Don’t Fight the Fed! Again.

Last month was the end not only of 2019, but of a whole decade. So it makes sense to place this Market Commentary in the context of a larger time frame.

Interestingly, some parallels can be drawn between the decade as a whole and the year 2019.

A high degree of uncertainty marked the beginning of both the decade and the year just ended. In 2010, shortly after the financial crisis, it was far from clear whether the worst (from an economic point of view) was over. Global capital markets were still licking their wounds and prices were still far short of their pre-crisis levels. It remained to be seen whether the resumption of economic growth was sustainable.

It was a similar story early last year. All optimism had disappeared after almost all asset classes recorded losses in 2018, due, for one, to the escalation of the global trade conflict. The fear that the economic cycle would soon end and the spectre of recession that this raised spread around the world.

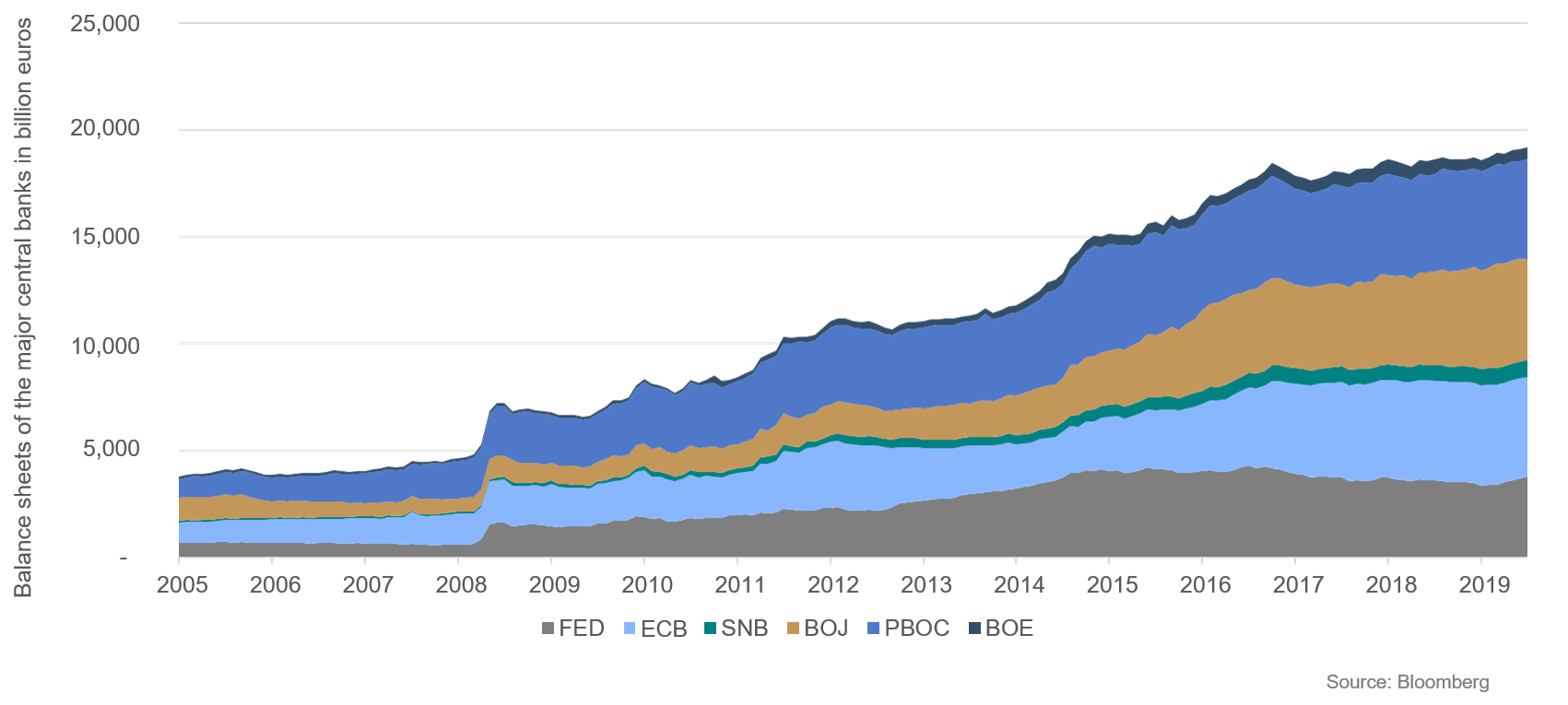

A good ten years ago, an unprecedented large-scale fiscal experiment was launched in response to the financial and economic upheaval. In parallel with record-low refinancing rates, global central banks – first and foremost the U.S. Federal Reserve – paved the way for various phases of unconventional measures with their additional purchase programmes, thereby creating a decade of ultra-accommodative monetary policy. Thus not only was the recession brought to an end, but a long-lasting economic cycle and an impressive upward trend in stock markets was initiated as well. In time, the broad MSCI World Total Return Index climbed 147%, the yield on the 10-year U.S. Treasury fell from 3.84% to 1.88% and the yield on its German counterpart fell from 3.39% as far as -0.18%. In the course of these measures, the balance sheets of the three largest central banks quadrupled in size.

Figure 1: Balance sheets of the main central banks in billions of euros

A good ten years later, it was the attempt to successively end this experiment, for one, that brought an already cooling global economy closer to recession. The parallel with the beginning of the decade becomes particularly striking when one considers that once again, the active intervention of the central banks brought about a lasting stabilisation of the financial markets and economic growth. The unexpected and very abrupt shift by the U.S. central bank in 2019 from the tightening of monetary policy it had begun, back to easing, triggered a significant risk-on rally in almost all asset classes. A short time later, the fundamentals began to bottom out. Capital markets, and the equity market in particular, once again fulfilled their role as forerunner.

Again, a portfolio manager could be successful in both periods by applying the motto “Don’t fight the Fed”.

