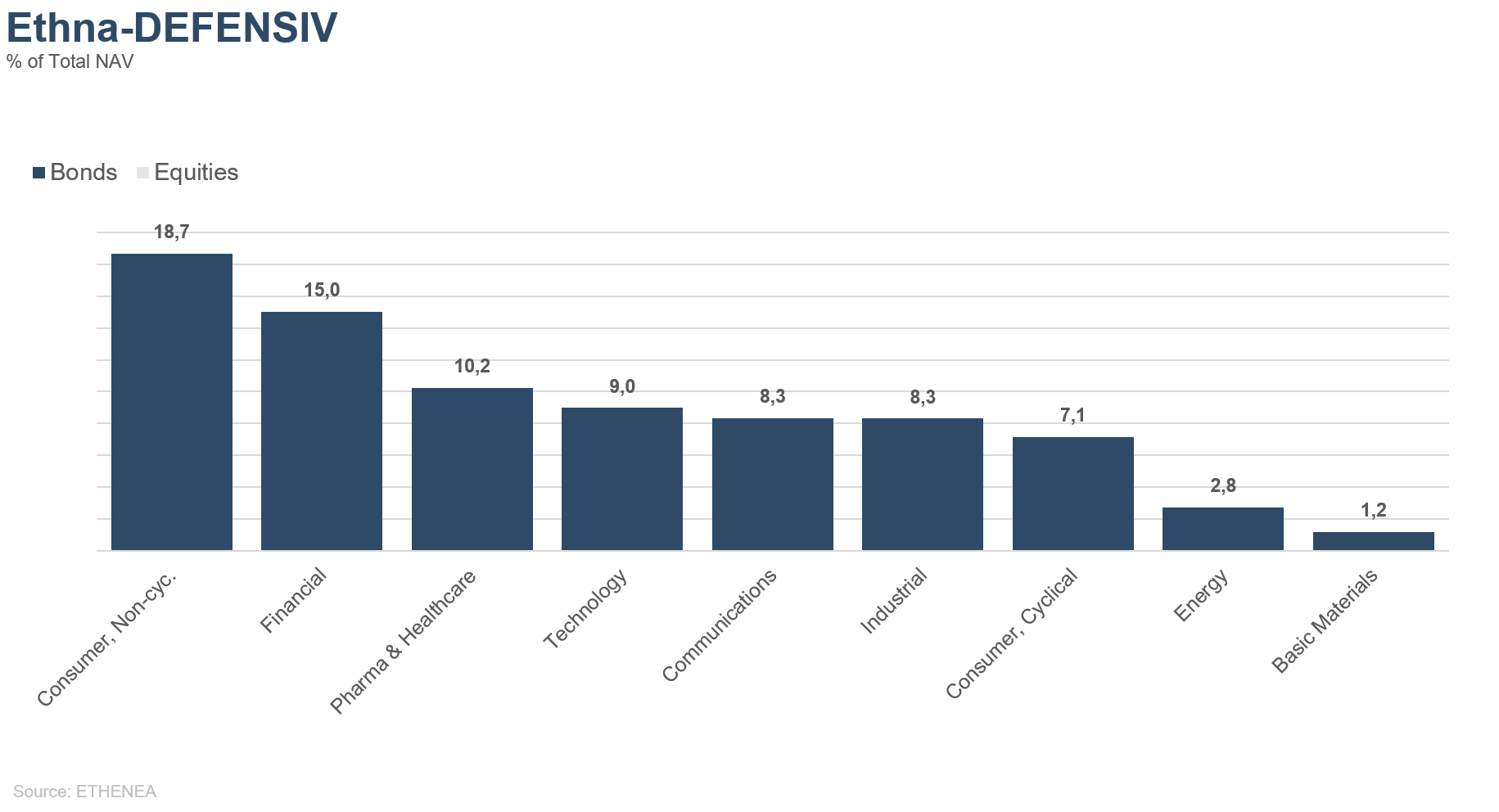

Figure 10: Portfolio composition of the Ethna-DEFENSIV by issuer sector

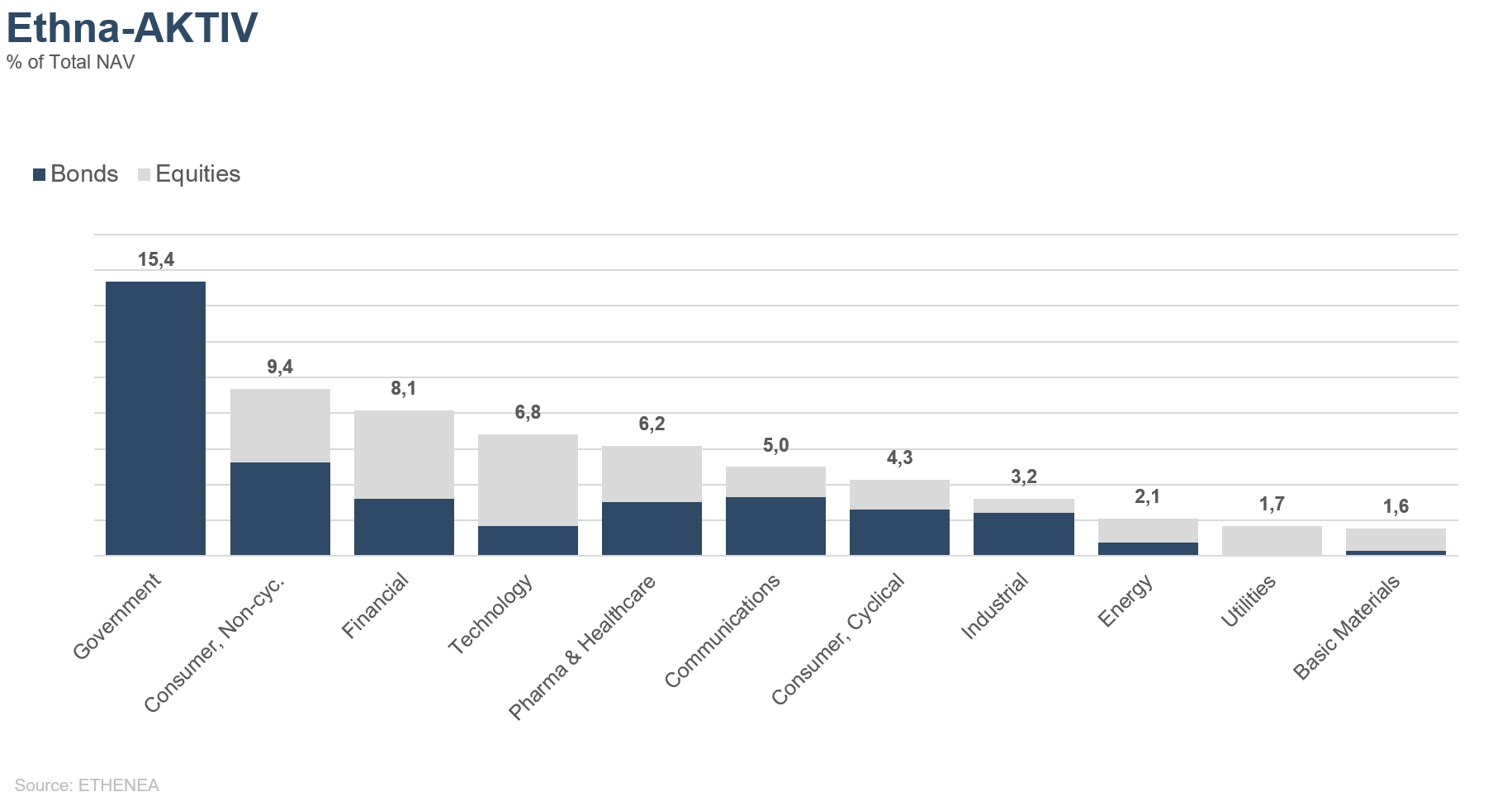

Figure 11: Portfolio composition of the Ethna-AKTIV by issuer sector

Figure 12: Portfolio composition of the Ethna-DYNAMISCH by issuer sector

* “Cash” comprises term deposits, call money and current accounts/other accounts. “Equities net” comprises direct investments and exposure resulting from equity derivatives.

