Your questions, our answers

Markets continue to be influenced by geopolitics and persistently high inflation on both sides of the Atlantic. In our second quarterly update of the year, portfolio managers responded to the following questions, among others, to explain their views.

Ethna-DEFENSIV

Ethna-AKTIV

Ethna-DYNAMISCH

Ethna-DEFENSIV

When do you think it is time to invest in or switch to longer-dated bonds? What would be your criteria for selecting longer-dated bonds?

From our point of view, this time has already come. In recent weeks, we have invested opportunistically in the corporate bonds with maturities between 2028 and 2032. The slowdown of the global economy, especially in the industrialised countries such as the US and the EU, as well as falling inflation rates give us reason to expect lower yields at the longer end of the yield curve. An increase in duration therefore seems attractive to us. So far, we have increased the interest rate sensitivity of our portfolio to 4.4 by investing in new issues and building a 15% position in 10-year US Treasuries.

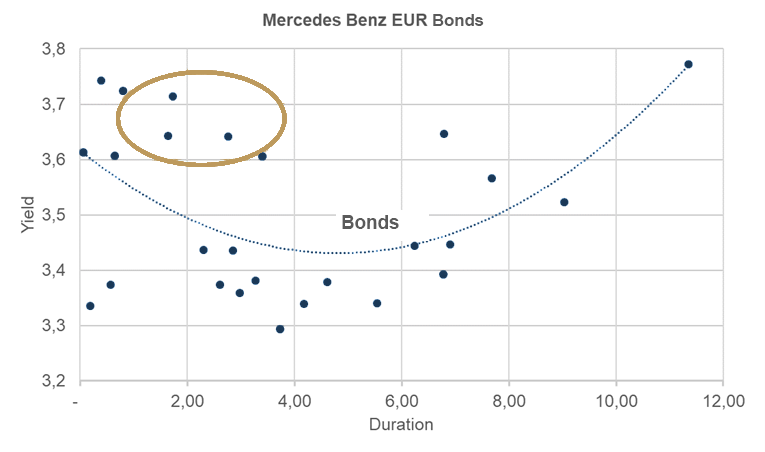

There are two factors to consider when selecting individual positions. The first is yield. In the current economic environment, we can achieve higher returns without taking on more risk. Yields above 4.5% are attractive to us at the moment, and we are closely monitoring new issues in this area. At the same time, the second factor is the inversion of the government yield curve. For some safer companies, the risk premium is not sufficient to form an inverted curve (government yield + risk premium). For example, the government yield at the short end and the risk premium at the long end of the Mercedes Benz yield curve have a greater impact, leading to a U-shaped curve (blue line in Figure 1).

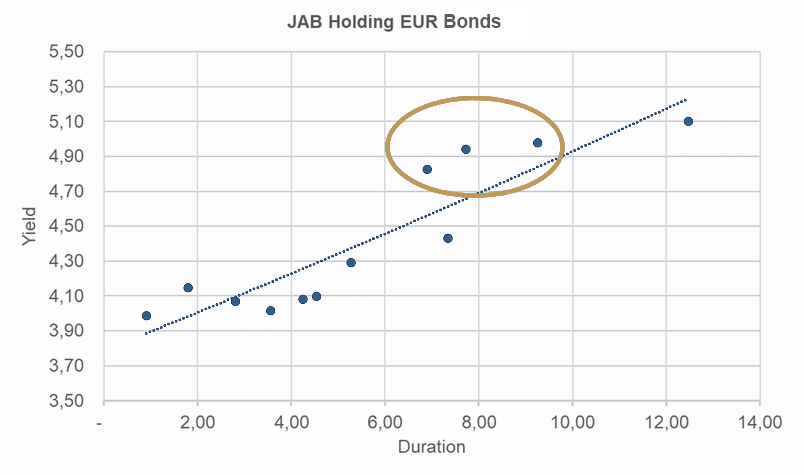

Other companies offer higher risk premiums. Companies such as JAB Holdings, Autostrade per L'Italia Autostrade, Fiserv or VW have linearly rising yield curves:

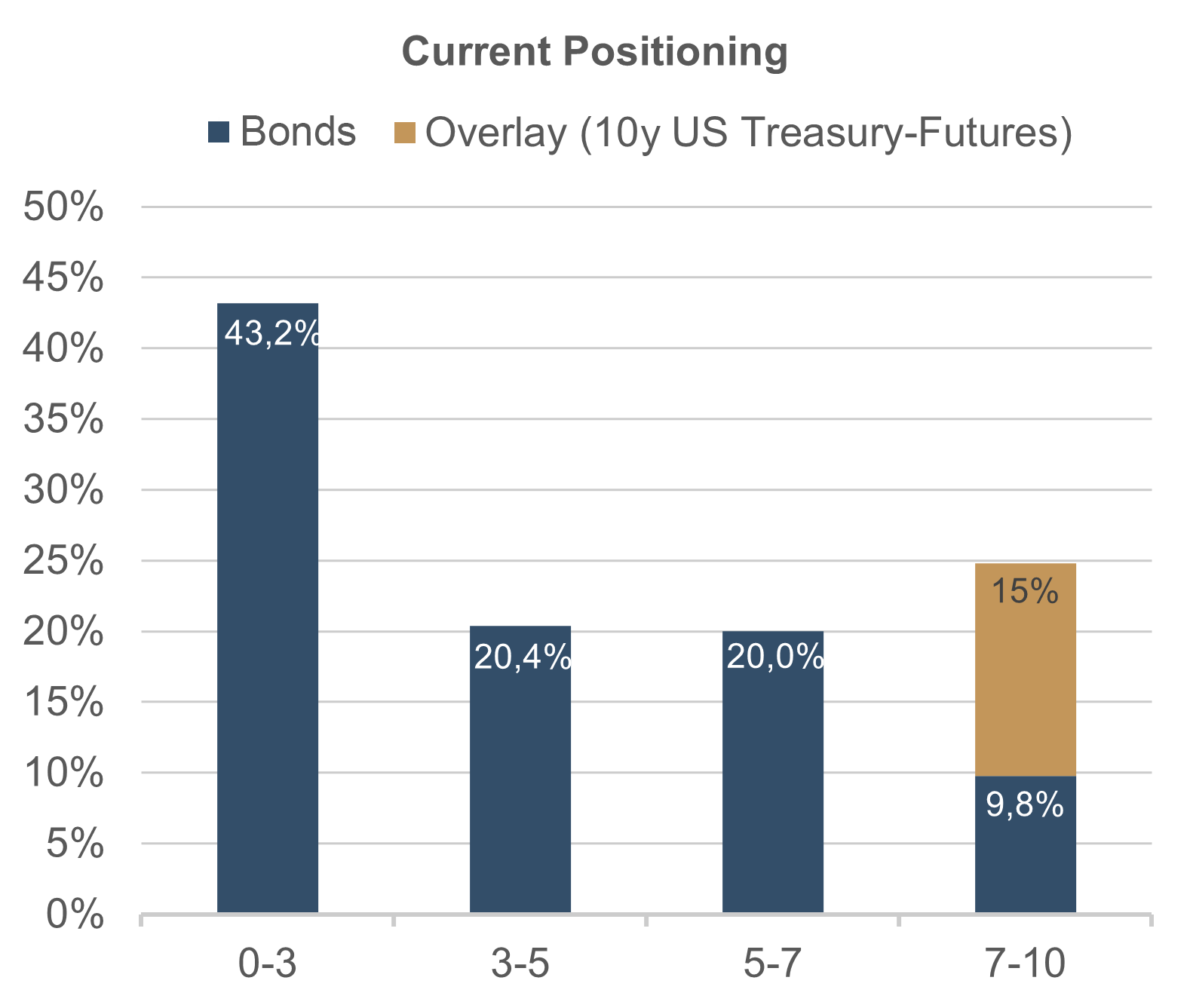

We are therefore currently positioned to benefit from the inversion with 43.2% exposure in the 0-3 year maturities and 24.8% (incl. futures overlay) at the long end.