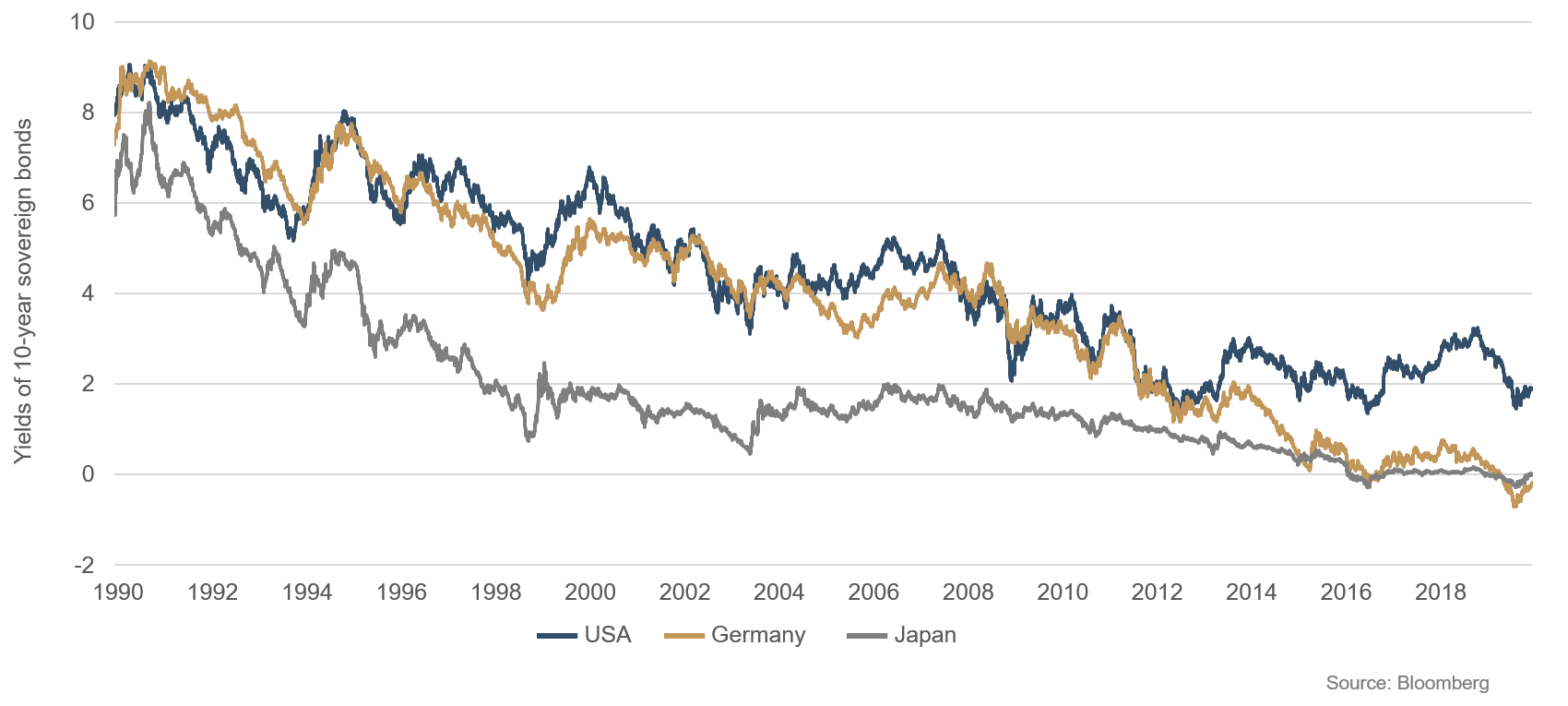

What does that mean in concrete terms for the coming year? What positioning should an investor adopt? On the one hand, we know that the central banks’ supportive stance will continue for the foreseeable future. On the other hand, a not insignificant portion of this monetary policy has probably already been priced in. The long-term interest rates remain at record lows despite the increase in the last quarter. The risk premium for corporate bonds of average quality has almost returned to the level it had reached prior to the 2008 financial crisis on both sides of the Atlantic. Equities, too, are valued at a multiple of the current and even future profits or revenues, which are at the high end of the valuation range in historical terms. From our point of view, however, these valuations at the extremes of observable historical data are not intrinsically bad. We do not think that values will directly revert to the mean after such an extreme. Rather, it is important to be aware of the current circumstances and, if necessary, query old dogmas that stem from an environment of moderate inflation and high growth. This does not mean that there will be no mean reversion on this occasion. In our analyses we, too, go by Mark Twain’s “History does not repeat itself, but it often rhymes”.

However, in the current environment the challenge is that the yield on the much-cited alternative investment – the virtually risk-free sovereign bond – has never been as low as it currently is. Thus there is no “history” for future events to “rhyme” with.

Figure 2: Yields on 10-year sovereign bonds

For this reason, it is all the more important to remain open even to scenarios that do not necessarily follow a familiar pattern. Anomalies must be played through to the end – or at least thought through to the end – taking into account the changing environment, which, in case of doubt, must be regarded as the new normal. What, for instance, does it mean for central banks’ interest rate policy when the national debt is already enormous in many developed countries? Not much, as long as debt grows at a slower pace than the economy. But what if that’s not the case? What happens if increasing populism ramps up current spending further and further – building up a debt mountain that will have to be reduced in the future – without stimulating economic growth? Without going into too much detail, it can be said that this aspect alone has far-reaching consequences both for interest rates and for capital market development.

For us as active portfolio managers, what we have to do is come up with short-term and long-term scenarios, and work their consequences for the various asset classes. When determining the subjective probabilities of the scenarios occurring, one must take care to avoid the usual pitfalls of behavioural economics. Is our attitude positive only because last year was positive (anchoring effect), or are we talking up the theories and looking for information to confirm them (confirmation bias)?

Looking ahead to the new year, which is also the start of a new decade, our main scenario tends to be constructive. We are acutely aware of the risks, which are no doubt numerous. However, we are confident that risks always go hand in hand with opportunities. For example, if interest rates fall further – which we expect in the longer term – equities have plenty of upside potential in terms of valuation alone. How much potential remains to be seen this year, and this decade.

Auteur:

In search of inflation

In our latest video, Dr Volker Schmidt goes into the key elements that may indicate rising inflation, and explains how this affects our bond strategy in the Ethna-DEFENSIV and the Ethna-AKTIV.

Kan de video niet weergegeven worden? Gelieve HIER TE KLIKKEN.

Positioning of the Ethna Funds

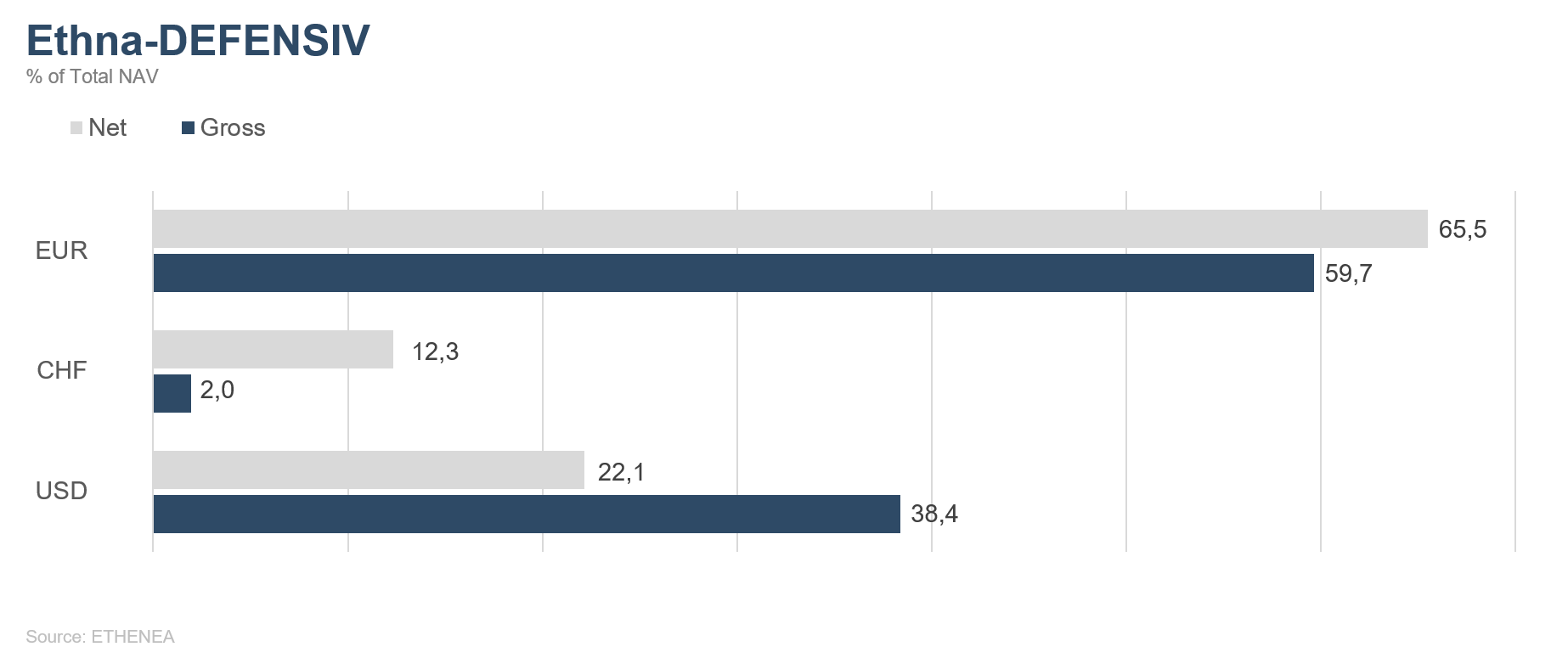

Ethna-DEFENSIV

Fresh impetus in December came not from the Fed or the ECB, but from Donald Trump. But let’s talk about the central banks first. As expected, the ECB’s monetary policy has not changed under new president Christine Lagarde, and the key rate remains at the historic low of 0%. The ECB also left the deposit rate at its previous level of -0.5%. Since the beginning of November the ECB has been buying up 20 billion euros’ worth of bonds on the secondary market due to the weak economy. An end date for the programme was not set in the latest meeting either. Also as we expected, the U.S. central bank, the Federal Reserve, left the Fed Funds rate unchanged in the range of 1.5% to 1.75%. In addition, the Fed made it clear that following the three rate cuts of 25 basis points each in July, September and October of 2019, it deems the current interest rate level as appropriate. It thus indicated that there will be no change in the monetary policy for the foreseeable future. On the whole, the central bank meetings threw no curveballs at all. December held a pleasant surprise on the issue of Brexit. Boris Johnson’s Tories were the clear winners of the general election in the UK. Now that they have an absolute majority, the Conservatives can press ahead with Brexit.

However, the rapprochement in the trade conflict probably had the biggest impact on markets. The U.S. and China have agreed Phase One of a trade deal which is to be signed this month. Hopes for a resulting improvement of the global economy led to falls in the prices of long-dated sovereign bonds over the course of the month. Yields on 10-year Bunds rose from -0.36% to -0.26%, and those on 10-year Treasuries from 1.77% to 1.87%. In this environment, the reaction was a narrowing of risk premia on corporate bonds.