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

Dit is een marketing communicatie. Het is uitsluitend bedoeld om productinformatie te verstrekken en is geen verplicht wettelijk of regelgevend document. De informatie in dit document vormt geen verzoek, aanbod of aanbeveling om participaties in het fonds te kopen, te verkopen of om enige andere transactie aan te gaan. Het is uitsluitend bedoeld om de lezer inzicht te geven in de belangrijkste kenmerken van het fonds, zoals het beleggingsproces, en wordt noch geheel noch gedeeltelijk beschouwd als een beleggingsaanbeveling. De verstrekte informatie is geen vervanging voor de eigen overwegingen van de lezer of voor enige andere juridische, fiscale of financiële informatie en advies. Noch de beleggingsmaatschappij, noch haar werknemers of bestuurders kunnen aansprakelijk worden gesteld voor verliezen die rechtsreeks of onrechtstreeks worden geleden door het gebruik van de inhoud van dit document of in enig ander verband met dit document. De verkoopdocumenten in het Duits die op dit moment geldig zijn (verkoopprospectus, essentiële-informatiedocumenten (PRIIPs-KIDs) en de halfjaar- en jaarverslagen), die gedetailleerde informatie geven over de aankoop van participaties in het fonds en de bijbehorende kansen en risico's, vormen de enige wettelijke basis voor de aankoop van participaties. De bovengenoemde verkoopdocumenten in het Duits (evenals in onofficiële vertalingen in andere talen) zijn te vinden op www.ethenea.com en zijn naast de beleggingsmaatschappij ETHENEA Independent Investors S.A. en de depothoudende bank, ook gratis verkrijgbaar bij de respectieve nationale betaal- of informatieagenten en van de vertegenwoordiger in Zwitserland. De betaal- of informatieagenten voor de fondsen Ethna-AKTIV, Ethna-DEFENSIV en Ethna-DYNAMISCH zijn de volgende: België, Duitsland, Liechtenstein, Luxemburg, Oostenrijk: DZ PRIVATBANK S.A., 4, rue Thomas Edison, L-1445 Strassen, Luxemburg; Frankrijk: CACEIS Bank France, 1-3 place Valhubert, F-75013 Paris; Italië: State Street Bank International – Succursale Italia, Via Ferrante Aporti, 10, IT-20125 Milano; Société Génerale Securities Services, Via Benigno Crespi, 19/A - MAC 2, IT-20123 Milano; Banca Sella Holding S.p.A., Piazza Gaudenzio Sella 1, IT-13900 Biella; Allfunds Bank S.A.U – Succursale di Milano, Via Bocchetto 6, IT-20123 Milano; Spanje: ALLFUNDS BANK, S.A., C/ Estafeta, 6 (la Moraleja), Edificio 3 – Complejo Plaza de la Fuente, ES-28109 Alcobendas (Madrid); Zwitserland: Vertegenwoordiger: IPConcept (Schweiz) AG, Münsterhof 12, Postfach, CH-8022 Zürich; Betaalagent: DZ PRIVATBANK (Schweiz) AG, Münsterhof 12, CH-8022 Zürich. De betaal- of informatieagenten voor HESPER FUND, SICAV - Global Solutions zijn de volgende: België, Duitsland, Frankrijk, Luxemburg, Oostenrijk: DZ PRIVATBANK S.A., 4, rue Thomas Edison, L-1445 Strassen, Luxemburg; Italië: Allfunds Bank S.A.U – Succursale di Milano, Via Bocchetto 6, IT-20123 Milano; Zwitserland: Vertegenwoordiger: IPConcept (Schweiz) AG, Münsterhof 12, Postfach, CH-8022 Zürich; Betaalagent: DZ PRIVATBANK (Schweiz) AG, Münsterhof 12, CH-8022 Zürich. De beleggingsmaatschappij kan bestaande distributieovereenkomsten met derden beëindigen of distributievergunningen intrekken om strategische of statutaire redenen, mits inachtneming van eventuele deadlines. Beleggers kunnen informatie over hun rechten verkrijgen op de website www.ethenea.com en in de verkoopprospectus. De informatie is zowel in het Duits als in het Engels beschikbaar, en in individuele gevallen ook in andere talen. Opgemaakt door: ETHENEA Independent Investors S.A. Het is verboden om dit document te verspreiden aan personen die wonen in landen waar het fonds geen vergunning heeft of waar er een toestemming vereist is voor verspreiding. Participaties mogen enkel aangeboden worden aan personen in landen waarin dit aanbod in overeenstemming is met de toepasselijke wettelijke bepalingen en waar ervoor wordt gezorgd dat de verspreiding en publicatie van dit document, evenals een aanbod of verkoop van participaties, aan geen enkele beperking is onderworpen in het betreffende rechtsgebied. Het fonds wordt met name niet aangeboden in de Verenigde Staten van Amerika of aan Amerikaanse burgers (volgens Rule 902 of