Ethna-AKTIV

Ethna-AKTIV has always been a very conservative fund, so the equity allocation is surprising, especially given the current situation on the capital markets. Can you please explain this?

The Ethna-AKTIV is still the right choice for the conservative and risk-conscious investor. However, the attributes active and flexible are also part of our offering. Our task is to find the optimal asset allocation for attractive long-term capital growth, depending on the market environment. This is usually derived from an assessment of the macroeconomic situation, valuation parameters and positioning data. At the end of the first quarter, we noted a clear disconnect between the available macro data, including our forecasts, and the measurable reaction of market participants (flows and positioning). Despite declining inflation, stable to positive markets for months, and an economic outlook that was relatively constructive to us, the sentiment and positioning of many market participants was very negative. We recognised this opportunity and our flexible approach allowed us to adjust the portfolio accordingly. It is important to note that this does not contradict the conservative nature of the portfolio. On a risk/reward basis, the opportunities outweighed the risks at the time. Firstly, a market that everyone expects to fall is relatively well supported. You have usually hedged accordingly. Second, when prices are stable, it often only takes a catalyst to adjust positioning and follow a new narrative. The shift from the recession to the soft-landing narrative and the hype about the potential efficiency gains from artificial intelligence were just such catalysts. But adjusting the equity exposure was not the only adjustment. We have also significantly increased the duration of the bond portfolio this year and hedged all currency risks. This means that changing a specific allocation is never an isolated decision but must always be seen in the context of the entire portfolio. In the meantime, however, the starting position on the equity side has changed to the extent that we are currently discussing a return to a more neutral position. Always in the spirit of: Taking active and flexible advantage of opportunities.

Ethna-DYNAMISCH

Looking at the hype around AI and NVIDIA's spectacular performance: Do you think it is sustainable? Do you want to allocate part of Ethna-DYNAMISCH to this segment to participate in the potential gains of this industry?

Although Artificial Intelligence (AI) is nothing new, it is the ChatGPT application that seems to have really caught the public's imagination. So much so that hardly a day goes by without another company announcing its AI solutions and capabilities. The stock market is taking notice.

We don't want to underestimate the fact that AI has the potential to change many things. From efficiency gains to new products and services. But we are sceptical that this will happen as suddenly as the recent performance of some stocks suggests. Spectacular really is the appropriate description.

Well, not everything is fantasy, some of it is already reality: NVIDIA's latest quarterly results were huge. The fundamental performance is of course impressive. But to be considered for an investment, the valuation must also be right. Keyword: "growth at a reasonable price" (GARP). In any case, we are not entirely comfortable with an expected P/E ratio of around 50. The potential for setbacks is too great if the high growth expectations are not met. Experience shows that over-hyped themes and stocks that are flooded with inflows into active or passive fund structures have a hard time meeting expectations - and thus their valuation levels - in the future.

It is true that over a longer time horizon, valuation plays an increasingly subordinate role if the fundamentals are right. But the past has also shown that it is very difficult to identify the long-term winners in technological (r)evolutions, even if they seem obvious in retrospect. In any case, Alphabet was considered the leader in the field of AI language models until OpenAI’s ChatGPT, which is essentially funded by Microsoft, took off. Competition is very dynamic.

We are already invested in several AI companies, although this was not the basis of our initial investment decision. We also have a number of relevant stocks on our watch list. We will not hesitate to invest when opportunities arise. Until then, however, we prefer companies that are thriving outside the hype. Those with solid fundamental growth (preferably with good visibility) and attractive valuations, i.e. GARP stocks.