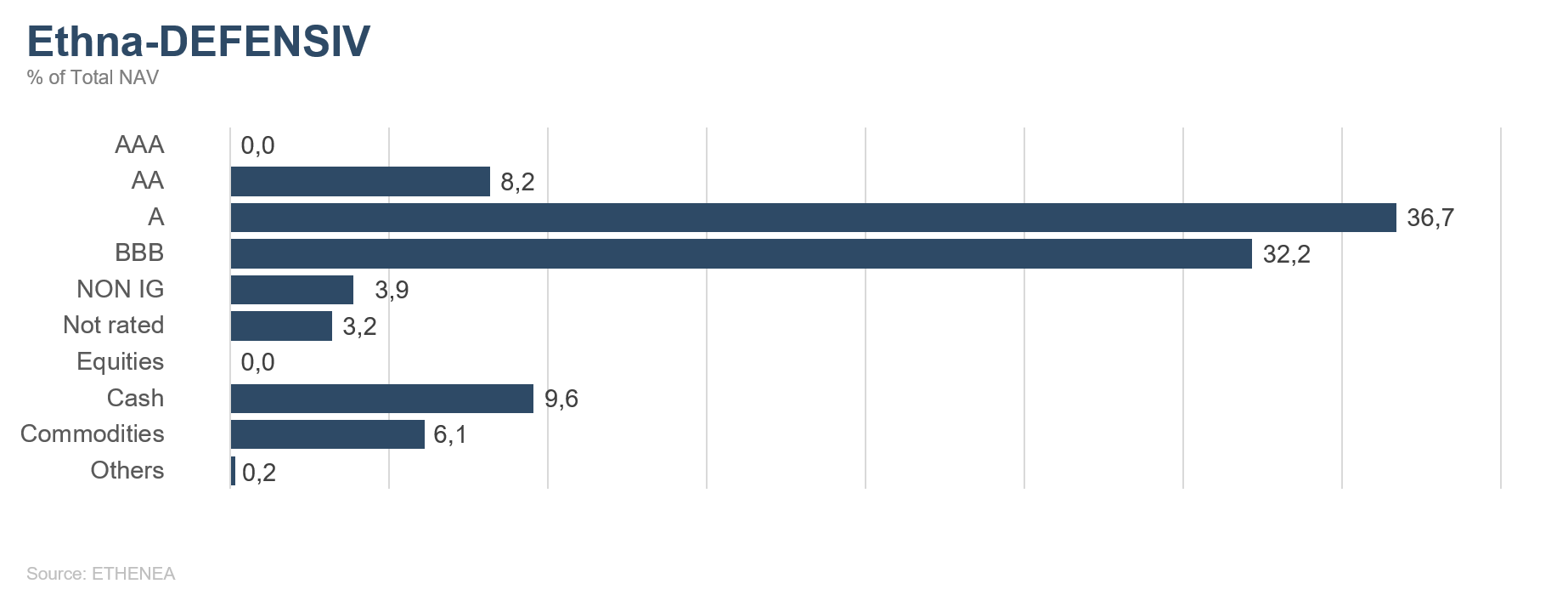

Within the Ethna-DEFENSIV, we maintain our focus on high quality, globally diversified companies. The average rating remains between A- and BBB+ and illustrates the portfolio’s robustness. Despite rising interest rates and a slightly weaker dollar against the euro, the fund managed to make a small gain over the month, as falling risk premia for corporate bonds and the higher price of gold more than compensated for the movements in interest rates and currencies. The tactical reduction of duration also made a positive contribution to performance. For one, we took profits on long-dated bonds and increased the cash allocation. For another, we further reduced the dollar duration by selling Treasury futures. Our position in Spanish sovereign bonds should benefit from the resumption of the ECB’s asset purchase programme. Gold remains part of the portfolio mix. We still assume that the growth dynamics in the U.S. will remain stronger than in Europe, and that the euro will tend to weaken against the U.S. dollar. In addition, bond markets, especially in Europe, will continue to be supported by persistently low interest rates. Since trade relations between the U.S. and China are easing, we can well imagine taking on more risk again soon; for instance, by increasing the equity allocation.

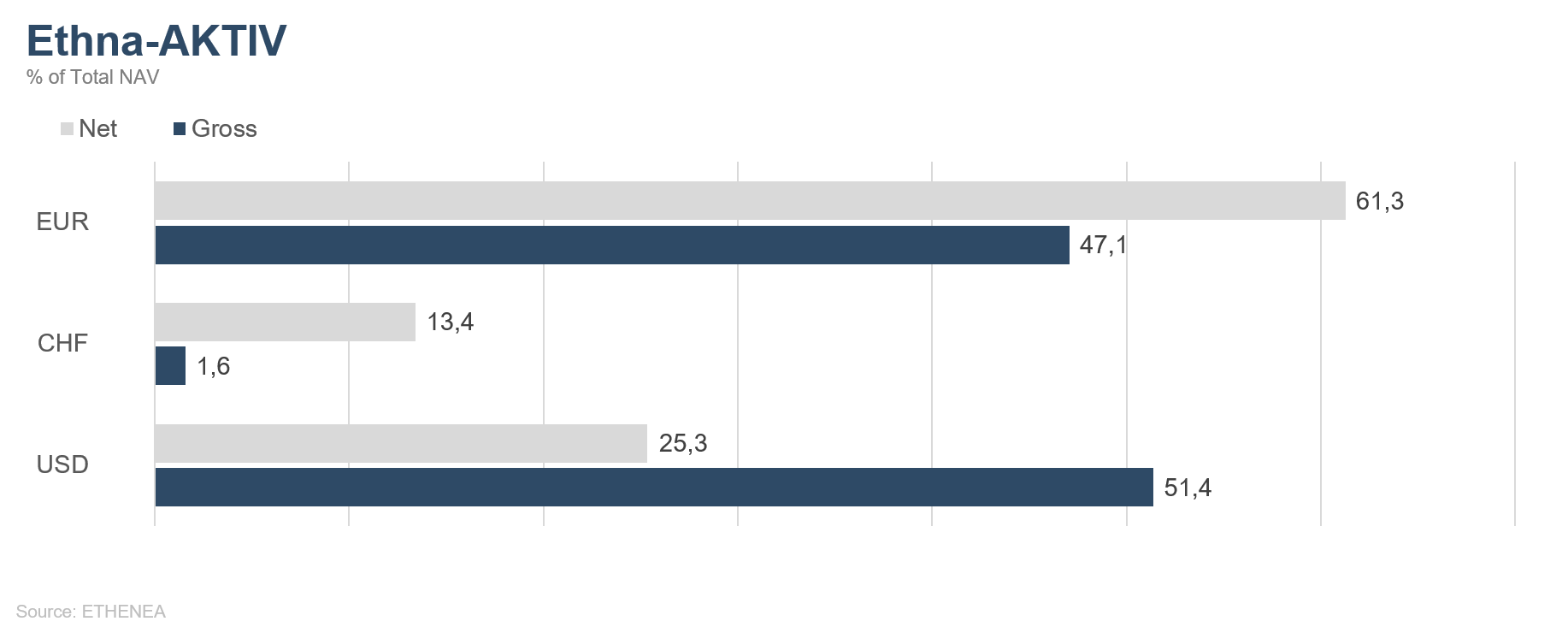

Ethna-AKTIV

From the point of view of stock markets, the month of December ended not only a very successful year, but also an exceptional decade. The much-vaunted year-end rally materialised and helped the global equity indices in particular to reach fresh highs for the year – and in some cases, even all-time highs. As in the months prior, the reasons for the main events were threefold: the majority of price movements were again attributable to the central bank meetings, debate about the trade conflict and Brexit. There was positive news on all three fronts. While the U.S. central bank did end the short-term cycle of rate cuts, it also made it clear that rate hikes cannot be expected in the near future. On the basis of this supportive stance, both surprisingly good labour market figures in the United States and the announcement of a Phase One deal between China and the U.S. – despite its flimsiness – led to further price rises. The clear victory of the Tories in the UK general election on 12 December have paved the way for an orderly Brexit. Almost three years of deadlock should therefore be nearing an end. Even though the UK’s certain exit from the EU is not exactly positive as such, it is at least a welcome end to the uncertainty in the capital markets.