Regulation S of the U.S. Securities Act of 1933, in de huidige versie) of personen die namens hen, in hun rekening of ten voordele van een Amerikaanse burger handelen. Resultaten die in het verleden behaald zijn, mogen niet worden opgevat als indicatie of garantie voor toekomstige prestaties. Schommelingen in de waarde van onderliggende financiële instrumenten of hun rendementen, evenals veranderingen in rentetarieven en valutakoersen, zorgen ervoor dat de waarde van participaties in een fonds, evenals de daaruit voortvloeiende rendementen, zowel kunnen dalen als stijgen en zijn niet gegarandeerd. De waarderingen die hierin opgenomen zijn, zijn gebaseerd op een aantal factoren, waaronder, maar niet beperkt tot, huidige prijzen, schattingen van de waarde van de onderliggende activa en marktliquiditeit, evenals andere veronderstellingen en openbaar beschikbare informatie. In principe kunnen prijzen, waarden en rendementen zowel stijgen als dalen, tot en met het totale verlies van het geïnvesteerde kapitaal, en aannames en informatie kunnen zonder voorafgaande kennisgeving worden gewijzigd. De waarde van het belegde vermogen of de prijs van participaties, evenals de daaruit voortvloeiende rendementen en uitkeringsbedragen, zijn onderhevig aan schommelingen of kunnen geheel verdwijnen. Positieve prestaties in het verleden zijn daarom geen garantie voor positieve prestaties in de toekomst. Met name het behoud van het geïnvesteerde vermogen kan niet worden gegarandeerd; er is dan ook geen garantie dat de waarde van het belegde kapitaal of de aangehouden participaties bij verkoop of terugkoop zal overeenkomen met het oorspronkelijk belegde kapitaal. Beleggingen in vreemde valuta zijn onderhevig aan bijkomende wisselkoersschommelingen of valutarisico's, d.w.z. het rendement van dergelijke beleggingen hangt ook af van de volatiliteit van de vreemde valuta, wat een negatieve impact kan hebben op de waarde van het belegde kapitaal. Beleggingen en toewijzingen kunnen gewijzigd worden. De beheer- en depotvergoedingen, evenals alle andere kosten die overeenkomstig de contractuele bepalingen ten laste van het fonds zijn, worden in de berekening opgenomen. De prestatieberekening is gebaseerd op de BVI-methode (Duitse Federale Vereniging voor Beleggings- en Vermogensbeheer), dat wil zeggen dat uitgiftekosten, transactiekosten (zoals order- en makelaarskosten), evenals bewaar- en andere beheervergoedingen niet inbegrepen zijn in de berekening. Het beleggingsrendement zou lager zijn indien rekening zou worden gehouden met de uitgiftetoeslag. Er kan geen garantie worden gegeven dat de marktprognoses gehaald worden. Om het even welke risicobehandeling in deze publicatie mag niet worden beschouwd als een onthulling van alle risico's of een sluitende behandeling van de genoemde risico's. In de verkoopprospectus wordt expliciet verwezen naar de gedetailleerde risicobeschrijvingen. Er kan geen garantie worden gegeven dat de informatie juist, volledig of actueel is. De inhoud en de informatie zijn auteursrechtelijk beschermd. Er kan geen garantie worden gegeven dat het document voldoet aan alle wettelijke of regelgevende vereisten die andere landen dan Luxemburg hebben vastgesteld. Opmerking: De belangrijkste technische termen kunnen worden gevonden in de woordenlijst op www.ethenea.com/lexicon. Informatie voor beleggers in België: Het prospectus, de statuten en de periodieke verslagen, alsmede de essentiële-informatiedocumenten (PRIIPs-KIDs), zijn kosteloos verkrijgbaar in het Frans bij de beheermaatschappij, ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxemburg en bij de vertegenwoordiger: DZ PRIVATBANK S.A., 4, rue Thomas Edison, L-1445 Strassen, Luxemburg. Informatie voor beleggers in Zwitserland: Het vestigingsland van de collectieve beleggingsregeling is Luxemburg. De vertegenwoordiger in Zwitserland is IPConcept (Schweiz) AG, Münsterhof 12, P.O. Box, CH-8022 Zürich. De betaalagent in Zwitserland is DZ PRIVATBANK (Schweiz) AG, Münsterhof 12, CH-8022 Zurich. Het prospectus, de essentiële-informatiedocumenten (PRIIPs-KIDs) en de statuten, evenals de jaar- en halfjaarverslagen zijn kosteloos verkrijgbaar bij de vertegenwoordiger. Copyright © ETHENEA Independent Investors S.A. (2025) Alle rechten voorbehouden. 03-11-2021