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

Deze marketingmededeling dient uitsluitend ter informatie. Het mag niet worden doorgegeven aan personen in landen waar het fonds niet voor distributie is toegestaan, met name in de VS of aan Amerikaanse personen. De informatie vormt noch een aanbod noch een uitnodiging tot koop of verkoop van effecten of financiële instrumenten en vervangt geen op de belegger of het product toegesneden advies. Er wordt geen rekening gehouden met de individuele beleggingsdoelstellingen, financiële situatie of bijzondere behoeften van de ontvanger. Lees vóór een beleggingsbeslissing zorgvuldig de geldende verkoopdocumenten (prospectus, essentiële informatiedocumenten/PRIIPs-KIDs, halfjaar- en jaarverslagen). Deze documenten zijn beschikbaar in het Duits en als niet-officiële vertaling bij ETHENEA Independent Investors S.A., de bewaarbank, de nationale betaal- of informatiekantoren en op www.ethenea.com. De belangrijkste vaktermen vindt u in de lexicon op www.ethenea.com/lexicon/. Uitgebreide informatie over kansen en risico's van onze producten vindt u in het actuele prospectus. In het verleden behaalde resultaten bieden geen betrouwbare indicatie voor toekomstige prestaties. Prijzen, waarden en opbrengsten kunnen stijgen of dalen en kunnen leiden tot volledig verlies van het geïnvesteerde kapitaal. Beleggingen in vreemde valuta zijn onderhevig aan extra valutarisico's. Aan de verstrekte informatie kunnen geen bindende toezeggingen of garanties voor toekomstige resultaten worden ontleend. Aannames en inhoud kunnen zonder voorafgaande kennisgeving worden gewijzigd. De samenstelling van de portefeuille kan op elk moment wijzigen. Dit document vormt geen volledige risico-informatie. De distributie van het product kan vergoedingen opleveren voor de beheermaatschappij, verbonden ondernemingen of distributiepartners. De informatie over vergoedingen en kosten in het actuele prospectus is doorslaggevend. Een lijst van nationale betaal- en informatiekantoren, een samenvatting van de beleggersrechten en informatie over de risico's van een foutieve netto-inventariswaarde-berekening vindt u op www.ethenea.com/juridische-opmerkingen/. In geval van een foutieve NIW-berekening wordt compensatie verleend volgens CSSF-circulaire 24/856; bij via financiële intermediairs aangeschafte participaties kan de compensatie beperkt zijn. Informatie voor beleggers in Zwitserland: Het land van herkomst van de collectieve belegging is Luxemburg. De vertegenwoordiger in Zwitserland is IPConcept (Schweiz) AG, Bellerivestrasse 36, CH-8008 Zürich. De betaalagent in Zwitserland is DZ PRIVATBANK (Schweiz) AG, Bellerivestrasse 36, CH-8008 Zürich. Prospectus, essentiële informatiedocumenten (PRIIPs-KIDs), statuten en de jaar- en halfjaarverslagen zijn gratis verkrijgbaar bij de vertegenwoordiger. Informatie voor beleggers in België: Het prospectus, de essentiële informatiedocumenten (PRIIPs-KIDs), de jaarverslagen en de halfjaarverslagen van het subfonds zijn op verzoek gratis in het Duits verkrijgbaar bij ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxemburg en bij de vertegenwoordiger: DZ PRIVATBANK AG, Niederlassung Luxemburg, 4, rue Thomas Edison, L-1445 Strassen, Luxemburg. Ondanks de grootst mogelijke zorg wordt geen garantie gegeven voor de juistheid, volledigheid of actualiteit van de informatie. Alleen de originele Duitstalige documenten zijn juridisch bindend; vertalingen dienen alleen ter informatie. Het gebruik van digitale advertentieformaten is op eigen risico; de beheermaatschappij aanvaardt geen aansprakelijkheid voor technische storingen of schendingen van gegevensbescherming door externe informatieaanbieders. Het gebruik is alleen toegestaan in landen waar dit wettelijk is toegestaan. Alle inhoud is auteursrechtelijk beschermd. Elke reproductie, verspreiding of publicatie, geheel of gedeeltelijk, is alleen toegestaan met voorafgaande schriftelijke toestemming van de beheermaatschappij. Copyright © ETHENEA Independent Investors S.A. (2025). Alle rechten voorbehouden. 20-06-2023