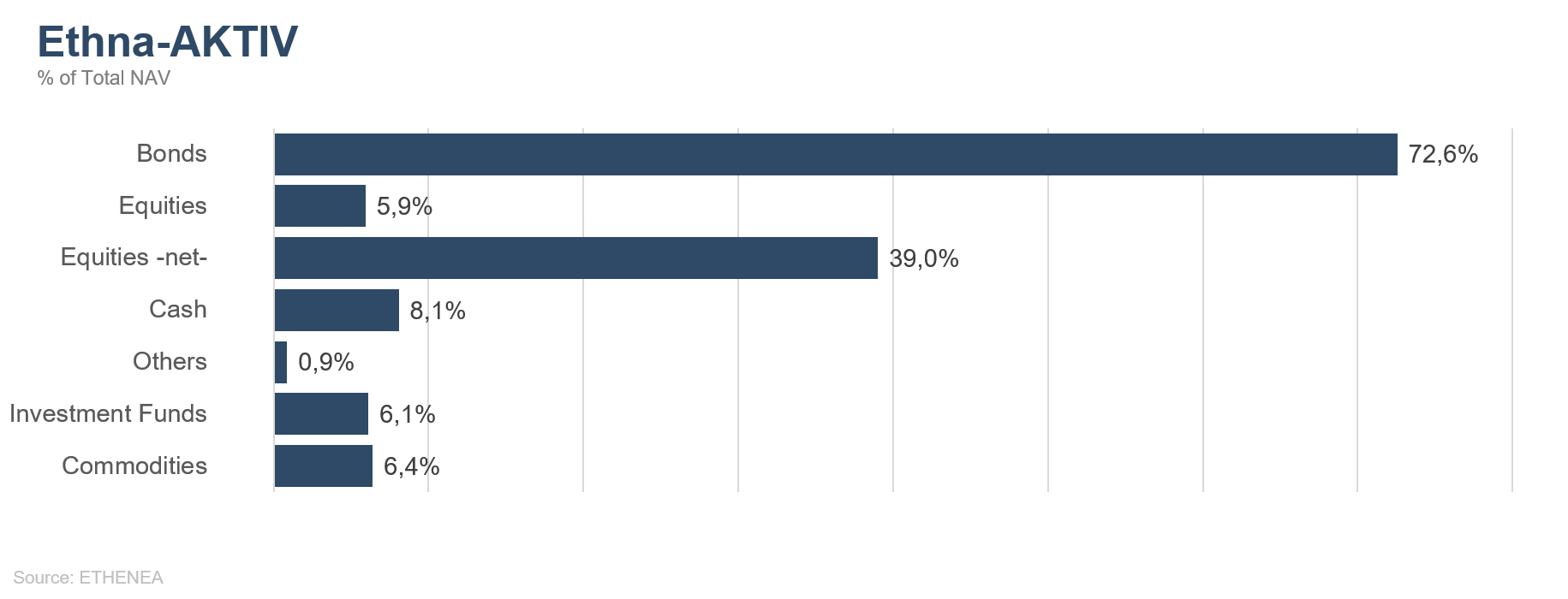

The euro in particular benefited, and managed to sustain a breakout from its low trading range at the beginning of October. In the meantime, the price of the U.S. dollar versus the euro is reaching a level at which we will be compelled to reduce the position for tactical reasons, despite our positive opinion of the dollar. The current 25% position was a slight detractor from fund performance in December. The gains on a stronger Swiss franc were unable to fully make up for this, as the position was much smaller (13%). On the equity side, we slightly reduced the positioning solely for tactical reasons during the week of the central bank meeting and the general election. We subsequently increased the allocation to almost 40%, as we still expect the rally to continue. We took advantage of the very low volatility by having a quarter of the exposure in options on the S&P 500. This will cushion the blow of short-term setbacks, which are to be expected. Instead of EURO STOXX 50 futures, we now have 5% futures on bank equities, which should benefit both from the general rise in the equity market and from the steepening yield curve in Europe. The corporate bond portfolio was further slightly reduced in favour of Spanish sovereign bonds. Long-dated American bonds in particular were sold. This resulted in a shorter duration, and the sale of interest futures reduced duration further; we do not rule out a further rise in the short term, especially in American interest rates. Both measures reduced the modified portfolio duration from 7 to 6. Overall, the gains from the narrowing of spreads and the losses due to the rise in interest rates balanced each other out. In the next few months, we plan to successively reduce the weighting of corporate bonds to approx. 60% due to the deterioration of the risk/return ratio.

We expect the rally in equities to continue at the start of 2020. Negative headlines, such as the ongoing impeachment of President Trump and the resumption of geopolitical unrest involving North Korea, have not impacted on the market so far. One decisive factor in how risk assets fare in 2020 will be the extent to which the fundamental data can confirm the higher valuation of the equity indices; secondly, what happens in the U.S. election, which will start to heat up with the Iowa caucuses at the beginning of February, will also have a strong effect on the market. Ultimately, in historical terms, U.S. election years where the sitting president has been re-elected have been above-average years for stock markets. It remains to be seen whether this will hold true for 2020.

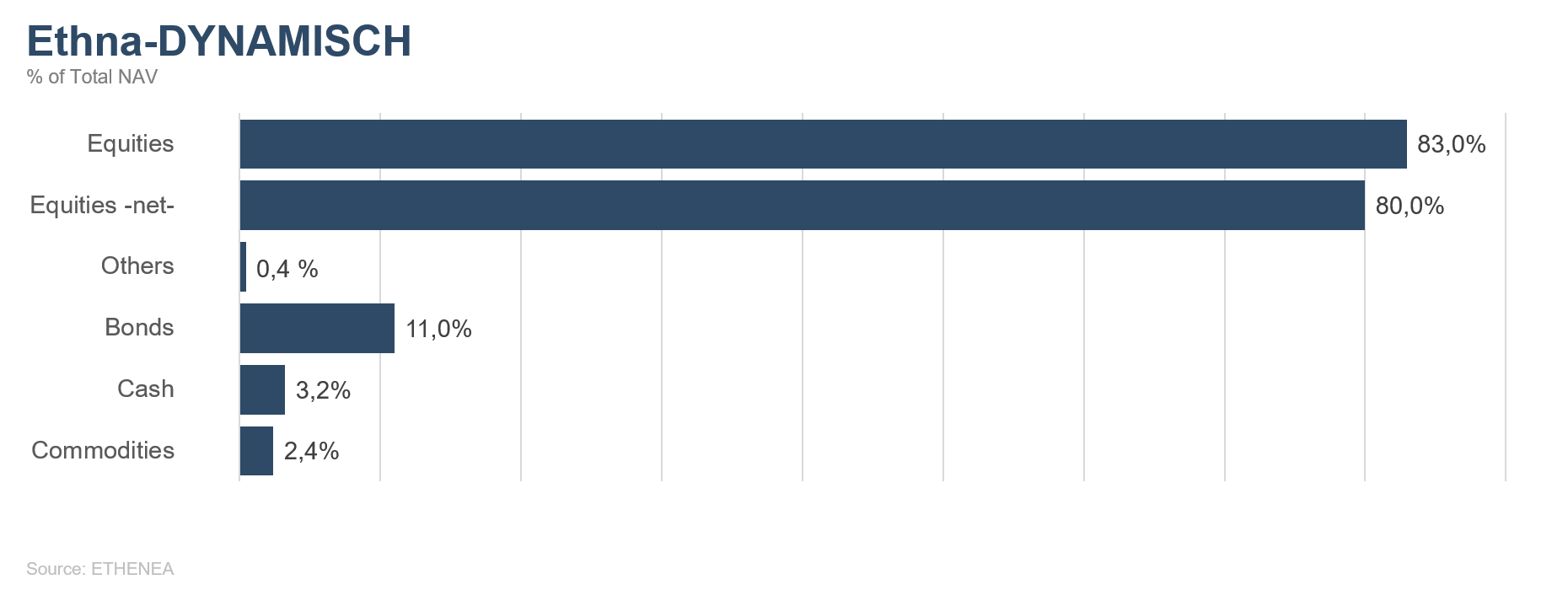

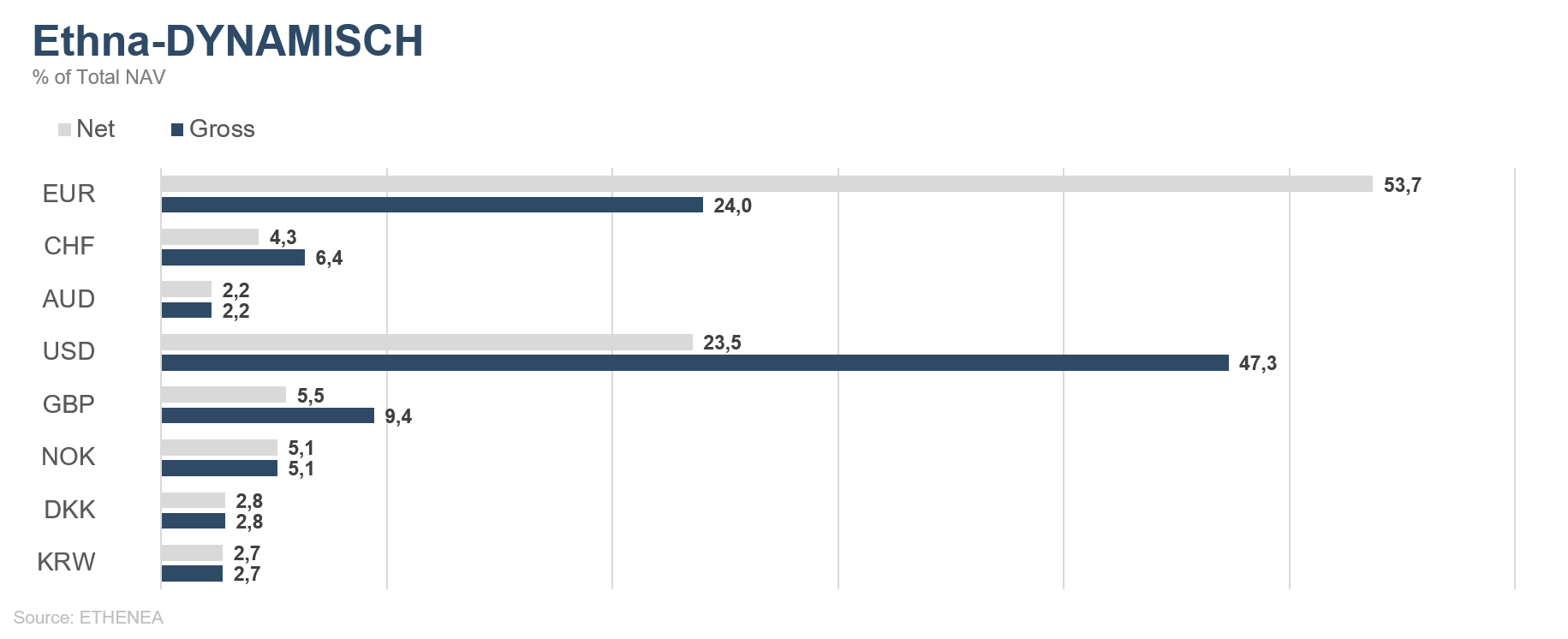

Ethna-DYNAMISCH

2019 was one for cracking open the champagne! December marked a positive end to a strong year for the stock markets overall. It was also the end of a very successful decade for equity markets, even though the basis of comparison (31 December 2009) was low due to the financial crisis in 2008/09. The decade was much more successful for the U.S. than for the rest of the world. Emerging markets suffered the effects of low commodities prices and there was infighting in Europe. This can be seen from weak growth rates and stock market momentum that could not match the pace in the U.S. In December at least, there were some positive signals out of Europe that can help overcome the chronically weak growth. The election in the UK resulted in a majority in parliament, and the final resolution of the vexatious question of Brexit is nigh. European – and UK stock exchanges in particular – benefited from mid-December. There was no upset on the economic front in December. U.S. growth remains solid and Europe is trying not to fall behind. The leading indicators are still climbing and expectations, as measured by the ifo index, which is closely watched in Germany, have risen for the third time in succession, which can be seen as a hugely positive signal. There should therefore be no fear of recession for the time being.

We added two new equities to the portfolio in December. Fever-Tree PLC is a British manufacturer of premium mixers. Fever-Tree is benefiting from the boom in gin and tonic, and its variety of tonics and a market share of up to 50% in the UK make it the clear market leader. Fever-Tree is expecting further growth, especially from its expansion in the U.S. The second new equity is Bunzl PLC. The outsourcing and distribution company for consumer goods headquartered in London primarily serves customers in the B2B sector, such as hospitals and hotels. The demand patterns of such customer groups are stable and reliable. In addition, the valuation is relatively cheap.

There were major adjustments in the bond portfolio in December. Our cash position, 6% of which was invested in the Norwegian krone, was shifted into short-dated NOK bonds from first-class issuers (KFW, EIB). In addition, another 4% was invested in 30-year U.S. Treasuries. U.S. yields have increased perceptibly since August/September and the cost of hedging against rising interest rates is getting extremely high. Given this state of affairs, using Treasuries for diversification makes increasing sense for the portfolio.

The gold and hedging components remained unchanged compared with November.

What do we expect for the coming year? 2020 will see a face-off between the bears with their late cycle, higher valuations and sluggish economy, and the bulls with their lower interest rates and scarcity of investment opportunities. In our opinion, the investment crisis will win out, and further boost equities. The (in some cases) high valuations should not be completely disregarded, but are put into perspective by the effectively non-existent interest rates. Dividend yields in more or less all European equity markets are well above the yields on corresponding sovereign bonds, which are negative for the short to medium term. The dividend yield in the S&P 500 is approximately on a par with 10-year U.S. Treasuries. A direct comparison of valuations emphasises the attractiveness of equities. For these reasons, we will hold a significant equity allocation in the Ethna-DYNAMISCH portfolio in the new year.

Figure 3: Portfolio structure* of the Ethna-DEFENSIV

Figure 4: Portfolio structure* of the Ethna-AKTIV

Figure 5: Portfolio structure* of the Ethna-DYNAMISCH

Figure 6: Portfolio composition of the Ethna-DEFENSIV by currency

Figure 7: Portfolio composition of the Ethna-AKTIV by currency

Figure 8: Portfolio composition of the Ethna-DYNAMISCH by currency

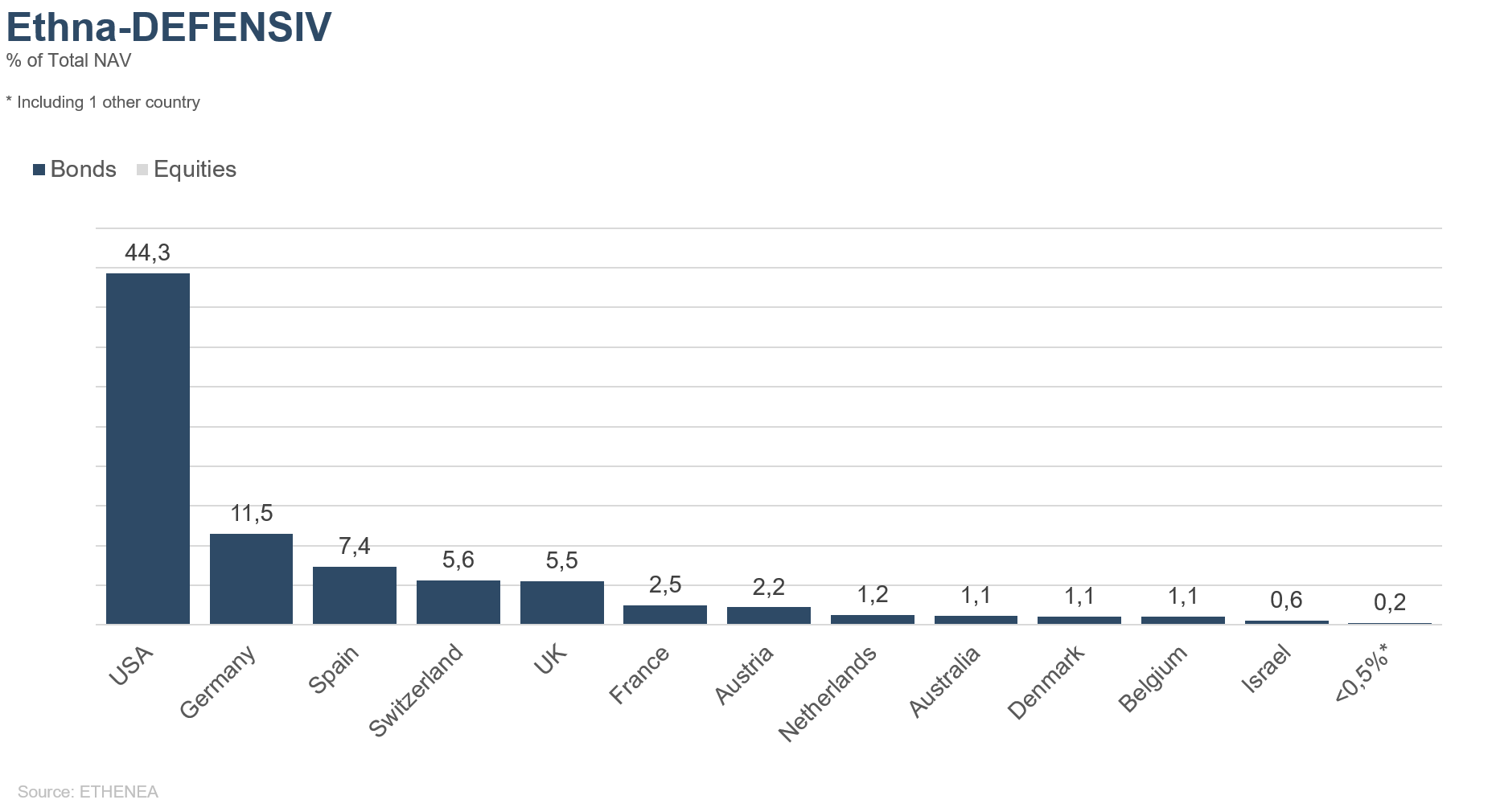

Figure 9: Portfolio composition of the Ethna-DEFENSIV by country

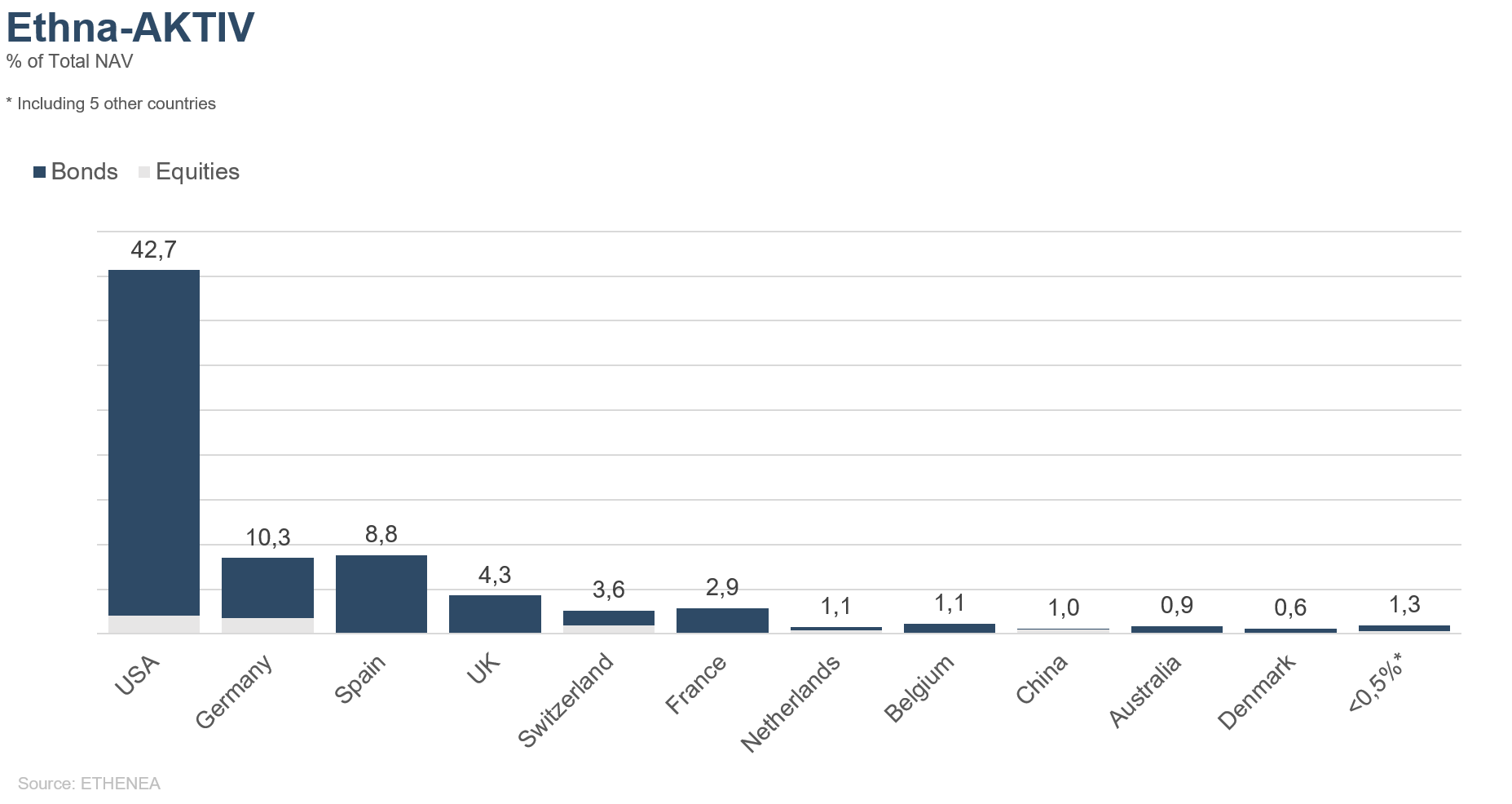

Figure 10: Portfolio composition of the Ethna-AKTIV by country

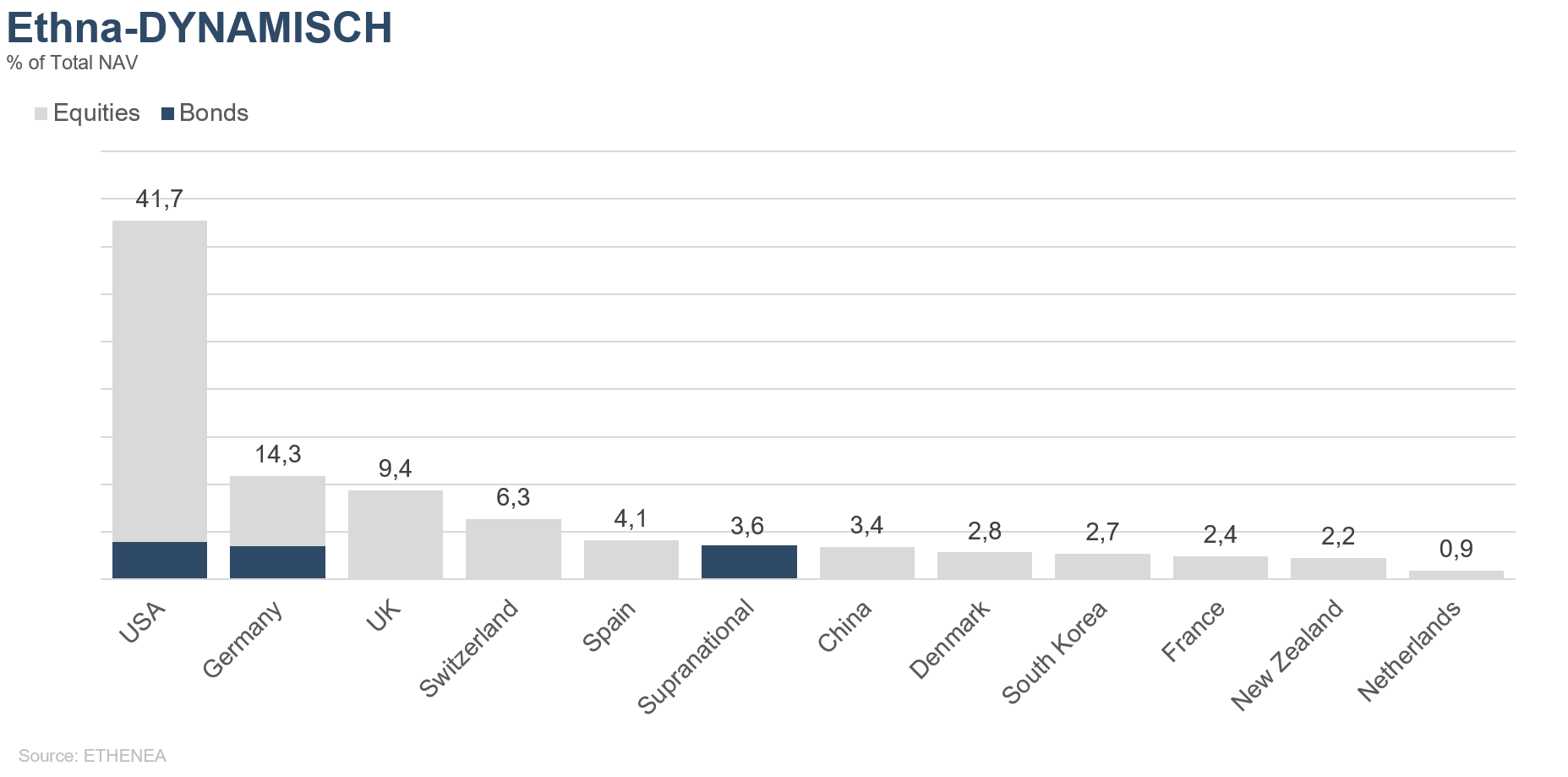

Figure 11: Portfolio composition of the Ethna-DYNAMISCH by country

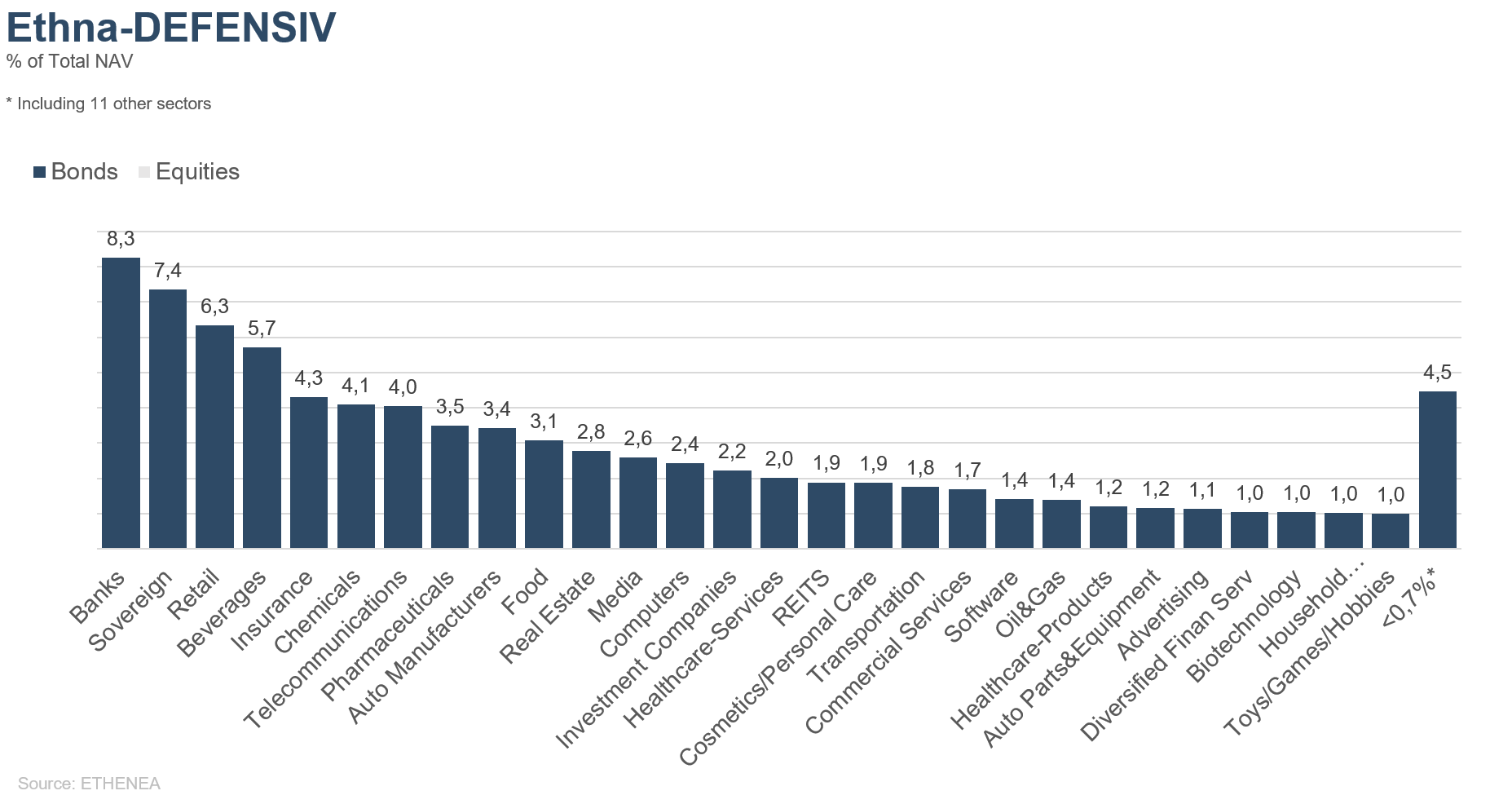

Figure 12: Portfolio composition of the Ethna-DEFENSIV by issuer sector

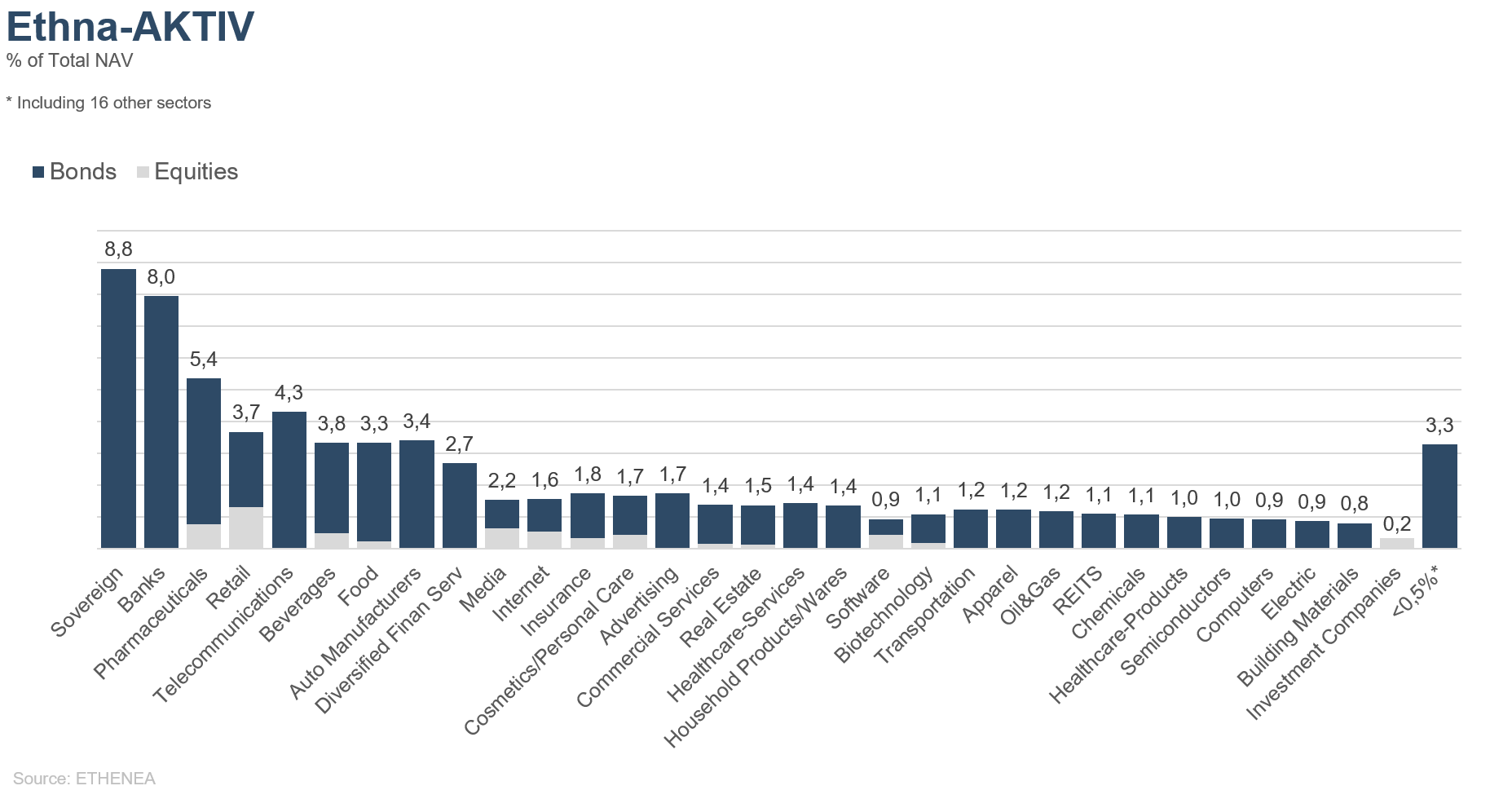

Figure 13: Portfolio composition of the Ethna-AKTIV by issuer sector

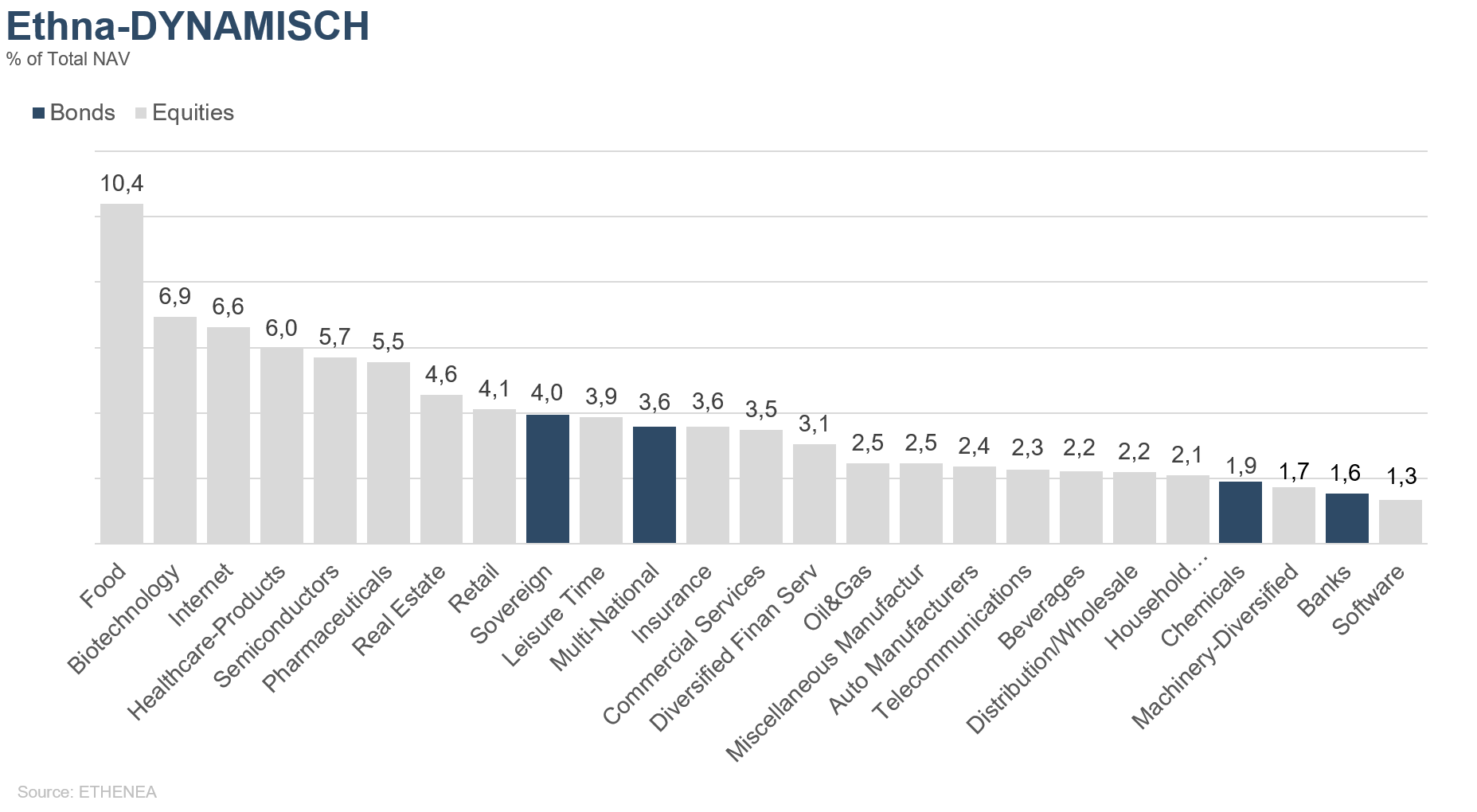

Figure 14: Portfolio composition of the Ethna-DYNAMISCH by issuer sector

* “Cash” comprises term deposits, call money and current accounts/other accounts. “Equities net” comprises direct investments and exposure resulting from equity derivatives.

Please contact us at any time if you have questions or suggestions.

ETHENEA Independent Investors S.A.

16, rue Gabriel Lippmann · 5365 Munsbach

Phone +352 276 921-0 · Fax +352 276 921-1099

info@ethenea.com · ethenea.com

Deze marketingmededeling dient uitsluitend ter informatie. Het mag niet worden doorgegeven aan personen in landen waar het fonds niet voor distributie is toegestaan, met name in de VS of aan Amerikaanse personen. De informatie vormt noch een aanbod noch een uitnodiging tot koop of verkoop van effecten of financiële instrumenten en vervangt geen op de belegger of het product toegesneden advies. Er wordt geen rekening gehouden met de individuele beleggingsdoelstellingen, financiële situatie of bijzondere behoeften van de ontvanger. Lees vóór een beleggingsbeslissing zorgvuldig de geldende verkoopdocumenten (prospectus, essentiële informatiedocumenten/PRIIPs-KIDs, halfjaar- en jaarverslagen). Deze documenten zijn beschikbaar in het Duits en als niet-officiële vertaling bij ETHENEA Independent Investors S.A., de bewaarbank, de nationale betaal- of informatiekantoren en op www.ethenea.com. De belangrijkste vaktermen vindt u in de lexicon op www.ethenea.com/lexicon/. Uitgebreide informatie over kansen en risico's van onze producten vindt u in het actuele prospectus. In het verleden behaalde resultaten bieden geen betrouwbare indicatie voor toekomstige prestaties. Prijzen, waarden en opbrengsten kunnen stijgen of dalen en kunnen leiden tot volledig verlies van het geïnvesteerde kapitaal. Beleggingen in vreemde valuta zijn onderhevig aan extra valutarisico's. Aan de verstrekte informatie kunnen geen bindende toezeggingen of garanties voor toekomstige resultaten worden ontleend. Aannames en inhoud kunnen zonder voorafgaande kennisgeving worden gewijzigd. De samenstelling van de portefeuille kan op elk moment wijzigen. Dit document vormt geen volledige risico-informatie. De distributie van het product kan vergoedingen opleveren voor de beheermaatschappij, verbonden ondernemingen of distributiepartners. De informatie over vergoedingen en kosten in het actuele prospectus is doorslaggevend. Een lijst van nationale betaal- en informatiekantoren, een samenvatting van de beleggersrechten en informatie over de risico's van een foutieve netto-inventariswaarde-berekening vindt u op www.ethenea.com/juridische-opmerkingen/.In geval van een foutieve NIW-berekening wordt compensatie verleend volgens CSSF-circulaire 24/856; bij via financiële intermediairs aangeschafte participaties kan de compensatie beperkt zijn. Informatie voor beleggers in Zwitserland: Het land van herkomst van de collectieve belegging is Luxemburg. De vertegenwoordiger in Zwitserland is IPConcept (Schweiz) AG, Bellerivestrasse 36, CH-8008 Zürich. De betaalagent in Zwitserland is DZ PRIVATBANK (Schweiz) AG, Bellerivestrasse 36, CH-8008 Zürich. Prospectus, essentiële informatiedocumenten (PRIIPs-KIDs), statuten en de jaar- en halfjaarverslagen zijn gratis verkrijgbaar bij de vertegenwoordiger. Informatie voor beleggers in België: Het prospectus, de essentiële informatiedocumenten (PRIIPs-KIDs), de jaarverslagen en de halfjaarverslagen van het subfonds zijn op verzoek gratis in het Duits verkrijgbaar bij ETHENEA Independent Investors S.A., 16, rue Gabriel Lippmann, 5365 Munsbach, Luxemburg en bij de vertegenwoordiger: DZ PRIVATBANK AG, Niederlassung Luxemburg, 4, rue Thomas Edison, L-1445 Strassen, Luxemburg. Ondanks de grootst mogelijke zorg wordt geen garantie gegeven voor de juistheid, volledigheid of actualiteit van de informatie. Alleen de originele Duitstalige documenten zijn juridisch bindend; vertalingen dienen alleen ter informatie. Het gebruik van digitale advertentieformaten is op eigen risico; de beheermaatschappij aanvaardt geen aansprakelijkheid voor technische storingen of schendingen van gegevensbescherming door externe informatieaanbieders. Het gebruik is alleen toegestaan in landen waar dit wettelijk is toegestaan. Alle inhoud is auteursrechtelijk beschermd. Elke reproductie, verspreiding of publicatie, geheel of gedeeltelijk, is alleen toegestaan met voorafgaande schriftelijke toestemming van de beheermaatschappij. Copyright © ETHENEA Independent Investors S.A. (2026). Alle rechten voorbehouden. 03-01-2020